Excess Net Passive Income Tax Worksheet

Instructions For Form 5471 02 2020 Internal Revenue Service

Instructions For Form 8995 2019 Internal Revenue Service

Is An Anomaly In Form 8960 Resulting In An Unintended Tax On Tax Exempt Income

Learn How To Report And Pay Taxes On Your 1099 Income Paying Taxes Income Income Tax Return

Instructions For Form 8990 05 2020 Internal Revenue Service

Instructions For Form 1040 Nr 2019 Internal Revenue Service

Built in gains big tax if a corporation has always been an s corporation built in gains.

Excess net passive income tax worksheet. The threshold for the enpi calculation is triggered when gross enpi is greater than 25 of gross receipts and the corporation has e p at year end. Gross royalty income. Available for pc ios and android. If your taxable income includes net capital gain and qualified dividend income you may be eligible for a tax rate on that income that is lower than the tax rate that applies to your other income.

Excess net passive income tax worksheet for line 22a. Excess net passive income is a corporate level tax on the passive income earned by an s corporation. Subtract line d from line b and enter the result on form 8582 cr line 6 for form 1040 or 1040 sr use the tax table tax computation worksheet or other appropriate method you used to. Taxable income including net passive income b.

Passive income includes income from interest dividends annuities rents and royalties. The most secure digital platform to get legally binding electronically signed documents in just a few seconds. Refer to irs form 1040 schedule d. Start a free trial now to save yourself time and money.

Capital gains not losses gross sales price from gains. Taxable income without net passive income d. To compute line 1 gross receipts for the tax year on the worksheet for excess net passive income tax the system includes the following. The excess net passive income tax applies if passive income is more than 25 of the s corporation s gross receipts.

Fill out securely sign print or email your excess net passive income tax instantly with signnow. Tax on line a c. Excess net passive income and lifo recapture tax. Interest due under the look back method completed long term contracts.

Investment credit recapture tax. This is not a problem if the s corporation has no accumulated e p. If the corporation has accumulated earnings and profits e p at the close of its tax year has passive investment income for the tax year that is in excess of 25 of gross receipts and has excess net passive income the corporation must pay a tax on the excess net passive income. Excess net passive income tax.

Tax from schedule d form 1120 s line 22c. The excess net passive income that is subject to the tax is limited to the taxable income calculated as if it were still a c corporation. Excess net passive income tax is 35 of the lesser of enpi or taxable income. Excess net passive income tax.

However if it does have both e p and excess passive investment income some of the excess net passive investment income may be subject to tax at the highest corporate income tax rate currently 35 thus the sting. In this example the corporation incurs an excess net passive income tax of 1 809 35 of 5 169. Non taxable interest income and dividend income.

Https Www Columbus Gov Workarea Downloadasset Aspx Id 2147512446

Https Www Cityofspringboro Com Documentcenter View 809 2018 Individual Income Tax Return Pdf

Https Www Ato Gov Au Uploadedfiles Content Mei Downloads Nat0976deduct 04 Pdf

Http Www Psc State Ms Us Insiteconnect Insiteview Aspx Model Insite Connect Queue Cts Archiveq Docid 556418

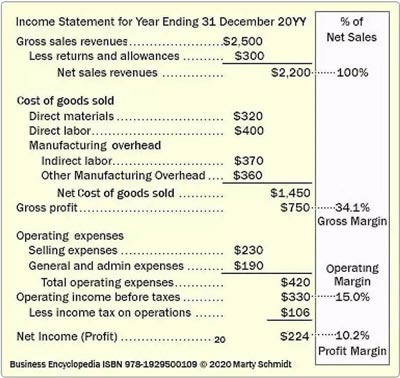

How To Read Income Statement Understand Structure And Contents

Https Investor Apachecorp Com Static Files 92f9e587 Ae4a 4b89 9fcc 33a78f9a7d13

Publication 514 2019 Foreign Tax Credit For Individuals Internal Revenue Service

Finacc3 Debits And Credits Expense

Https Revenue Ky Gov Software Developer Corporation 20income 20tax 20forms 16 41a720s I Pdf

Https Www Gillibrand Senate Gov Download 2019taxes

Corporate Partnership Estate And Gift Taxation 6th Edition Pratt Solu

Https Cffm Umn Edu Wp Content Uploads 2019 02 2016 Ag Income Tax Update Farm Families Pdf