Passive Investment Income Termination

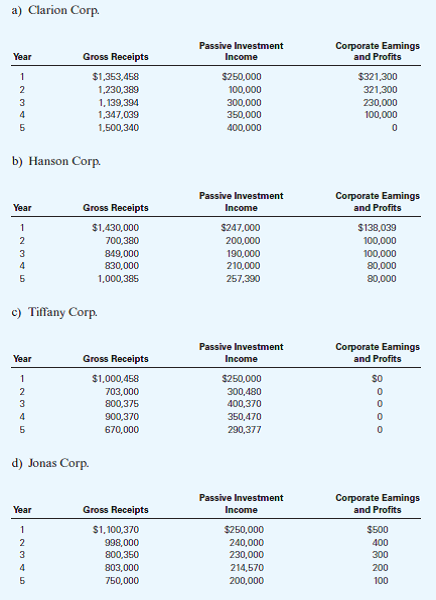

Solved Assume The Following S Corporations And Gross Receipts Chegg Com

Chapter 22 S Corporations Ppt Download

2013 Cch Basic Principles Ch16 Piv

Http Www Irs Gov Pub Irs Wd 201523008 Pdf

Partnerships And S Corporations Ppt Download

Https Www Ftb Ca Gov Tax Pros Procedures S Corp Handbook S Corp Chapter 4 Pdf

In financial terms passive income describes money that a one time investment continually generates without requiring the investor to monitor or adjust their holdings.

Passive investment income termination. Staff reports november 20 2020. Analysis under certain circumstances an s corporation may face two problems from having passive investment income pii. For example if an s corporation earns 100 000 in a year 35 000 of which is from passive income the total passive income percentage for the year would be 35 percent. And one of the most profitable investments out there is staking a claim in dividend aristocrats.

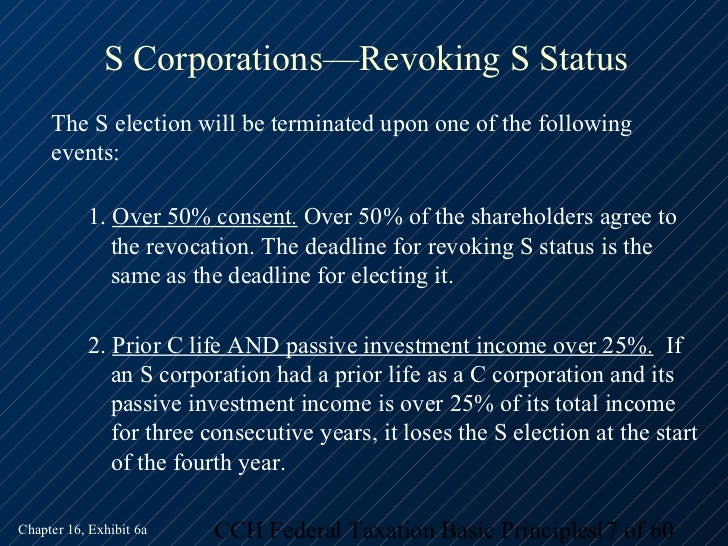

1 imposition of a separate corporate level tax on excess passive income and 2 eventual termination of s status if excess passive income is received for three consecutive years. Passive investment income is generated when an s corporation earns income by an activity it is not directly involved with or participated in. If the business does generate more than 25 percent of its receipts from passive income the excess is taxed at the highest corporate income rate. The passive investing.

It can grow an individual s wealth in more ways than one. Any termination under this paragraph shall be effective on and after the date of cessation. And if you invest 14 000 you will get 7 a day by 2030 from 3 a day in 2020. This is a tried and true passive income investment strategy.

Passive income investment no. 3 where passive investment income exceeds 25 percent of gross receipts for 3 consecutive taxable years and corporation has accumulated earnings and profits a termination i. An example of passive investment income is dividends. 5 steps for living off dividends forever.

A termination for this reason can be considered to be inadvertent as discussed below. Investing for passive income. Passive investment income is any income that is generated by an activity that the business did not directly participate in. The other way the business may lose its status is if over the past three tax years it derived more than 25 percent of its gross income from passive investment income.

Passive income exceeds the passive investment income limitation if the s corporation has accumulated earnings and profits at the close of each of three consecutive tax years this would occur only if the corporation or its predecessor had been a c corporation. Since this is investment u we re going to focus on the more practical investment side of things.

Https Www Irs Gov Pub Irs Wd 202005004 Pdf

Https Www Jstor Org Stable 25094490

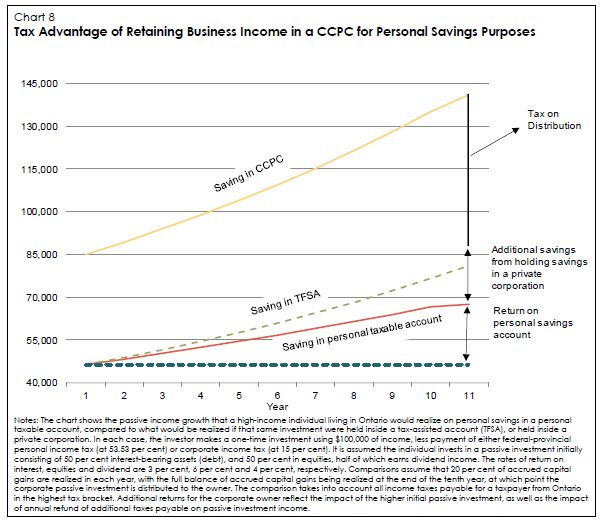

Is It Time To Reexamine Your Corporate Structure Tax Canada

Termination Payment Was Ordinary Gain For Taxpayer

Http Www Irs Gov Pub Irs Prior P589 1994 Pdf

Https Checkpointlearning Thomsonreuters Com Courses Filedownload Courseidhiddenfield 11401 Deliveryformatidhiddenfield 5

Https Www Bradfordtaxinstitute Com Endnotes Irc Section 1362f Pdf

Http Scholarship Law Wm Edu Cgi Viewcontent Cgi Article 1302 Context Tax

Pin On Affiliate

Http Www Saepc Org Assets Councils Southernarizona Az Library Handout 20 20gorin 20business 20structuring 20materials Pdf

Https Www Revenue Ie En Tax Professionals Documents Notes For Guidance Tca Part04 Pdf

Https Www Ftb Ca Gov Tax Pros Procedures Multistate Audit Technical Manual Chapter 4000 Pdf

Https Checkpointlearning Thomsonreuters Com Courses Filedownload Courseidhiddenfield 1480 Deliveryformatidhiddenfield 5