Can Passive Income Offset Passive Loss

Understanding Passive Activity Limits And Passive Losses 2020 Tax Update Stessa

You Either Need Cash Or Time To Create Passive Income There Are Many Ways To Achieve Financial F Start Online Business Creating Passive Income Online Business

How I Earn High And Passive Income From Rental Properties Seeking Alpha

Best Passive Income Investments 2019 Foxy Monkey

Pin By Financial Shaper On Monthly Dividend Income Dividend Income Income Passive Income Streams

How Is Passive Income Taxed Free Investor Guide

Passive losses are only deductible up to the amount of passive income.

Can passive income offset passive loss. Each and every single company on earth that manufactures or produces a product wants to sell it. I believe after several hours of research on the internet the answer is yes you can use passive loss carryover to offset up to 25k of ordinary income if you make less than 100k which my wife and myself do as we only have a household income of about 40k per year mostly from social security. They would use this lease income ordinarily passive income to offset the losses from their rentals. Losses from rental property are considered passive losses and can generally offset passive income only that is income from other rental properties or another small business in which you do not materially participate not including investments.

Passive activity losses are generally not deductible. The short answer is maybe the internal revenue service irs generally doesn t allow passive losses from real estate investments to be deducted from any type of income other than rental profits. They can be used. Classification of losses affects the ability to offset other profits profits from other activities not related to the business that the investor includes in her personal income.

And a loss that results from rental real estate is always considered to be passive even if you meet the 500 hour requirement. So if you have a passive loss from a passive activity and nonpassive income from a nonpassive activity such as a sole proprietorship that you own and run you would not be allowed to deduct a loss from the passive activity from a net profit of the sole proprietorship. Passive activity loss rules are a set of irs rules stating that passive losses can be used only to offset passive income. Passive losses can be used to offset passive income.

Likewise active losses can be used to offset active income. Currently what do you assume costs much more for that corporation. A permanent salaried and commissioned salesman with a workplace a corporate vehicle and also a business charge card. As a result of this combination of income and losses the beechers paid no tax on the rental income paid to them by their corporations this amounted to over 85 000 of tax free income over three years.

To qualify your modified adjusted gross income must not exceed 100 000 for the year. A passive activity is one wherein the taxpayer did not materially. You may not offset passive losses against nonpassive income.

Pin By Financial Shaper On Monthly Dividend Income Dividend Dividend Income Financial

Proven Ways On How To Make Money Online Faq What Are The Ways On How To Make Money Online Beradiva Beradiva Proven Ways On How To Make Money Online Beradiva

Rental Property Tax Deductions Real Estate Rentals Being A Landlord Property Tax

Passive Income Definition

Changing Level Of Participation In An S Corporation For Tax Planning Purposes

Passive Income Concept Stock Vector Royalty Free 200593751

Claiming A Business Loss On Taxes Can Schedule C Losses Offset W 2 Income Or Do The Hobby Loss Rules Prevent This Personal Finance Bloggers Personal Finance Finance Bloggers

How To Earn Money Without Skills Full Time Income Part Time Income In 2020 Earn Money Income Business Management

Which Geoup Would You Pick Comment Bellow In 2020 Dividend Dividend Stocks Business Money

Is Rental Income Passive Or Active Free Investor Guide

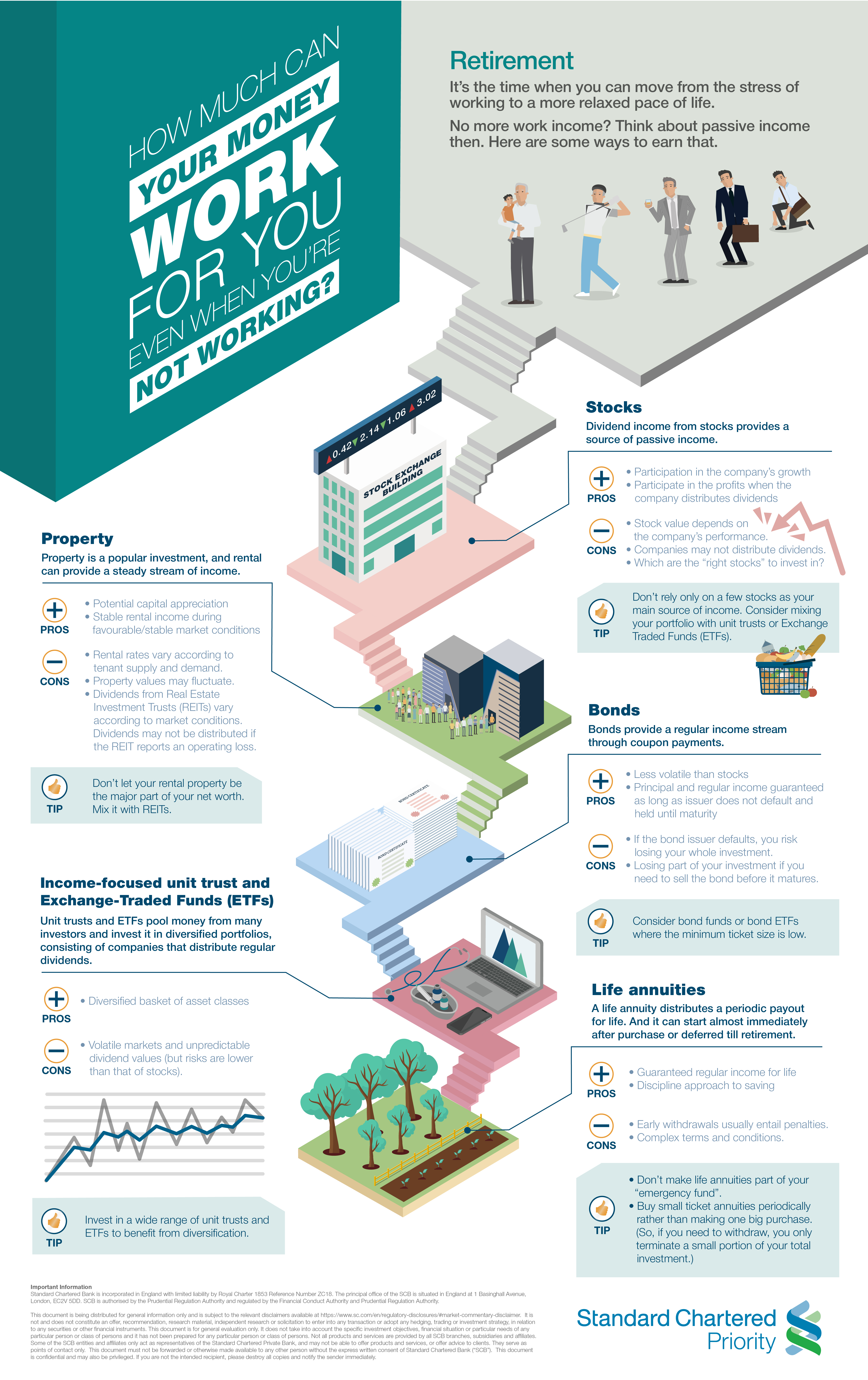

Passive Income For Retirement Standard Chartered Singapore

Passive Income For Christmas Something 2 Offer Ways To Save Money Money Spending Money

Tax Loss Harvesting Tax Tax Brackets Income Tax