Corporate Tax Rate On Passive Income In Canada

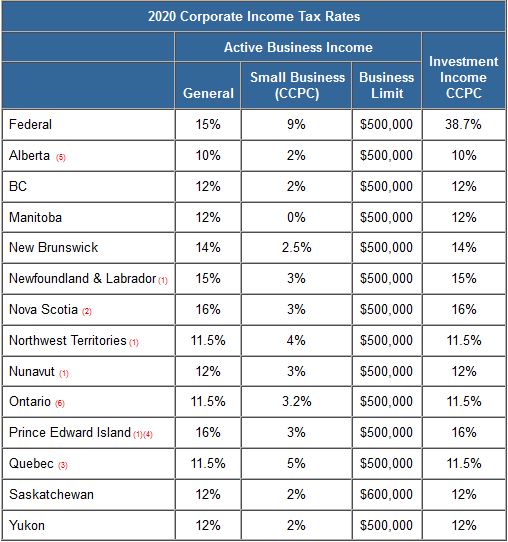

Taxtips Ca Business 2020 Corporate Income Tax Rates

Tax Checklist For Canadians Tax Checklist Tax Prep Checklist Financial Checklist

Taxtips Ca Personal Income Tax Rates For Canada Provinces Territories

Pin By Christen Best Money Mom Pe On Investing Money In 2020 Income Tax Money Mom Tax Refund

Annual Financial Report Of The Government Of Canada Fiscal Year 2017 2018 Canada Ca

Income Tax 2020 Changes Every Canadian Needs To Know In 2020 Money Mom Income Tax Budgeting Money

With the exception of inter corporate dividends passive income earned by ccpcs or any corporation in canada is ineligible for deductions and consequently fully taxable at the corporation s combined provincial and federal tax rate.

Corporate tax rate on passive income in canada. As outlined the effective tax rate on passive income is 50 7 while dividend income is taxed at 38 3. The higher rate is 14. Table 1 below walks us through the corporate tax rates for those four types of income. Prior to april 1 2018 it 3.

In other words only 350k of active business income is eligible under the small business tax rate of 10 rather than the general corporate tax rate of 15. At 150 000 of passive income none of the active business income will qualify for the small business tax rate. Passive investment income in your private corporation. In this case the business owner would pay an additional 150k 5 7 500 in corporate tax following the assumptions in the table above.

The new rule changes mean that a ccpc s passive investment income now exposes a business owner to more tax on active business income. This has a dramatic effect on the amount of tax on that 500 000. For many small business owners their private company is a key component in saving for their family and their future retirement. Since 2009 a ccpc using the sbd could claim the small business tax rate on the first 500 000 of its active business income carried on in canada representing a fairly substantial reduction in tax.

In new brunswick the lower rate of corporate income tax is 2 5. The following rates apply for a 12 month taxation year ending on 31 december 2020. This is frequently higher than the marginal tax rate payable by the individual which reduces the desirability. However a portion of the federal tax on passive and dividend income is refundable when a taxable dividend is paid to a corporation s shareholder.

For non resident corporations the rates apply to business income attributable to a permanent establishment pe in. For this ccpc 150 000 of passive investment income results in 135 500 of tax on active business income at the combined corporate tax rate of 27.

The Guide On Tax Efficient Investing In Canada Genymoney Ca Investing Dividend Income Dividend Investing

A 93 Tax Rate Private Corporation Tax Could Make It Possible Tax Rate Tax Tax Lawyer

If You Have Rental Properties In Canada Check Out This Helpful Infographic F Real Estate Investing Rental Property Rental Property Investment Rental Property

Get The Right Tax Information Tools And Resources You Need To Plan And Prepare For Filing Small Business Taxes Small Business Tax

Https Encrypted Tbn0 Gstatic Com Images Q Tbn And9gcscmaefvmvtjfaiaxakoludm C1r I9loo6xg Usqp Cau

What Is Considered Passive Income In Canada

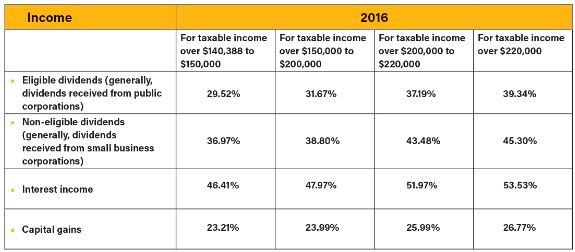

Tax Tips 2016 Investment Income Capital Gains And Losses Tax Canada

How Money You Earn Flows Through Your Corporation To Your Pocket Physician Finance Canada

Pin On Investing Money Financial Freedom

Download J K Lasser S Your Income Tax 2020 Pdf Free In 2020 Tax Guide Tax Return Filing Taxes

What Can I Claim On My Taxes In Canada The Young Professional Tax Refund Tax Deductions Tax Return

Tax Tardiness The Who What And Why Of Late Filing Finance Infographic Canadian Money Infographic

Are You Bored Living In Poor Mindset You Are On The Right Place If You Want To Learn About In 2020 Business Inspiration Quotes Finance Investing Inspirational Quotes