Passive Activity Loss Disposition Related Party

Security Deposit Itemization Pdf Being A Landlord Property Management Rental Property Management

Security Deposit Itemization Pdf Being A Landlord Property Management Rental Property Management

Http Taxworkbook Com Files 2016 08 Relatedparties Pdf

Https Www Irs Gov Pub Int Practice Units Fcu Cu C 18 2 1 04 Pdf

Https Www Irs Gov Pub Irs Pdf F6781 Pdf

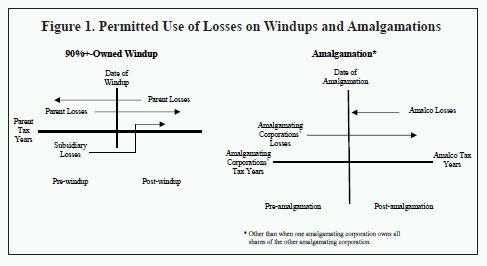

Using Tax Losses Within A Corporate Group Tax Canada

How do the disposition rules work.

Passive activity loss disposition related party. The term passive activity loss means the amount if any by which a the aggregate losses from all passive activities for the taxable year exceed. This is due to irc sec. 469 g 1 b which states that if a passive activity is sold to a related party any suspended losses attributable to that activity are not deductible at that time. When a taxpayer disposes of the entire interest in a passive activity that activity is no longer subject to the passive activity rules.

This rule also applies to trades of property between related parties defined next under losses on sales or trades of property. Is the gain on the sale truly passive income and entered on irs form 8582 triggering deductibility of unrelated passive losses. If the activity is disposed of in a fully taxable as opposed to tax deferred transaction to an unrelated party both current and suspended passive activity losses generated by that activity as well as any loss on the disposition can be deducted sec. The tax law generally limits a deduction for losses from passive activities to the extent of passive activity income.

Rather the suspended losses remain with the seller until the related party assuming another related party does not acquire the activity the suspended losses become deductible by the original seller. Unused losses are suspended and carried over only to be used to offset passive activity income in future years. Note that one of the criteria requires the disposition be a fully taxable transaction. Current and suspended losses are deducted in a qualified disposition if.

However when there is a qualifying disposition of a passive activity losses from that activity that have been carried over can be claimed in full without regard to passive activity income. Disposing of a passive activity allows suspended passive losses to be deducted. Subparagraph a not to apply to disposition involving related party. A inc is a psc that owns two passive activities a leased office building and a book unit.

The disposition is to an unrelated party. A read as follows. The overall net loss is fully deductible to the extent the taxpayer has basis in the asset. A read as follows.

If all gain or loss realized on such disposition is recognized any loss from such activity which has not previously been allowed as a deduction and in the case of a passive activity for the taxable year any loss realized on such disposition shall not be treated as a passive activity loss and shall be allowable as a deduction against income in the following order. If the taxpayer and the person acquiring the interest bear a relationship to each other described in section 267 b or. This excludes like kind exchanges conversions to personal use gifts transfers incident to divorce transfer due to death and dispositions to related parties. A disposition generally occurs if the taxpayer s entire interest in the activity is disposed of in a fully taxable transaction to an unrelated party sec.

