Income Tax After Death Uk

Income Tax Form Hmrc Why You Should Not Go To Income Tax Form Hmrc In 2020 Tax Forms Income Tax Income

Tax Implications On Transferring Money Money Transfer Paying Taxes Blog Taxes

Transfer Pension To Australia Uk Pension Vs Qrops Uk Pension Pensions Death Tax

Qrops Spain 2015 How To Transfer Uk Pensions To Spain Uk Pension Spain Retirement Planning

Apply For A Repayment Of Tax Using R40 Tax Form Savings And Investment How To Apply Repayment

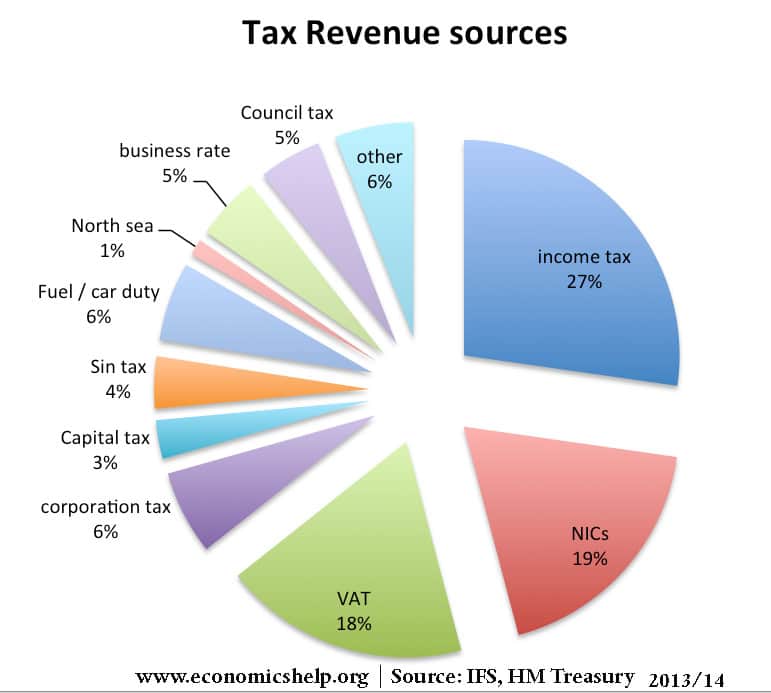

Types Of Tax Economics Help

Income from rent on a property abroad or foreign business profit and shareholdings won t have uk tax automatically deducted.

Income tax after death uk. On the death of an individual it is the personal representatives responsibility to file a tax return disclosing all income received by the deceased taxpayer from 6 april up to the date of death. There are several ways to send a trust and estate tax return to hmrc. To tell hmrc about any untaxed or foreign income call their deceased estate helpline on 0300 123 1072 call charges apply. Income tax will be charged as normal on all taxable income arising up to the date of death.

There are special rules that may apply if the personal representative is not resident in the uk and we. Fill in the paper form self assessment. For example if someone had an annual income of 24 500 lets assume for the sake of simplicity that they pay tax at a rate of 20. They would therefore pay 200 a month in tax.

You ll need to complete a tax return for the estate on this income. This period is called the period of administration. However if they died at any time in the tax year before they had earned 12 500 then they would have paid tax that would now not be due. The low incomes tax reform group litrg explain how the personal representative executor deals with and reports any income and or capital gains that arise after the deceased s death but before the estate is distributed to beneficiaries.

This other tax return is for the dead person s estate. Tax affairs up to the date of death. Therefore when the beneficiary is considering the extent of the variation it might be sensible for him to accept the income. Income tax practical law uk practice note 6 517 2446.

For the first tax year the nephew will need an r185 estate income certificate for the 400 of income deemed to be received by him net of tax in that year 300 savings interest with tax of 60 deemed to have been paid and 100 dividend income with 7 50 deemed to have been paid. Send it by post to hmrc before the 31st of october after the tax year to which it applies. Trust and estate tax return sa900.

Etaxmentor Is An Authorized E Return Intermediary Eri From Income Tax Department Etaxmentor Is One Of The It Filing Site Income Tax Filing Taxes Web Traffic

How Do I File A Deceased Person S Tax Return Tax Return Tax Deceased

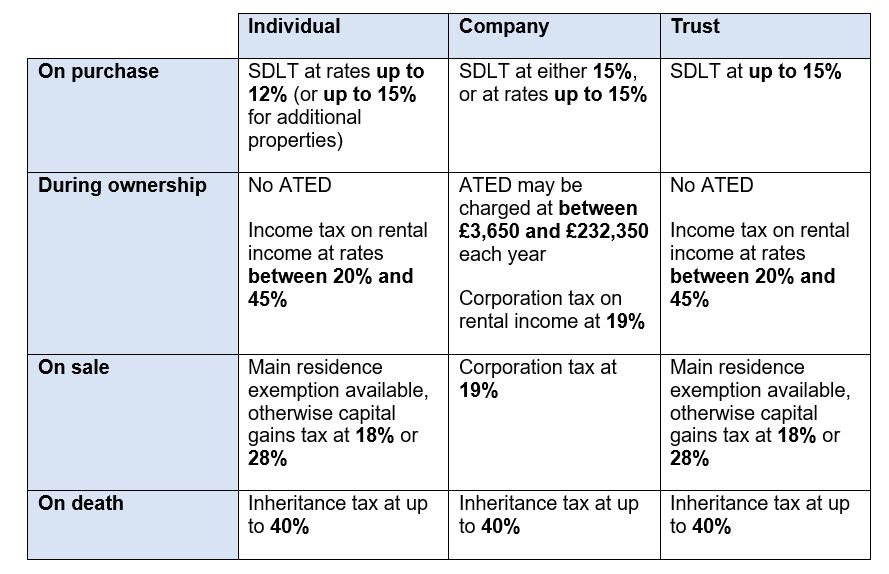

Uk Residential Property Structures What Are My Options

Portability Of Estate Tax Exemption For Surviving Spouses Estate Tax Inheritance Tax Types Of Taxes

What Is Taxable Income In The Uk Finance Blog Financial Stress Child Tax Credit

Ask The Taxgirl Help With A Corrected W 2 Federal Income Tax Paying Taxes Help

Inheritance Tax Haul Hits A Record 5 2bn So Why Is Nobody Claiming New Family Home Perk Https Www Telegraph Co Uk Inheritance Tax Inheritance Records

Tax Cartoon 2110 Andertoons Tax Cartoons Accounting Humor Accounting Jokes Tax Season Humor

Cayman Pension Rules For Uk Pension Transfers To Avoid Uk Taxes Legally For British Expats In The Caymans Uk Pension Cayman Islands British

It Takes Some Good Fortune To Win A Lottery But It Takes A Lot Of Planning To Save All The Money From The Tax Man Learn How Tax Debt Tax Debt Relief

Income Tax Returns Are The Most Imaginative Fiction Being Written Today Herman Wouk With Images Income Tax Brackets Trump Tax Plan Income Tax

Pin On Truth About Trump

Tax Cartoons Tax Season Humor Taxes Humor Accounting Humor