Passive Income Impact On Small Business Deduction

Best Of Passive Income Strategies Passive Income Strategies Passive Income Income

How To Add Passive Income To Your Business Five Design Co In 2020 Passive Income Design Income

Pin By P Mo On Business With Images Investing Money Business Motivation Money Mindset

Income Tax Changes For 2018 Atkins E Corp Business Tax Deductions Income Tax Small Business Tax Deductions

Pin On Tax Planning

Maximizing Your 199a Qbi Deduction As A Specialized Service Business With Images Services Business Business Deduction

A ccpc s passive income business limit reduction for a particular taxation year will be the amount determined by the formula.

Passive income impact on small business deduction. The small business deduction saved this corporation 65 000 in taxes. Passive income reduces the small business deduction. In 2019 the company will earn 500 000 of active business income. In canada a lower tax rate is available for canadian controlled private corporations ccpcs on the first 500 000 of income it actively earns from a.

Above 500 000 the general federal tax rate is 15. If a corporation earns more than 50 000 of passive investment income in a year the amount of income eligible for the small business tax rate is reduced and more of its active income is taxed at the general corporate rate. A corporation can have up to 50 000 of investment income in the prior year with no impact to the small business deduction. For ontario the small business limit is 500 000.

The draft legislation also contained minor amendments to other provisions relating to the taxation of passive income. The small business limit the amount of income annually eligible for the small business rate is 500 000 federally and in most provinces. Most significantly a corporation that earns more than 50 000 of investment income will suffer a reduction in its small business deduction limit the grind for taxation years beginning after 2018. Companies of this size will be wholly taxed at the corporate rate.

Up to 500 000 the ontario tax rate is 3 5 and above 500 000 it is 11 5. Passive investment income and its impact on the small business deduction april 17 2018 the recent federal budget proposed changes the proposals that will restrict access to the small business deduction sbd for many corporations. Had the full corporate tax rate of 26 5 been applied the tax obligation would have been 265 000 26 5 of 1m. That cumulative deduction 5 off for every 1 over 50 000 means that businesses making more than 150 000 in passive income won t be able to apply the small business tax rate at all.

To illustrate the impact of these cra passive income changes let s assume we have a ccpc with a december 31 fiscal year end. The method proposed by the federal government is to reduce access to the small business tax deduction for corporations earning considerable passive investment income on a straight line basis. Bl is the ccpc s business limit otherwise determined for the particular year i e its business limit as described above. The budget introduces a new eligibility mechanism for the small business deduction based on a canadian controlled private corporation s ccpc passive investment income.

There is a new limitation on the 500 000 small business deduction based on a company s previous year s passive income. In 2018 the company earned 100 000 of passive investment income.

Have You Ever Wondered How Poshers Are Filling Out Their Income Tax Return Forms Do You K Small Business Tax Deductions Business Tax Deductions Tax Deductions

Tips To File Self Employed Taxes Perfect For Small Businesses And Bloggers Understand Deductions And How The Tax La Small Business Tax Business Tax Tax Money

Don T Be Passive About Canada S New Passive Income Rules Advisor S Edge

Pin On Running A Business Llc

Are Blogging Courses Worth It In 2020 Impact Freedom In 2020 Blogging Courses Blog Tools Blogging Advice

Online Sales Taxes An Explanation Of The Changes And How You Re Affected Small Business Tax Business Tax Deductions Business Tax

Does My Llc Need To File A Tax Return Even If It Had No Activity Business Tax Deductions Tax Return Small Business Tax Deductions

Major Sales Tax Changes For Small Business Owners Small Business Tax Deductions Business Tax Deductions Business Tax

Pin By Dylen Mccrumb On Budget Financing Etc Bust Investing Money Business Money Money Financial

The New Instagram Algorithm And How To Benefit From It Instagram Algorithm Instagram Marketing Tips More Followers On Instagram

Https Advisors Td Com Saverio Veltri Mediahandler Media 313770 410 18 Passive Investment Income En1 Pdf

