Passive Activity Loss In California

Pin On Natural Disasters Activities

California S Tax System A Primer

California R D Tax Credit Summary Pm Business Advisors

2019 Personal Income Tax Booklet California Forms Instructions 540 Ftb Ca Gov

Https Www Ftb Ca Gov Forms 2016 16 3885a Pdf

California S Excess Business Loss Deduction May Be Different Than Federal Windes

The passive loss rules stated in irc section 469 c 7 may affect the computation of the corporation s passive loss and credit limitation.

Passive activity loss in california. However when completing the ftb 3801 it looks like you are forced to take the allowable amount of loss 25000 even if you have lit read more. There are 5 properties. This deduction phases out 1 for every 2 of magi above 100 000 until 150 000 when it is completely phased out. Get federal form 8810 corporate passive activity loss and credit limitations for more information.

Under the passive activity rules you can deduct up to 25 000 in passive losses against your ordinary income w 2 wages if your modified adjusted gross income magi is 100 000 or less. I understand that ca conforms to fed passive activity loss rules. California passive activity worksheet see general instructions for step 1 use this worksheet to figure california income loss from passive activities before application of passive activity loss pal rules. Passive activity loss not allowed on california return.

Yes it is regarding rental real estate activities. Enter information for each passive activity on the schedule separately. 11 00 7451193 ftb 3801 2019 side 1 california worksheets attach side 2 to your california tax return. The only other income is 48 interest income yet every tax software i use automatically takes the full 25 000 loss and it is then lost and is not carried forward.

For federal purposes only rental real estate activities of taxpayers engaged in a real property. Step 1 figuring your california passive activity income loss use the california passive activity worksheet on form ftb 3801 side 2 to determine the current year california net income or net loss from each passive activity before application of the pal rules. First line 11 on the ftb 3801 form comes to 26 315 allowable loss which includes the 25 000 allowance and 1 315 passive gain. Passive activity loss rules are generally applied at the individual level but they also extend to virtually all businesses and rental activity in various reporting entities except c corporations.

Pin On Giveaways

An Overview Of California S Research And Development Tax Credit

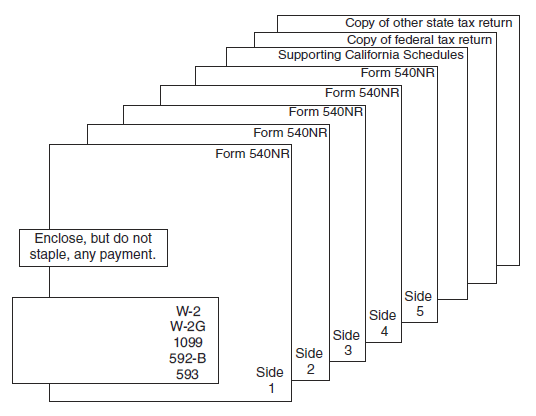

2018 540nr Booklet Ftb Ca Gov

Temperature Monitoring Systems Market Expected To Reach 5 4 Billion By 2024 In 2020 Life Science Marketing System

Wells Fargo Bank Statement Template Free Download Statement Template Credit Card Statement Bank Statement

Https Www Caltax Com Wp Content Uploads 2018 03 Nonresidentsonline Pdf

Rental Ftb Ca Gov

Argentina Bbva Bank Statement Template In Doc Format Fully Editable In 2020 Statement Template Bank Statement Profit And Loss Statement

20 Self Care Routine Ideas To Revitalize Your Body Mind Soul In 2020 Self Care Activities Self Improvement Self

Freshpet Is A Growth Oriented Company With A Great Entrepreneurial Spirit Fun Environment And A Very High Quality Manuf Food Animals Tv Network New Community

Family Night At The Movies Inside Out And Purpose Of Sadness Movie Inside Out Emotions Feeling Down

Can Cacao Actually Help You Sleep Better Cocoa Fruit Cacao Cocoa

Excellent Book For Parents Who Are Divorcing Coping With Divorce Divorce Divorce And Kids