Passive Income And 199a

Do I Qualify For The 199a Qbi Deduction Myra Personal Finance For Immigrants

Maximizing Your 199a Qbi Deduction As A Specialized Service Business With Images Services Business Business Deduction

Section 199a Qualified Business Income Deduction Qbid Gleim Exam Prep

2019 Tax Deductions Discover If Your Business Qualifies For Section 199a Qualified Business Income To Get Yo Saving Money Tax Deductions Financial Education

Understanding The New Sec 199a Business Income Deduction Kruggel Lawton Cpas

Irs Publishes Final Guidance On The 20 Pass Through Deduction Putting It All Together This Or That Questions Deduction Being A Landlord

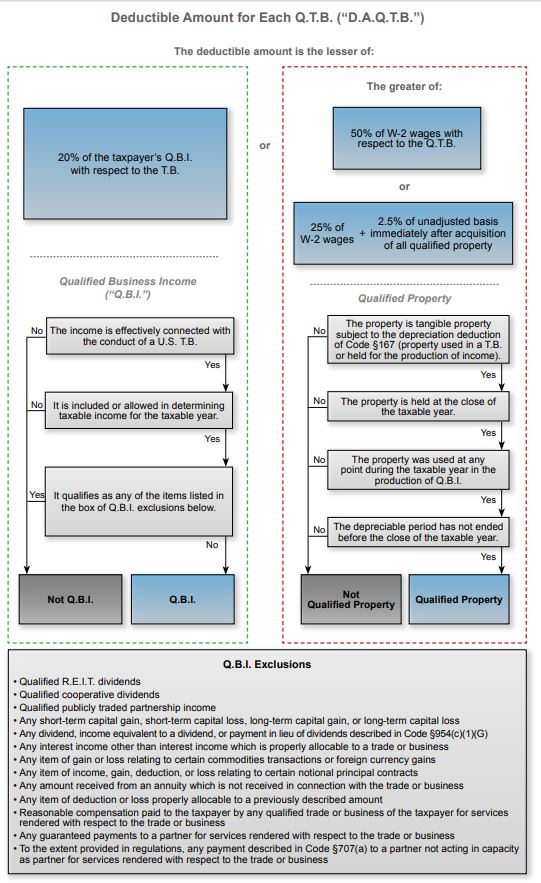

199a which permits owners of sole proprietorships s corporations or partnerships to deduct up to 20 of the income earned by the business.

Passive income and 199a. The proposed 199a rules introduce a new option to aggregate trades and businesses to maximize their 199a deduction. This aggregation would be separate from any grouping already in place for other tax provisions. In addition any losses disallowed before jan. The motivation for the new deduction is clear.

1 2018 are never taken into account for the qbi deduction. To allow these business owners to keep pace with. Consider the following scenario. With the enactment of legislation known as the tax cuts and jobs act the act 1 on dec.

Passive activity losses and sec. Niit was enacted to impose a medicare surcharge on passive income. However this 20 deduction found in new internal revenue code 199a is saddled with exclusions phase outs technical issues and uncertainties so that many well meaning non corporate. The section 199a only applied to qualified business income qbi which was generally defined as income from a qualified trade or business other than a specified service trade or business or the performance of.

In a nutshell roughly 97 of your clients have taxable income under the threshold so their deduction is equal to 20 of domestic qualified business income from a pass through entity subject to the overall limit based on taxable income roughly 3 of your clients are impacted by the threshold the deduction is phased out based on 1040 taxable income unless. After the issuance of proposed regulations in irc 199a commenters immediately looked for parallels between niit and qbi. In addition the section 199a deduction cannot exceed the ceiling limit of 20 of her total net income or the total marital net income if she and her spouse file a joint return so that losses. Passive income qualify for 199a.

Passive income qualify for 199a. When the 199a was first passed tax professionals didn t think it would apply to passive income from holding rental property. Passive activity losses pals are not taken into account for the qbi deduction if they are disallowed. Many taxpayers already group activities in response to the passive activity loss rules and the net investment income tax rules.

Section 199a was added to the internal revenue code under the tax cuts and jobs act of 2017 to provide taxpayers with a 20 deduction from income attributable to qualifying trades or businesses.

How Business Owners Get Preferential Tax Rates With 199a Qbi Deduction Production Income Https Www Kitces Com Blog 199a Deduction Tax Rate Financial Planning

199a Tax Rules For Qualified Business Income Qbi Bader Martin

Qbi Deduction Frequently Asked Questions Qbi Schedulec Schedulee Schedulef W2

Opportunity Funds Deferred And Tax Free Gains In 2020 Tax Saving Investment Investing Tax

Choice Of Entity Calculus Modified By Tax Reform In Light Of The Qualified Business Income Deduction Irc Section 199a Lane Powell Pc

199a Further Explored Qualified Business Income And Rental Arrangements

Harshwal Company Llp

Https Www Incpas Org Docs Default Source Course Materials February Qbi Rons Final Version With Toc Pdf

Farm Rental Agreements Under 199a

Qualified Business Income Are You Eligible For A 20 Deduction Lexology

Https Www Irs Gov Pub Irs Utl 2019ntf 01 Pdf

Section 199a 20 Deduction Explained With Examples Tax Cuts And Jobs Act 2017 Cpa Exam Reg Youtube

Does Rental Income Qualify For The New 20 Section 199a Deduction