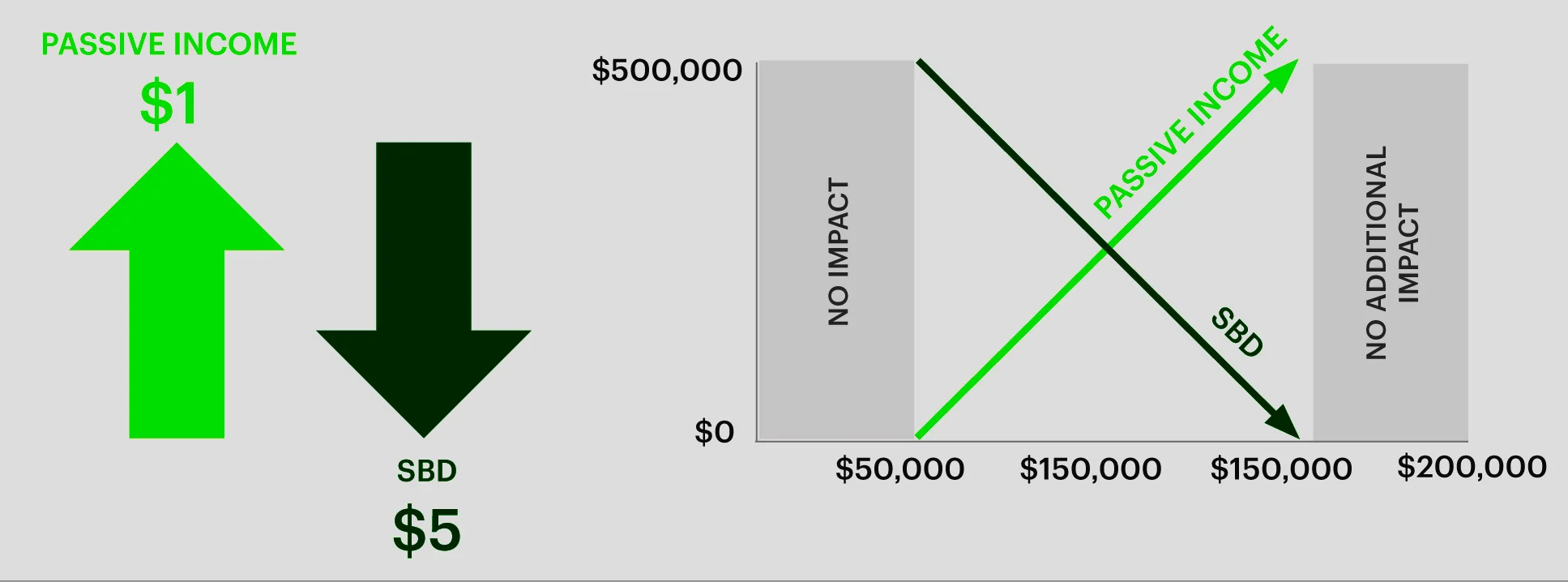

Passive Income And Sbd

Pin On Awesome Blog Posts

Pin On Awesome Blog Posts

Upvoting Services Bots And More Steemit Work From Home Jobs Online Money Making Opportunities Money Management

Pin On Lukedunham Com

How To Create A Website With Wix A Free Website Builder Passiveincomeideas Org Earn Passive Income While Sleeping Website Builder Free Free Website How To Start A Blog

Survey Junkie Review 2020 Can You Earn Legit Money In 2020 Make Money Now Money Habits Online Side Jobs

Canadian controlled private corporations cpcc can apply the small business deduction sbd to some active business income.

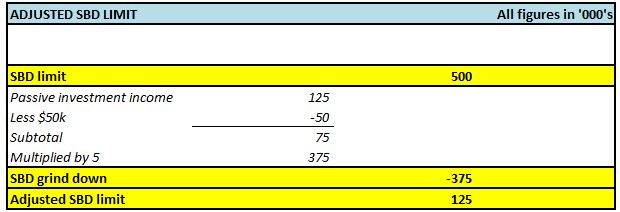

Passive income and sbd. Once passive investment income earned by the associated group exceeds 150 000 the ability to claim sbd is eliminated for the entire group. For every 1 of passive income earned over a new 50 000 threshold by an associated group of companies the sbd limit will be reduced by 5. Both companies have a december 31 year end. For every 1 of passive income earned over the new 50 000 threshold by an associated group of companies the sbd limit will be reduced by 5.

What is passive income and why does it matter. Owner managers can potentially avoid the passive income sbd grind in paragraph 125 5 1 b when triggering corporate capital gains by winding up and dissolving the corporation holding the investments in the same year. The consequences to a company claiming the sbd and having more than 50 000 of passive income in the year are limited to a loss of a deferral of tax 80 000 as shown in the example above and a relatively small increase in the integration cost of earning active business income in a corporation approximately 1 percent in the example above. That is private corporations that earn greater than 50 000 of passive income inside the corporation.

Under the new rules passive investment income earned by a ccpc can have a negative impact on the corporation s ability to claim the sbd. After much consideration and consultation as to how to best curb the accumulation of wealth through passive income strategies inside a corporation the government settled on utilizing the small business deduction sbd to impose the penalty.

Dqmwppcilde5mcs6nuxplscxxbtmuvqvrjenefhgx9b25rg 1 680 3 350 Pixels Infographic Blockchain Cryptocurrency Data Visualization

Simple Bookkeeping Spreadsheet Double Entry Bookkeeping Bookkeeping Spreadsheet Template Spreadsheet Business

The Small Business Clawback Wiim

83 41 Growth How To Buy Hxy Money Hxy A Step By Step Guide In 2020 Fiat Money Buy Bitcoin Blockchain

Yek Mining Limited In 2020 Kids Rugs Decor Home Decor

Earning Passive Investment Income Inside Your Company Carson Law Real Estate Corporate Wills Poas Intellectual Property Burlington Hamilton Milton Oakville Lawyer

Air Jordan 1 Low Black Toe 553558 116 Release Date Sbd Air Jordans Jordan 1 Black Jordan 1 Low

Don T Be Passive About Canada S New Passive Income Rules Advisor S Edge

Assam Irrigation Department Recruitment 2020 Apply For 643 Engineer And Other Posts Irrigation Assam Gov In In 2020 Recruitment Irrigation How To Apply

Our Investment Strategy Sbd Housing

New Sbd Limit Rules And The Impact On Professional Practices

Level 10 Life Level 10 Goals Boho Berry Planner Bullet Journal Goals Bullet Journal Bullet Journal Inspiration

Pin On How To Earn Cryptocurrencies Like Bitcoin Ethereum Litecoin Bitcoincash Dogecoin Dash Etc