Http Www Jdunman Com Ww Business Sbrg Pdfs Pal Pdf

Irs Releases Final Gilti Regulations Grant Thornton

Instructions For Form 5471 02 2020 Internal Revenue Service

Instructions For Form 8990 05 2020 Internal Revenue Service

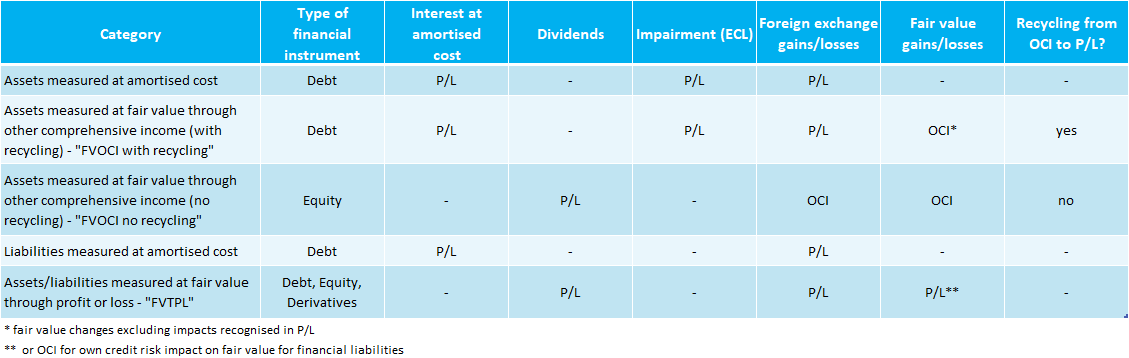

Classification Of Financial Assets Liabilities Ifrs 9 Ifrscommunity Com

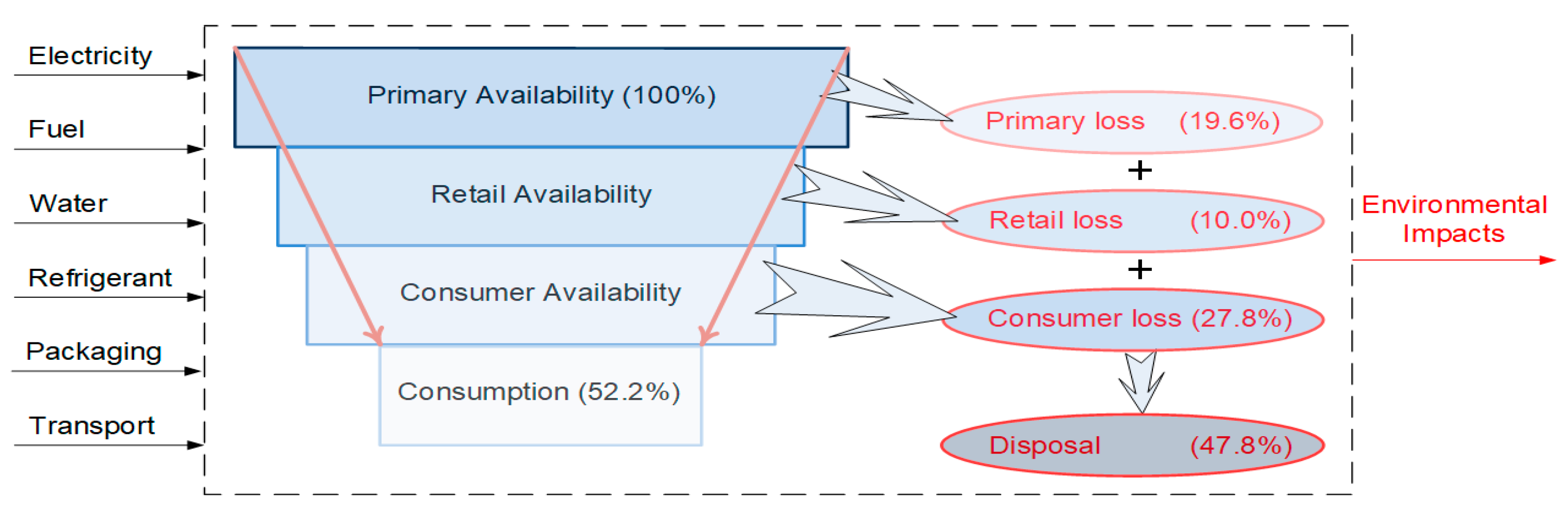

Sustainability Free Full Text Life Cycle Assessment Of Dietary Patterns In The United States A Full Food Supply Chain Perspective Html

Https Www Aicpa Org Content Dam Aicpa Advocacy Tax Downloadabledocuments 20190228 Aicpa Comments On Section 461 L Pdf

My First Ra Bulletin Board Willl Be This But With Questions All Around The Hands With Images College Bulletin Boards Ra Bulletin Boards Ra Bulletins

Publication 570 2019 Tax Guide For Individuals With Income From U S Possessions Internal Revenue Service

