Passive Investment Income Ato

Https Www Ato Gov Au Law View Pdf Pbr Lcr2018 D007 Pdf

Https Www Ato Gov Au Assets 0 104 1328 1465 048880dc 66cc 45f3 Bd56 B22c232762a9 Pdf

Certainty At Last For Base Rate Entities Or Not Taxbanter Blog

Https Www Ato Gov Au Uploadedfiles Content Mei Downloads Tp40264nat06692014 Pdf

Https Www Ato Gov Au Uploadedfiles Content Cs C Downloads N5806 11 2014 Js21554 Fen Pdf

Company Tax Rates Atotaxrates Info

Coffee and cake pty ltd is the owner of a small cafe.

Passive investment income ato. The ruling takes a broad view of the meaning of carrying on a business which will extend to companies that hold mainly passive assets such as shares or property as long as its activities are carried out with a view to making a profit. When working out the rate to use when franking your distributions you need to assume that your aggregated turnover assessable income and base rate passive income will be the same as the previous year. Because this income is only 3 8 of its assessable income happy feet pty ltd is a base rate entity for the 2019 20 income year and the 27 5 company tax rate applies. The ato has issued a final tax ruling tr 2019 1 which replaces its previous views expressed in tr 2017 d7.

Example 2 base rate entity. Corporate entities which hold passive investments such as rental properties as they could not satisfy the first eligibility requirement of carrying on a business. You must declare investment income on your tax return. This includes interest bonuses dividends rent you receive capital gains on assets sold and income or credits from trust investments.

The interest income is base rate entity passive income.

Https Www Ato Gov Au Uploadedfiles Content Mei Downloads 39823n83840614 Pdf

Https Www Aph Gov Au Documentstore Ashx Id 3b59820a A5a7 4a4a 86d5 Ed52b429d4b5 Subid 303094

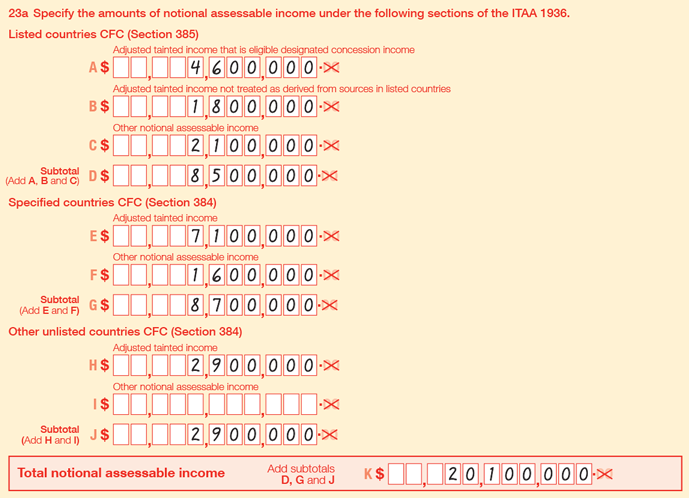

Question 23 Australian Taxation Office

Chapter 3 Taxation Of Foreign Dividends And Branch Profits Australian Taxation Office

Item 32 Non Concessional Mit Income Ncmi Partnership Return Ps Help Tax Australia 2020 Myob Help Centre

