Excess Passive Income Tax

Solved Calculate Anaheim Corporation S Excess Net Passive Inco Chegg Com

Chapter 22 S Corporations Ppt Download

Passive Activity Credit Flowchart

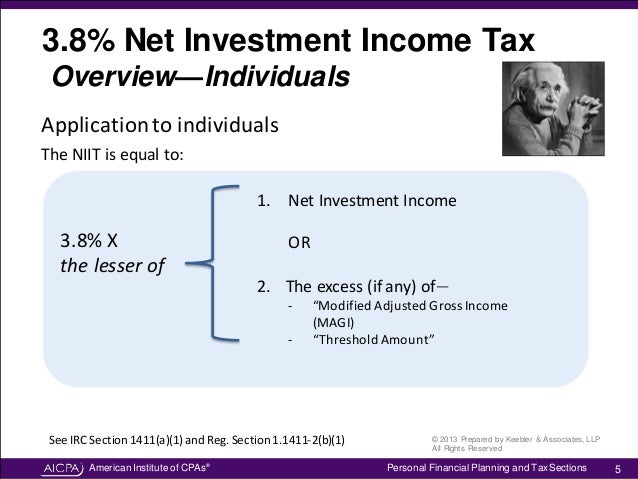

Understanding The Net Investment Income Tax

Determine Your Passive Investment Income Limit Free Tools

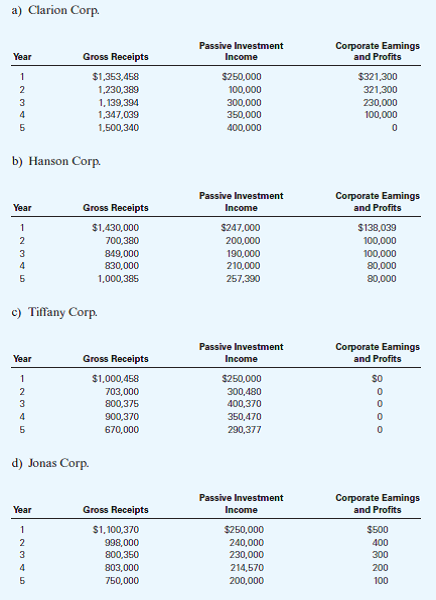

Solved Assume The Following S Corporations And Gross Receipts Chegg Com

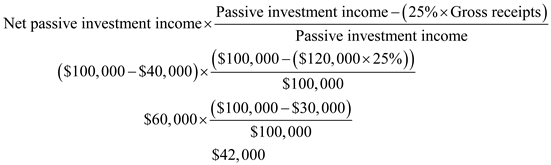

The surplus net passive income is 42 000.

Excess passive income tax. However i m still new to turbo tax and tax in general. And 2 the net passive income less deductions is multiplied by this percentage to arrive at excess net passive. The excess net passive income tax applies if passive income is more than 25 of the s corporation s gross receipts. In particular passive losses are typically deductible only against passive income and.

Excess net passive income tax. Passive income includes income from interest dividends annuities rents and royalties. Excess net passive income is a corporate level tax on the passive income earned by an s corporation. The threshold for the enpi calculation is triggered when gross enpi is greater than 25 of gross receipts and the corporation has e p at year end.

Excess net passive income is computed under a formula in which 1 the passive investment income in excess of 25 of gross receipts for the taxable year is divided by the corporation s passive investment income for the taxable year. Surplus net passive income tax is calculated 35 of least of the following. Surplus net passive income. Passive activity income often gets very different tax treatment from the ordinary income that people have.

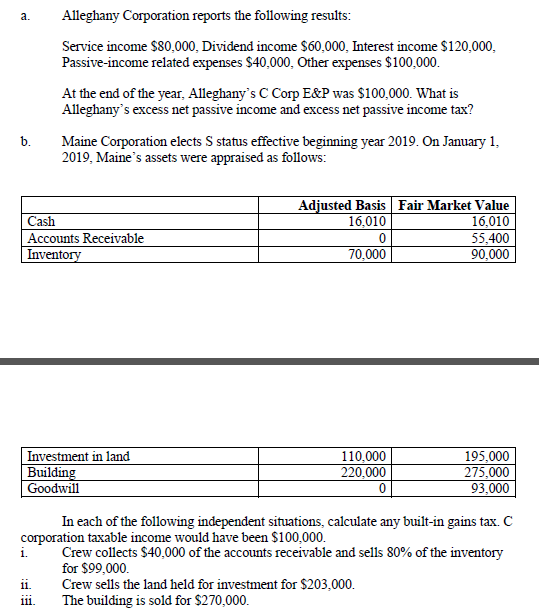

A corp s surplus net passive income tax needs to be computed under following scenarios as shown below. Taxable income if it was still a c corporation is 40 000. Excess net passive income tax if an s corporation previously operated as a c corporation and has accumulated earnings and profits at the end of the year from a prior c corporation year it may be subject to the excess net passive income tax. By reducing taxable income the s corporation is able to minimize the passive income tax.

53 congress created this tax to encourage s corporations to distribute their accumulated earnings and profits from prior c corporation years. It is still placing me back onto the excessive net passive income tax. I ve never done this and was wondering what is that. Also the passive income tax calculated using the lesser of excessive net passive income or taxable income.

