Passive Activity Loss In Year Of Disposition

Understanding Passive Activity Limits And Passive Losses 2020 Tax Update Stessa

Property Management Spreadsheet Excel Template For Tracking Rental Income And Expenses Rental Property Management Rental Property Property Management

Passive Activity Credit Flowchart

Pin On Examples Online Printable Form Templates

Comprehensive Volume Chapte Chapter 11

Security Deposit Itemization Pdf Being A Landlord Property Management Rental Property Management

However special rules apply to dispositions.

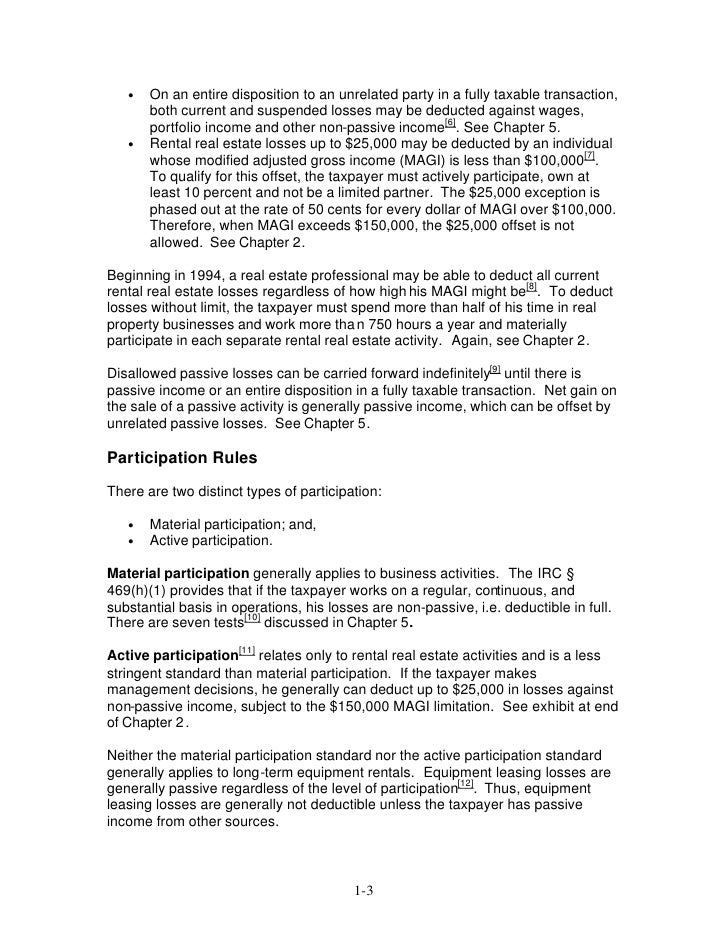

Passive activity loss in year of disposition. If the activity is disposed of in a fully taxable as opposed to tax deferred transaction to an unrelated party both current and suspended passive activity losses generated by that activity as well as any loss on the disposition can be deducted sec. A passive loss allowed from a disposition of a k1 activity will be reported as a nonpassive loss on schedule e line 28. However when there is a qualifying disposition of a passive activity losses from that activity that have been carried over can be claimed in full without regard to passive activity income. When a taxpayer disposes of the entire interest in a passive activity that activity is no longer subject to the passive activity rules.

Unused losses are suspended and carried over only to be used to offset passive activity income in future years. Any gain or loss from the disposition of a passive activity is generally also passive. The passive losses are multiplied by this ratio to generate the current year allowed loss. Unused pals are suspended and carried forward to future years until the taxpayer 1 disposes of the particular activity that generated the losses 2 generates net passive activity income in the case of a personal service corporation or 3 generates net passive activity income or net active income in the case of a closely held corporation.

How do the disposition rules work. Disposing of a passive activity allows suspended passive losses to be deducted. A special rule accomplishes this.

Passive Activity Losses

Https Support Cch Com Kb Solution 000056461

Http Ideaexchange Uakron Edu Cgi Viewcontent Cgi Article 1032 Context Akrontaxjournal

Rental Property Management Template Long Term Rentals Rental Etsy Rental Property Management Rental Property Property Management

Https Www Irs Gov Pub Irs Prior I8582 2018 Pdf

Pin On Individual Taxes

Rental Property Management Template Long Term Rentals Rental Etsy Rental Property Management Rental Property Property Management

Instructions For Form 8995 2019 Internal Revenue Service

Https Www Irs Gov Pub Irs Wd 201428008 Pdf

Https Www Aviation Cpa Com Resource Library Download Cfm X 80

18 Investments Overview Youtube Investing Youtube Math

Rental Real Estate Investors New Excess Business Loss Rule Dallas Business Income Tax Services

2017 Income Tax Fundamentals Chapter 4 By Unicorndreams8 Issuu