Passive Activity Loss Special Allowance

Instructions For Form 8582 Cr 12 2019 Internal Revenue Service

What Is The Special Allowance For Rental Real Estate Activities

12 Useful Formulas For Industrial Engineers Poster Industrial Engineering Engineering Quotes Engineering

Pin On Save Money Tips

Passive Activity Losses

Pin Di Business Template

This special allowance is an exception to the general rule disallowing losses in excess of income from passive activities.

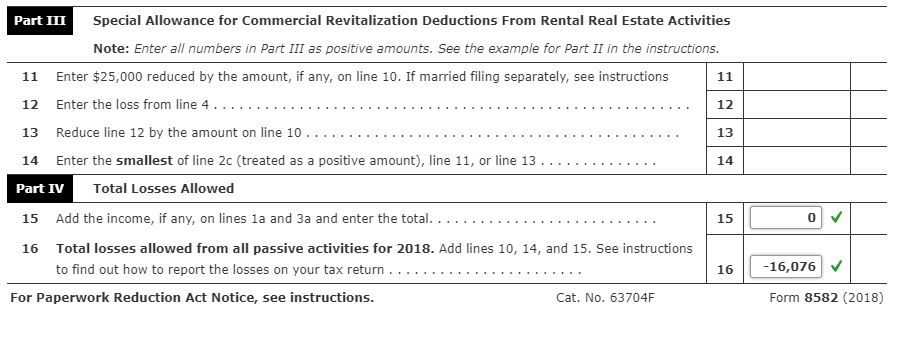

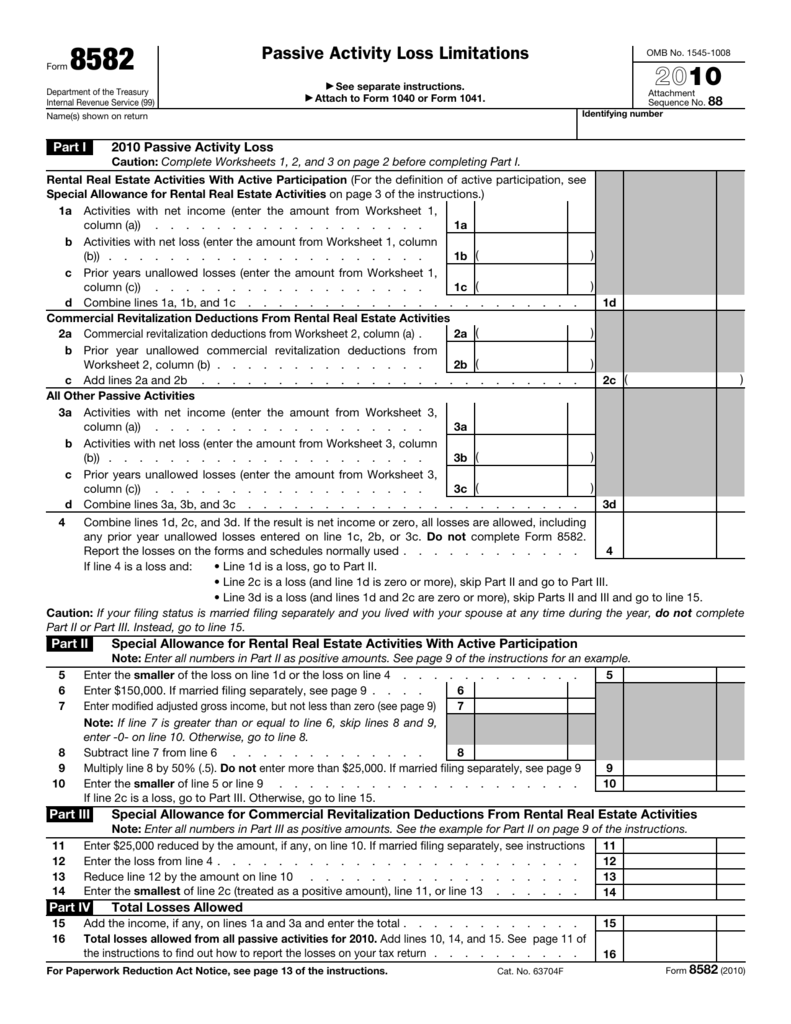

Passive activity loss special allowance. However a special allowance for rental real estate activities may allow some losses even if the losses exceed passive income. This special allowance is an exception to the general rule disallowing losses in excess of income and passive activities. Pals not allowed in the current year are carried forward until they re allowed either against passive activity income against the special allowance if applicable or when you sell or exchange your entire interest in the activity in a fully taxable transaction to an unrelated party. If you or your spouse actively participated in a passive rental real estate activity you can deduct up to 25 000 12 500 for married filing separate filers of loss from the activity from your nonpassive income.

Special 25 000 allowance for real estate nonprofessionals. Modified adjusted gross income for this purpose is your adjusted gross income figured without the following. This is because the special allowance is reduced to 0 since the modified adjusted gross income is over the 100 000 amount. The portion of passive activity losses attributable to the crd.

If you re not a real estate professional a special rule let s you classify up to 25 000 of rental losses as nonpassive. This means you can deduct up 25 000 of rental losses from your nonpassive income such as wages salary dividends and interest. If the property was not disposed ultratax cs would limit the losses on form 8582 in accordance with the special 25 000 allowance rules. 25 000 for single individuals and married individuals filing a joint return for the tax year.

Master Your Family Financial Plan With Passive Income Family Financial Planning Family Money Investing

Forras Pinterest Kayla Itsines 13 Hetes Programja Itt Megtalalsz A Facebookon Is Bo Kayla Itsines Nutrition Kayla Itsines Kayla Itsines Nutrition Guide

I Am Stuck On The Form 8582 I Have The Form 104 Chegg Com

Form 8582 Pillsbury Tax Page

Https Www Reginfo Gov Public Do Downloaddocument Objectid 2340801

Pin Di Business Template

How To Read Income Statement Understand Structure And Contents Income Statement Statement Income

Success Seems To Be Connected With Action Successful People Keep Moving They Make Mistakes But They Don T In 2020 Making Money Quotes Success Rich Kids Of Instagram

Https Www Irs Gov Pub Irs Prior I8582 2018 Pdf

Understanding Passive Activity Limits And Passive Losses 2020 Tax Update Stessa

Food Label Meaning Food Labels Food Labels

Passive Activity Loss Rules And Limitations

If Quote By Rudyard Kipling Jungle Book Author Plaque Zazzle Com In 2020 Jungle Book Quotes Rudyard Kipling Jungle Book If Rudyard Kipling