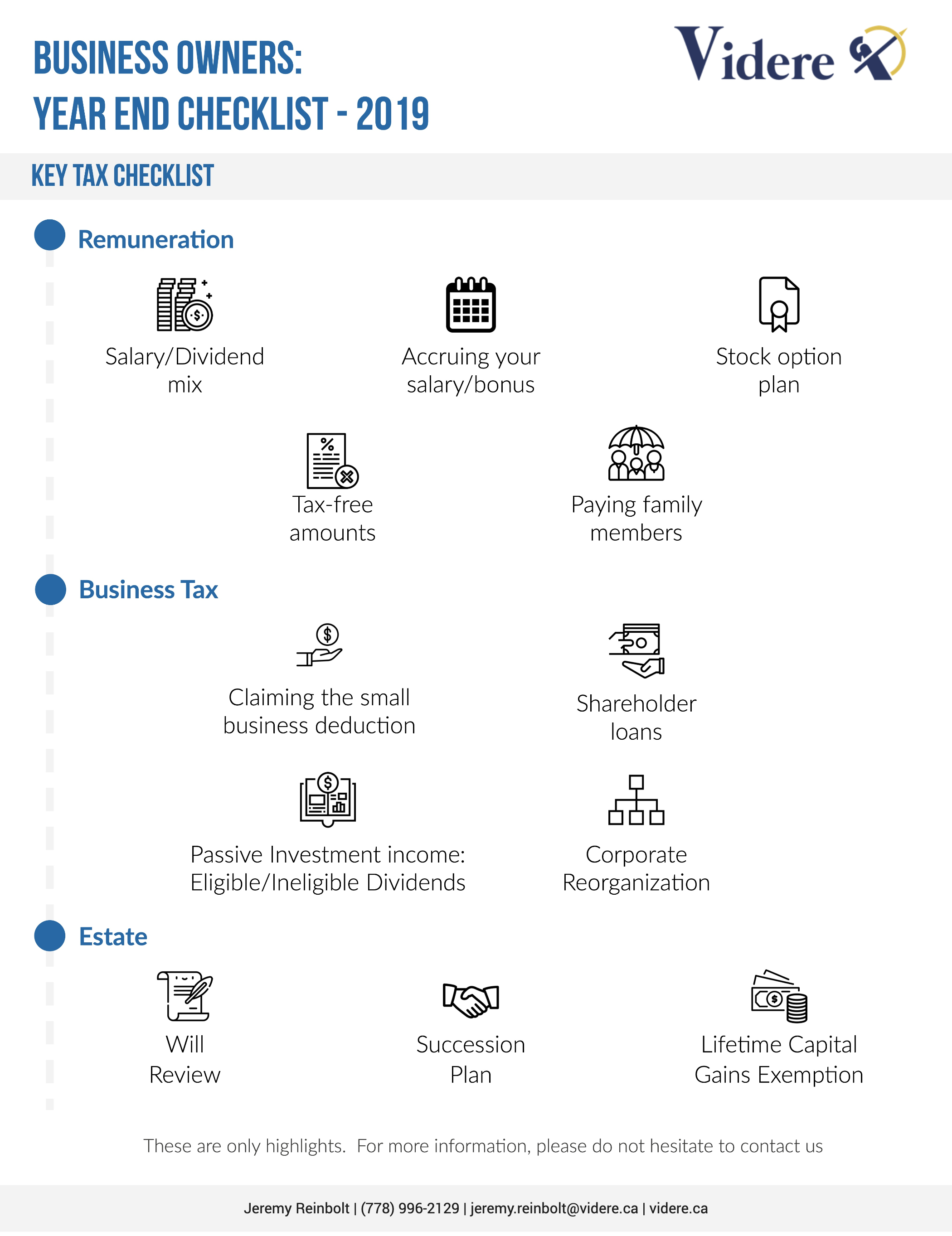

Business Owners 2019 Tax Planning Tips For The End Of The Year Videre

The Top Ways To Build Passive Income Sources Profit Raid Your Internet Marketing Guide Small Business Bookkeeping Bookkeeping Business Accounting Career