Passive Loss Carryover Rules

150 000 Income 150 Income Tax Income Tax Student Loan Interest Income

Grammar Used To Grammar Prepositional Phrases Learn English English Language Learning Grammar

Solved Tax Drill At Risk And Passive Loss Limitations A Chegg Com

Https Www Irs Gov Pub Irs Pdf F6781 Pdf

Https Www Irs Gov Pub Irs Utl 2019ntf 01 Pdf

Understanding Your Schedule K 1 And Real Estate Taxes Crowdstreet

Passive losses can be written off only against passive gains.

Passive loss carryover rules. Passive losses can include a loss from the sale of the passive business or property in addition to expenses exceeding income. A passive loss carryover is created when you have more expenses than income a loss from passive activities in a prior year that could not be used that year. What is a passive loss carry over. This deduction phases out 1 for every 2 of magi above 100 000 until 150 000 when it is completely phased out.

Aii noncorporate taxpayers including pass through entities such as estates and trusts are subject to the passive activity loss pal rules of irc sec. The internal revenue service places limits on passive losses the type that arise from activities you engage in on the side essentially as an investor. Under the passive activity rules you can deduct up to 25 000 in passive losses against your ordinary income w 2 wages if your modified adjusted gross income magi is 100 000 or less. Instead the passive loss is carried forward to future tax years to offset any passive income.

Passive activity loss rules are a set of irs rules stating that passive losses can be used only to offset passive income.

2019 Year End Tax Planning Individuals Ohio Tax Firm

What Is A Passive Loss Carry Over Finance Zacks

Https Www Irs Gov Pub Newsroom Tcja Training Provision 11012 Limits On Losses Pdf

Instructions For Form 8990 05 2020 Internal Revenue Service

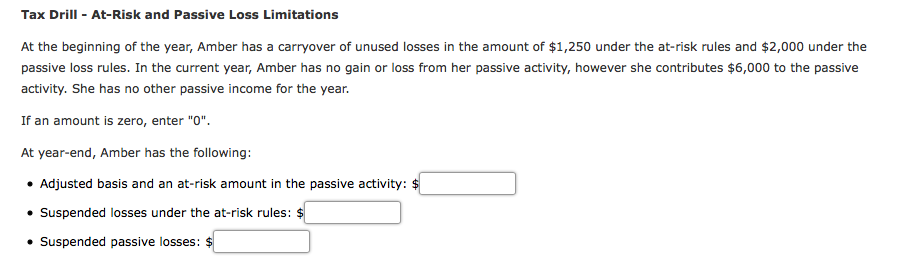

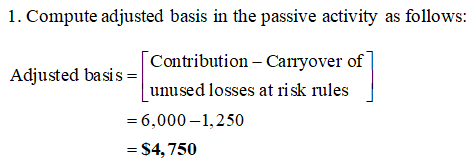

Answered At The Beginning Of The Year Amber Has Bartleby

August 20 21 2019 At Disney S Coronado Springs Resort In Orlando Florida Data Analytics Analytics Coronado Springs Resort Disney

Modified Adjusted Gross Income Under The Affordable Care Act Updated With Information For Covid 19 Policies Uc Berkeley Labor Center

Deducting Pass Through Business Losses

Https Static Store Tax Thomsonreuters Com Static Samplepages Real Estate Owners And The New Limitation For Active Losses Under The Tcja Journal Of Real Estate T Pdf

How To Use Tax Loss Carryforward On Your Rental Property Millionacres

Office Area Basementideas Basement Living Rooms Basement Home Office Home

/IRSForm8949-d55e89f19d8043719e68055fdd8dad41.jpg)

Dacr1dchjhbt5m

You Can T Take It With You Passive Activity Loss Carryovers At Death