Income Capitalization Approach Cap Rate

Real Estate Appraisals The Income Capitalization Approach Income Rental Income Appraisal

Cap Rate Calculations Ccim Institute

Capitalized Income Approach Excel Spreadsheet

Cap Rate Follies Ccim Institute

Cap Rate Calculator

What Cap Rate Means When Investing In Real Estate

.gif)

Income capitalization noi cap rate let s put this to work in a different example.

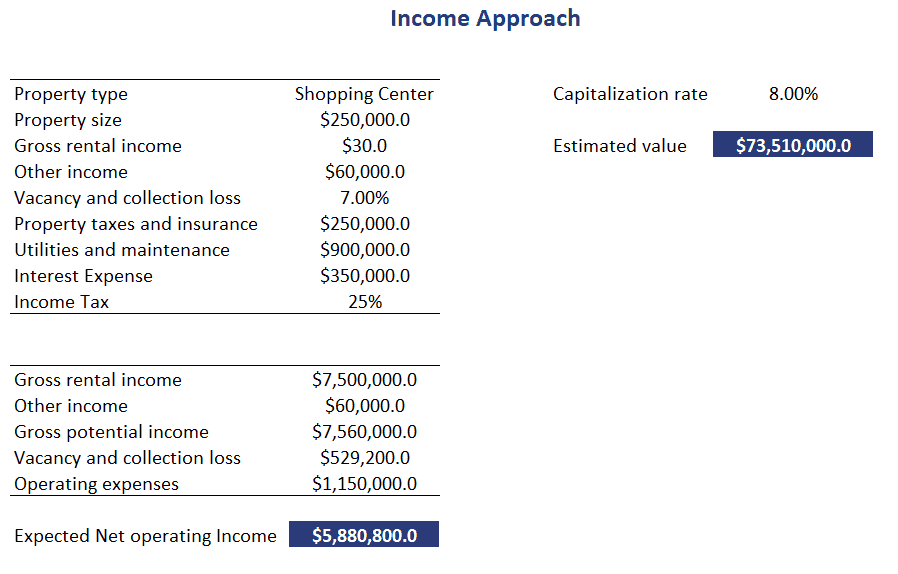

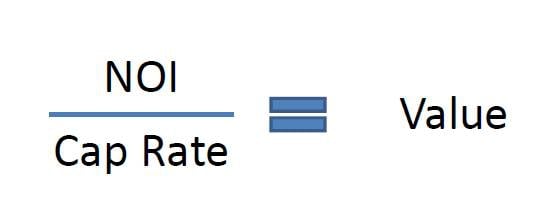

Income capitalization approach cap rate. Net operating income i capitalization rate r estimated value v 10 000 0 10 100 000. The terminal capitalization rate of 9 is estimated from current market cap rates. The capitalization rate can be used to determine the riskiness of an investment opportunity a high capitalization rate implies lower risk while a low capitalization rate implies higher risk. Capitalization rates or cap rates provide a tool for investors to use for roughly valuing a property based on its net operating income.

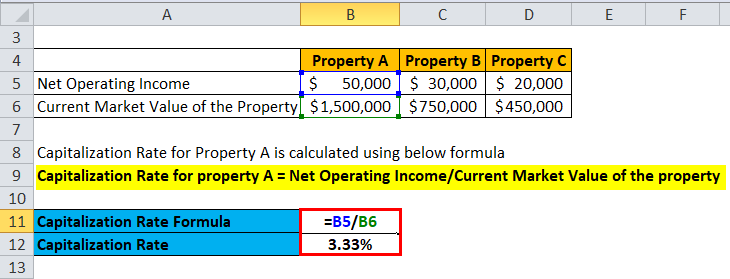

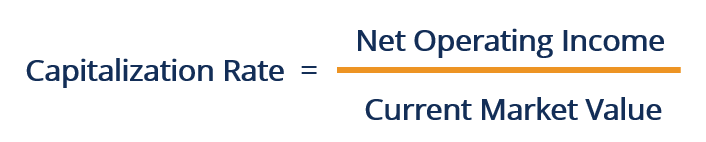

The market value will be the same whether the property has debt or is debt free. The formula for the capitalization rate is calculated as net operating income divided by the current market value of the asset. Cap rates represent the ratio of annual net operating income noi to the property asset value noi cap rate value. This is the proforma cash flow statement under the given market assumptions.

Let s say you are looking for investment properties and stumble upon a property with an 8 capitalization rate and it generates 20 000 in noi each year. The market income capitalization approach only calculates net operating income as if the property was debt free. With the income approach an investor uses market sales of comparables for choosing a capitalization rate. By dividing the net operating income of the subject property by the capitalization rate you have chosen you arrive at an estimate of 100 000 as the value of the building.

How to calculate income. By dividing the 75 000 in estimated noi by this cap rate remember to convert the percentage to a decimal or 0 065 the property s fair market value by the income capitalization approach would. Example of the income approach. For example when valuing a four unit apartment building.

For example if a real estate investment provides 160 000 a year in net operating income and similar properties have sold based on 8 cap rates the subject property can be roughly valued at 2 000 000.

Capitalization Rate Formula Calculator Excel Template

:max_bytes(150000):strip_icc()/market-value-69e5d658792841c3baabe0d0d23c2dcc.jpg)

How To Value Real Estate Investment Property

What Is Cap Rate And How To Calculate It Infographic What Is Cap Real Estate Infographic Investment Property For Sale

Hnn Hotel Capitalization Rates Caveat Emptor

Capitalization Rate And Property Tax Appeals

Capitalization Rate Cap Rate Formula Example Youtube

Rental Growth And Capitalisation Rates Uk Commercial And Industrial Download Table

Cap Rate Simplified For Commercial Real Estate Calculator

How To Calculate The Cap Rate

The Income Approach To Real Estate Valuation

What Are Capitalization Rates Ideal Rei Capitalization Rate Real Estate Investing Real Estate Advice

What Are Capitalization Rates Ideal Rei Commercial Real Estate Marketing Real Estate Investing Rental Property Capitalization Rate

Cap Rate Reit Overview How To Calculate Uses