Passive Activity Loss Pal Rules

This Worksheet Contains 15 Fill In The Blanks Sentences For Students To Practice The Passive Voice In Spanish It Includes Language Teaching Teaching Sentences

Understanding Passive Activity Limits And Passive Losses 2020 Tax Update Stessa

Http Www Jdunman Com Ww Business Sbrg Pdfs Pal Pdf

Verb Tenses Worksheets Converting Present To Past Verb Tenses Worksheet Verb Worksheets Verb Tenses

Pin On Health Beauty

Inspirational Failure Analysis Report Template Sample With Regarding Template For Evaluation Report In 2020 Report Template Analysis Professional Templates

Passive activity loss rules prevent.

Passive activity loss pal rules. Or schedule e supplemental income and loss as. What are passive activity loss rules. Pal rules are a set of irs rules that stipulate the losses from a passive activity can only be used to offset income or gains generated from other passive activities. Passive income or loss comes from.

The passive activity loss rules are applied at the individual level and extend beyond tax shelters to virtually every business or rental activity whether reported on schedule c profit or loss from business sole proprietorship. Schedule f profit loss from farming. Passive activity loss rules are a set of irs rules that prohibit using passive losses to offset earned or ordinary income. 469 outline seven ways to materially participate in an activity and six exceptions to the definition of a rental activity calculate the passive activity income and losses allowed and the tax.

When you are a passive participant even if the activity is income producing then your involvement is not continual or substantial so. The ratable portion of a passive activity deduction is the amount of the disallowed portion of the loss from the activity for the tax year multiplied by the fraction obtained by dividing. The passive activity loss rules created a special category of income and loss called passive income or loss. There are two types of passive income or loss.

In many instances a comprehensive understanding of these rules by the tax practitioner is required in order to properly handle the complex compliance issues that may arise. This deduction phases out 1 for every 2 of magi above 100 000 until 150 000 when it is completely phased out. The pal rules apply to all business activities but are particularly strict for real estate rentals because they were the primary tax shelter. These rules are known as passive activity loss rules or pal.

Under the passive activity rules you can deduct up to 25 000 in passive losses against your ordinary income w 2 wages if your modified adjusted gross income magi is 100 000 or less. Aii noncorporate taxpayers including pass through entities such as estates and trusts are subject to the passive activity loss pal rules of irc sec. Identify activities subject to the pal rules and the exceptions to them including those for certain real estate professionals define a passive activity rental and trade or business under irc sec.

Assessment Documents And Information For Three Year Old Children Literacy Assessment Preschool Assessment Assessment

Class 4 English Grammar Worksheet 05 English Grammar Worksheets Grammar Worksheets English Learning Spoken

Passive Activity Loss Limitations Working With The Complex Pal Rules Real Estate Tax Issues

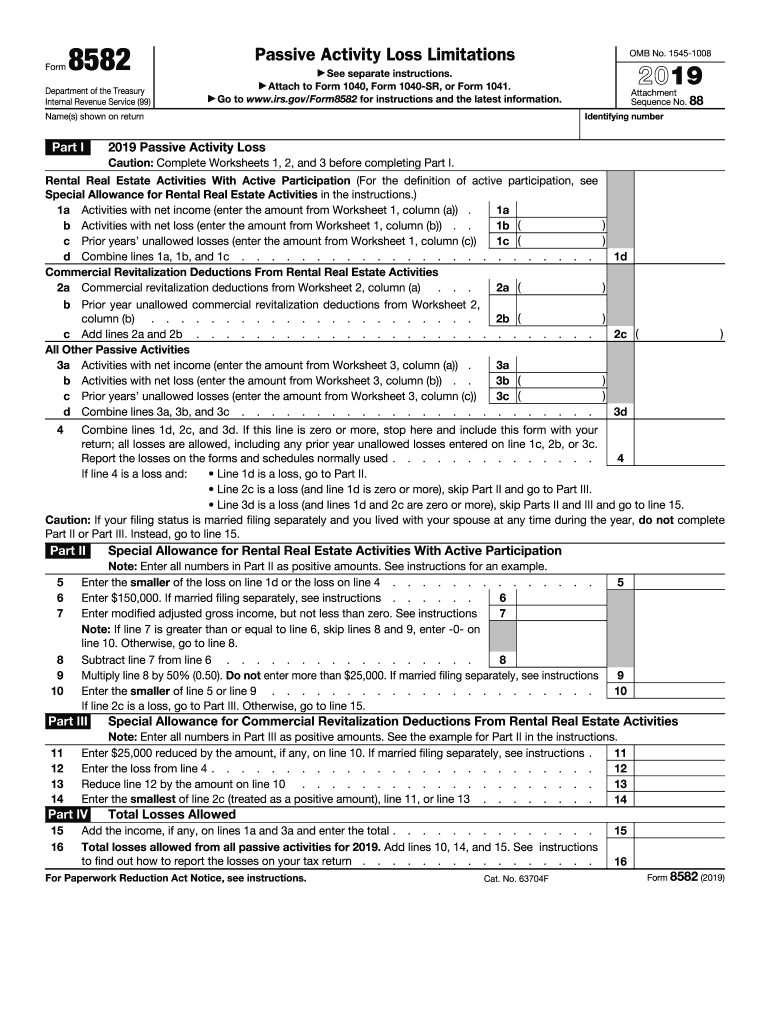

Irs 8582 2019 Fill And Sign Printable Template Online Us Legal Forms

At Risk Limits And Passive Activity Loss Income Tax Course Cpa Exam Regulation Tcja 2017 Youtube

Science Reveals The Most Confusing Emoji Emoji Communication Methods Things To Think About

Apprendreanglais Apprendreanglaisenfant Anglaisfacile Coursanglais Parler In 2020 English Language Learning Grammar Learn English Vocabulary English Language Learning

Mysterious How To Get Rid Of Tooth Decay Dentistselfie Toothdecayroots Dental Health Week Dental Health Health Words

10 Reasons That Will Make You Start A Blog In 2020 How To Start A Blog Successful Blogger Blog

1 Irc 469 Passive Activities Part 4 Definition Of Activity Rental Real Estate With Active Participation Real Estate Professionals Interaction With Ppt Download

What Are Macros And How Do I Calculate Them Keto Diet Book Keto Calculator Keto Macros Calculator

Nrgize Obstacle Course Training 5k Obstacle Course Training Obstacle Race Obstacle Course

5 Minutes Flexibility And Stretching Home Workout Gymguider Com Exercise Yoga Video Workout Workout