Hi thank you for answering this. Can you please explain this in lemans term. Even if there is no taxable income and the sting tax does not apply if the s corporation has both e p and excess passive investment income for three consecutive tax years then under section 1362 d 3 the s corporation status will be lost on the first day of the fourth tax year. Passive income when used as a technical term is defined as either net rental income or income from a business in which the taxpayer does not materially participate and in some cases.

Income Tax Computation Corporate Taxpayer 1 2 What Is A Corporation Corporation Is An Artificial Being Created By Law Having The Rights Of Succession Ppt Download

How The New Tax Law Affects Rental Real Estate Owners Mitchell Wiggins

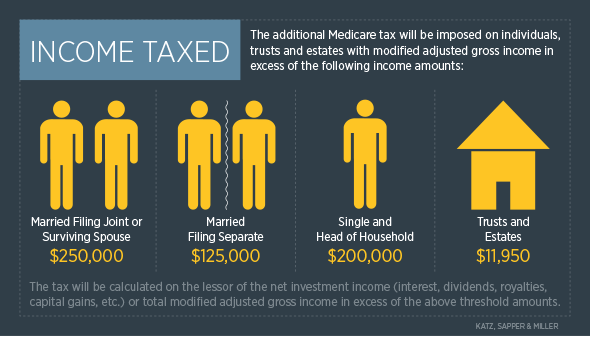

The Affordable Care Act And The 3 8 Medicare Tax Katz Sapper Miller

Ea Exam Prep Part 2b All Audio Is Streamed Through Your Computer Speakers There Will Be Several Attendance Verification Questions During The Live Webinar Ppt Download

Investing Through A Professional Corporation Physician Finance Canada

Income Types Not Subject To Social Security Tax Earn More Efficiently

Understanding Passive Activity Limits And Passive Losses 2020 Tax Update Stessa

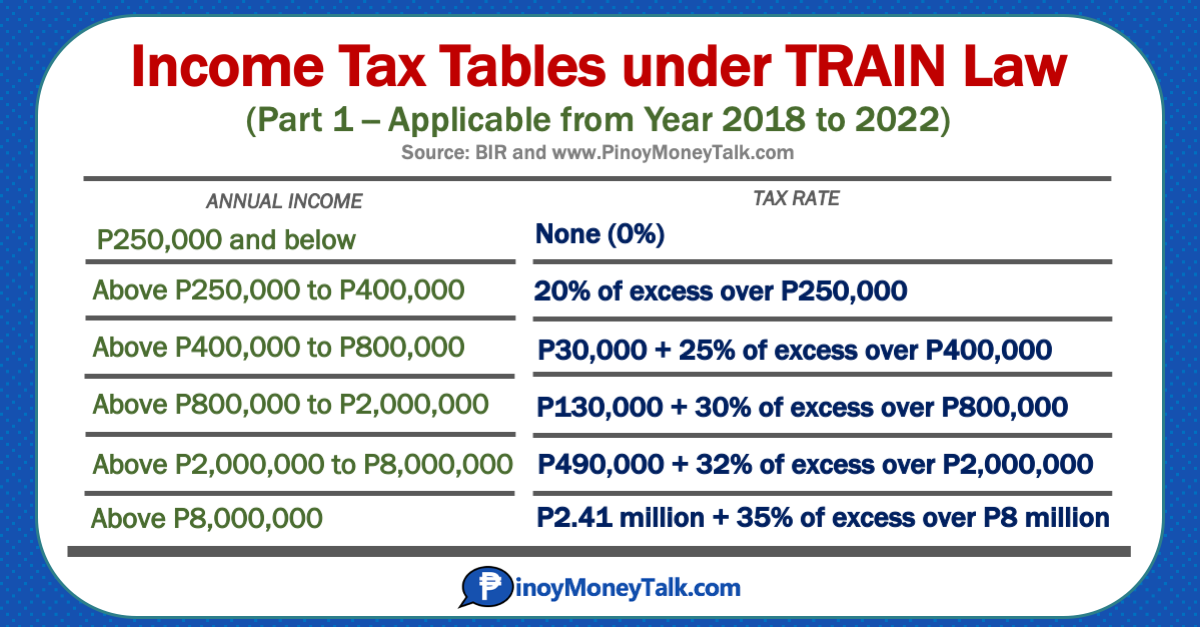

Train Law 2020 Income Tax Tables In The Philippines Pinoy Money Talk

Taxes From A To Z 2019 K Is For Kiddie Tax

Image Result For Train Tax Table Income Tax Income Tax Guide

A1t6rotnpjktsm

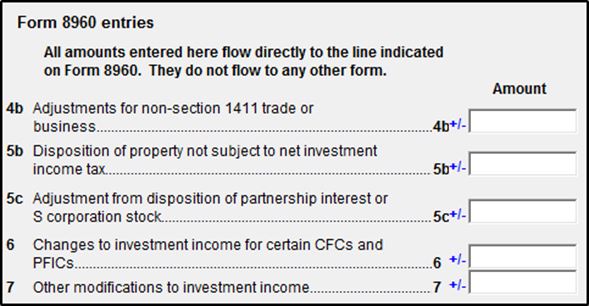

8960 Net Investment Income Tax 8960 K1 Schedulec Schedulee Schedulef