Passive Activity Loss Rules Publicly Traded Partnership

Reporting Publicly Traded Partnership Sec 751 Ordinary Income And Other Challenges

Instructions For Form 8582 Cr 12 2019 Internal Revenue Service

Https Www Irs Gov Pub Irs Utl 2017ntf Dealingpartnershipk1 Pdf

Ptps Mlps And Their Pesky K 1s

Http Media Straffordpub Com Products Mastering Reporting Of Publicly Traded Partnership And Mlp K 1s On Partners Returns 2016 01 19 Reference Materials Pdf

Instructions For Form 8995 2019 Internal Revenue Service

You must apply the rules in this part separately to your income or loss from.

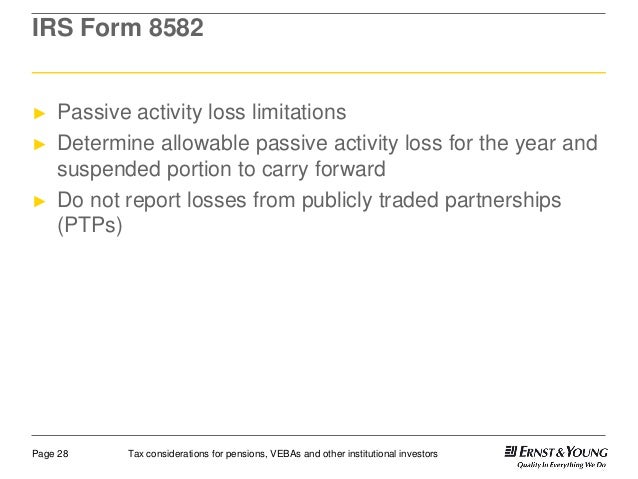

Passive activity loss rules publicly traded partnership. The following rules are useful for determining what to report on the form or schedule from your partnership s income gains and losses on passive activities during the tax year on the owned ptp. Passive activity loss rules for partners in ptps. The loss is not currently allowable due to the passive activity rules. The faq also clarifies that the passive loss limitation issue also spills over into publicly traded partnership qbi calculations.

The passive activity limitations are applied separately for items other than the low income housing credit and the rehabilitation credit from each publicly traded partnership ptp. Instead a passive loss from a ptp is suspended and carried forward to be applied against passive income from the same ptp in later years. You must also apply the limit on passive activity credits separately to your credits from a passive activity held through a ptp. Is it used in computing the reit ptp component.

Begin by tallying up the present year s income losses and gains and any previous year s unallowed losses to determine if the partner has a total gain or loss from the publicly traded partnership. You must apply the rules in this part separately to your income or loss from a passive activity held through a publicly traded partnership ptp. Thus a net passive loss from a ptp may not be deducted from other passive income. Per the instructions for form 8582.

Publicly traded partnerships ptps and the passive loss limitations according to the irs publication 925 there are two sets of rules that may limit the amount of deductive loss from a trade business rental or other income producing activity. The passive activity limitations are applied separately for items other than the low income housing credit and the rehabilitation credit from each publicly traded partnership ptp. Publication 925 passive activity and at risk rules passive activity and at risk rules publicly traded partnership. Do not report passive income gains or losses from a ptp on form 8582.

These losses can be deducted only against passive income of the ptp or when the interest in the ptp is disposed of in a taxable transaction. If the partner s entire interest in the ptp is completely disposed of in a fully taxable disposition any unused losses are allowed in full in the year of disposition. Limited to income from the same ptp excluded from being taken against other types of passive losses suspended and will carry forward until the ptp has income to offset the loss. The losses generated by a ptp that flow through to its partners are passive subject to the passive loss limitation rules.

Thus a net passive loss from a ptp may not be deducted from other passive income. Irs rules treat an overall loss from a publicly traded partnership ptp as passive and an overall gain from a ptp as nonpassive.

Https Www Aviation Cpa Com Resource Library Download Cfm X 80

Pin On Finances

Qualified Business Income Are You Eligible For A 20 Deduction Lexology

Https Www Irs Gov Pub Irs Prior I8582 2018 Pdf

Treasury Issues Final Rules On Partnership Representatives And New Proposed Rules Under The Partnership Audit Regime Tax United States

The Tax Impact On Pension Plans Vebas And More

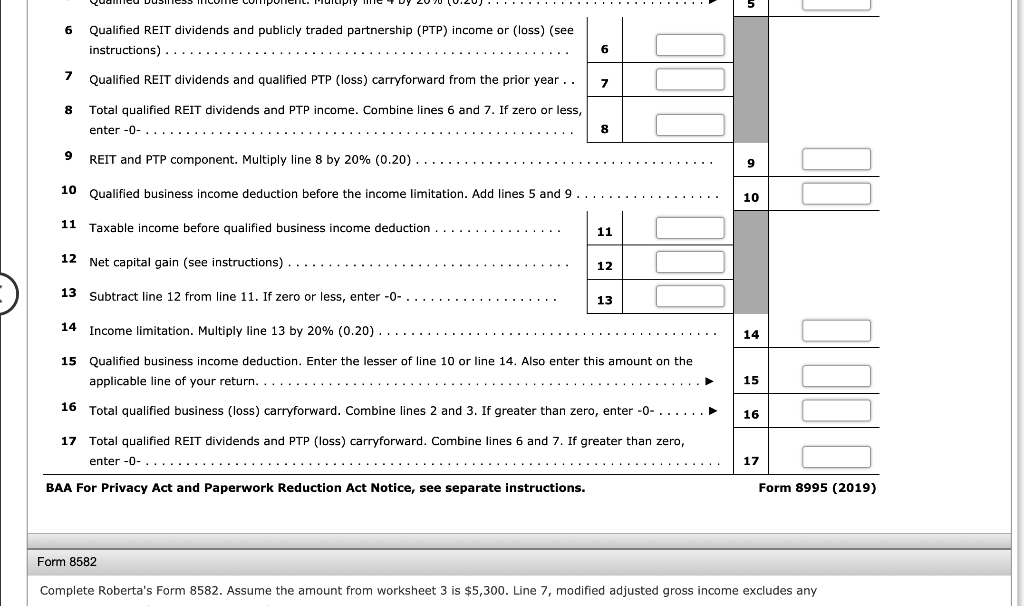

Note This Problem Is For The 2019 Tax Year Rober Chegg Com

Qbi Deduction Frequently Asked Questions Qbi Schedulec Schedulee Schedulef W2

The Pros And Cons Of Investing In Publicly Traded Partnerships Bartlett Pringle Wolf Santa Barbara Accounting Tax Audit Services

Tax Implications Of A Publicly Traded Partnership Investment

Http Scholarship Law Wm Edu Cgi Viewcontent Cgi Article 1372 Context Tax

The Ultimate Guide To Investing In Mlps Seeking Alpha

Https Www Irs Gov Pub Irs Utl 2018ntf Partnership Schedule K 1 Pdf