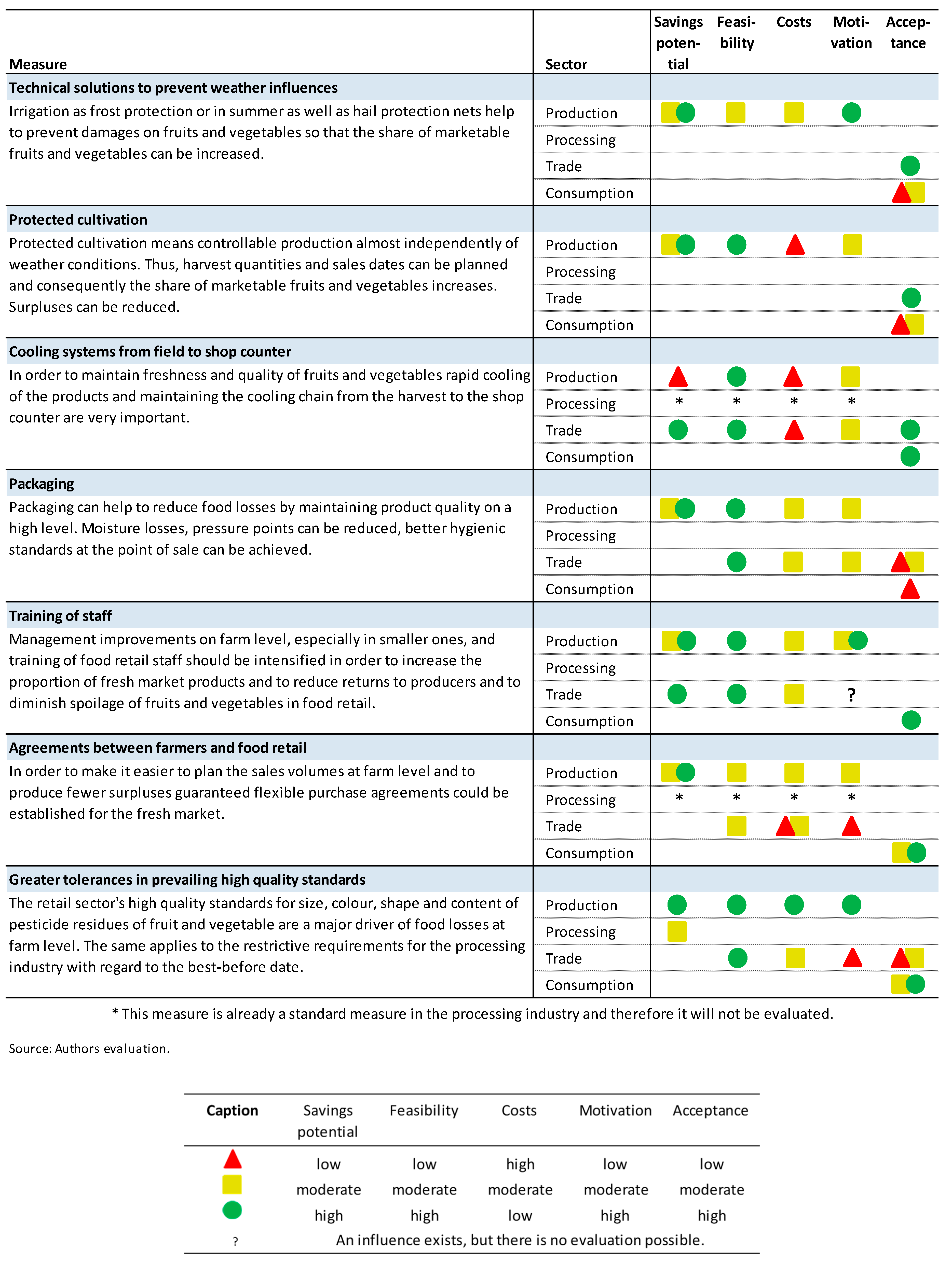

Sustainability Free Full Text Approaches To Reduce Food Losses In German Fruit And Vegetable Production Html

This Year Try Wrapping With Reusable Materials Memories Plastic Free