Https Www Ato Gov Au Law View Pdf Pbr Tr2018 Cp005 Pdf

Passive Investment Companies Tax Rate Still 30 Rubin Partners

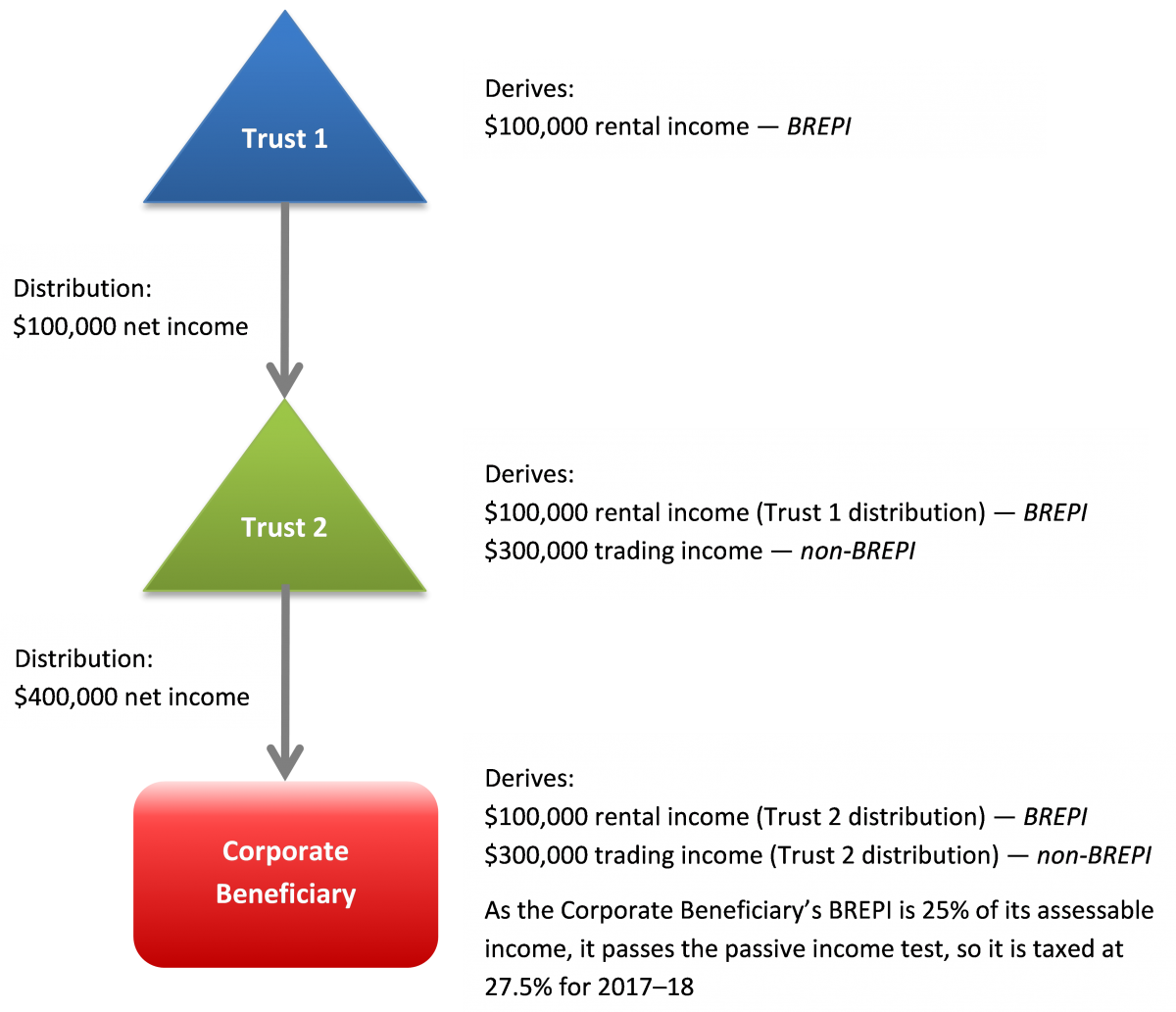

How Bucket Companies Work In Family Trusts

Https Treasury Gov Au Sites Default Files 2019 03 C2017 T240634 Deloitte Pdf

Part 3 Working Out Attributable Income And The Amount To Include In Your Assessable Income Australian Taxation Office

Https Www Myob Com Content Dam Public Website Docs A P Tax Seminars 2020 Myob 2020 Tax Eseminars Slides Pdf

Https Www Ato Gov Au Uploadedfiles Content Cas Downloads 45331 Refund Js33528 Pdf

Dominion Stock Analysis Energize Your Investments Investing Money Dividend Stocks Dividend Investing