Passive Activity Loss Oil And Gas

Oil Amp Gas Industry Mind Map Gas Industry Mind Map Mind Map Template

Tax Benefits From Oil Gas Drilling Investments Explained

The Science Behind Natural Gas Production Compressor Station Oil And Gas Energy

Oil And Gas Investments Tax Deductions Benefits Considerations

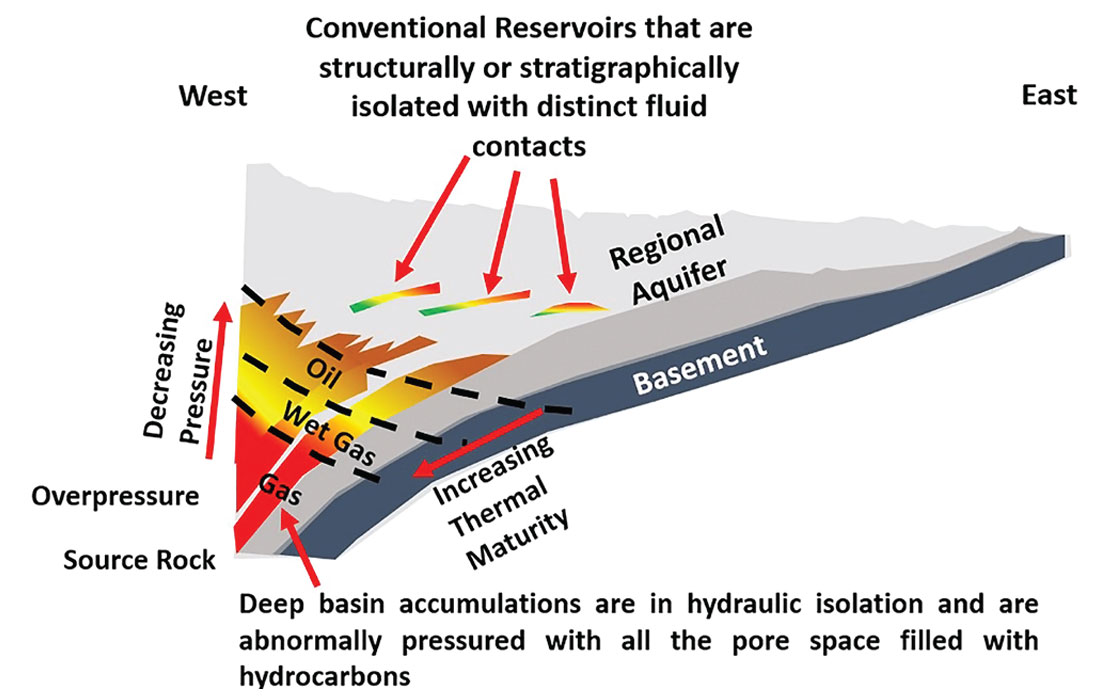

Changes In The Oil Gas Industry Unconventional Plays Engineering Fused With Geoscience Cseg Recorder

Pdf Applying Big Data Analytics To Logistics Processes Of Oil And Gas Exploration And Production Through A Hybrid Modeling And Simulation Approach

Many investors in real estate oil gas partnerships or other partnership entities expect to receive and accumulate passive activity losses.

Passive activity loss oil and gas. By holding an oil and gas working interest in an entity that does not limit liability general partner during the drilling and completion phases the investor may take the idc deduction against non passive income earned or portfolio income. However there is a major exception to the passive loss rules. If i won my oil and gas working interest in an llc is it passive. A passive activity is one that involves the conduct of any trade or business in which the taxpayer does not materially participate.

The passive loss exception enables working interest owners in oil and natural gas production to achieve some parity between their investments and those of corporate shareholders. However losses from working interests in oil and gas property are not subject to the limitation. If all or any part of your passive activity loss is disallowed for the tax year a ratable portion of the loss if any from each of your passive activities is disallowed. Allocation of disallowed passive activity loss among activities.

If any taxpayer has any loss for any taxable year from a working interest in any oil or gas property which is treated as a loss which is not from a passive activity then any net income from such property or any property the basis of which is determined in whole or in part by reference to the basis of such property for any succeeding taxable year shall be treated as income of the taxpayer. A common misconception is that these losses from an oil gas partnership can be used each year to offset earned income from w2 or other active business interests. By counting any working interest investment losses as active instead of passive investors are able to treat the normal business deductions from their investment in. Passive activity loss rules are generally applied at the individual level but they also extend to virtually all businesses and rental activity in various reporting entities except c corporations.

Oil and gas working interest faqs. Capital loss carrybacks and carryovers. 1988 passive activity losses and credits 391 real estate rental activities certain working interests in oil and gas prop erty and limited partnership interests 16 generally a closely held c cor. Any rental activity is a passive activity whether or not the taxpayer materially participates.

October 22 Is World Energy Day A Good Day To Talk About Methane Http Bit Ly 32l4gzc Information Society Methane Greenhouse Gases Gas Industry

What Is The Impact Of Theft Accidents And Natural Losses From Pipelines Gas Pipeline Nature What You Can Do

Oil Gas Investment The Need To Know Tax Basics Baker Tilly

Unconventional Oil Resource An Overview Sciencedirect Topics

Cementing Additives Supplier Corrosion Inhibitor Plant China Drag Reducer Manufacturer Zoranoc Oilfield Chemical Oil And Gas Climates Gas

Https Cyberleninka Org Article N 1486640 Pdf

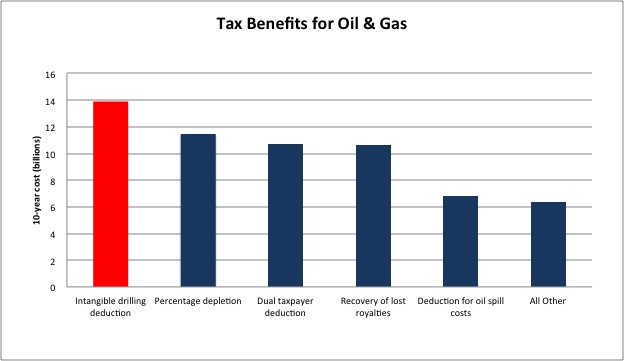

The Tax Break Down Intangible Drilling Costs Committee For A Responsible Federal Budget

Oil And Gas Processing

Pdf Local Content Policy In The Brazilian Oil And Gas Sectoral System Of Innovation

Oil Gas And Offshore Facilities Norphonic

How To Easily Read A Well Log Is Step By Step Approach In Interpreting Any Well Logs This Is A Techni Petroleum Engineering Oil And Gas Science And Nature

Film Former Corrosion Inhibitors For Oil And Gas Pipelines A Technical Review Sciencedirect