Passive Rental Income And Qbi

199a Further Explored Qualified Business Income And Rental Arrangements

Https Encrypted Tbn0 Gstatic Com Images Q Tbn And9gctpoabm Skaj62v8jjmv6aumsi3oqdbdv0vyg Usqp Cau

Safe Harbor Clarifies Qbi Deduction For Some Rental Properties Taxing Subjects

Irs Issues Final Section 199a Regulations And Defines Qbi Dental Cpa Dental Consulting Dentist Taxes

Qbi Deduction Frequently Asked Questions Qbi Schedulec Schedulee Schedulef W2

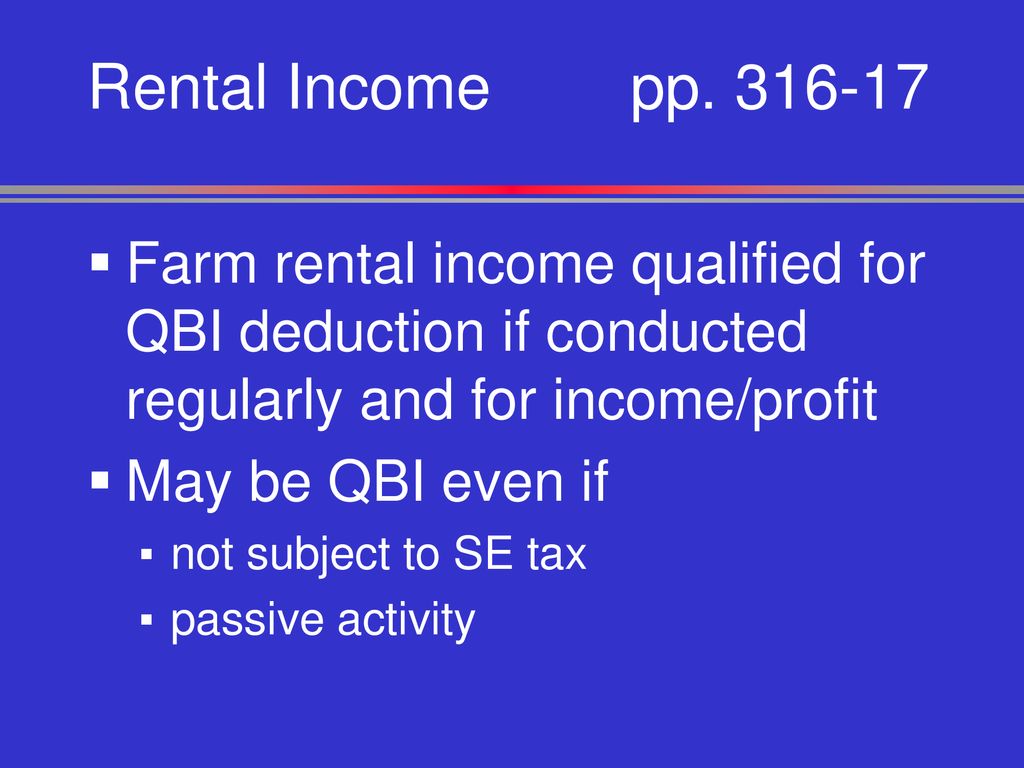

Farm Rental Agreements Under 199a

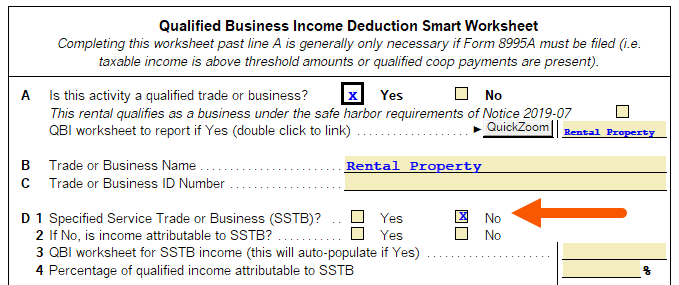

The irs issued notice 2019 07 concurrently with the final qbi regulations.

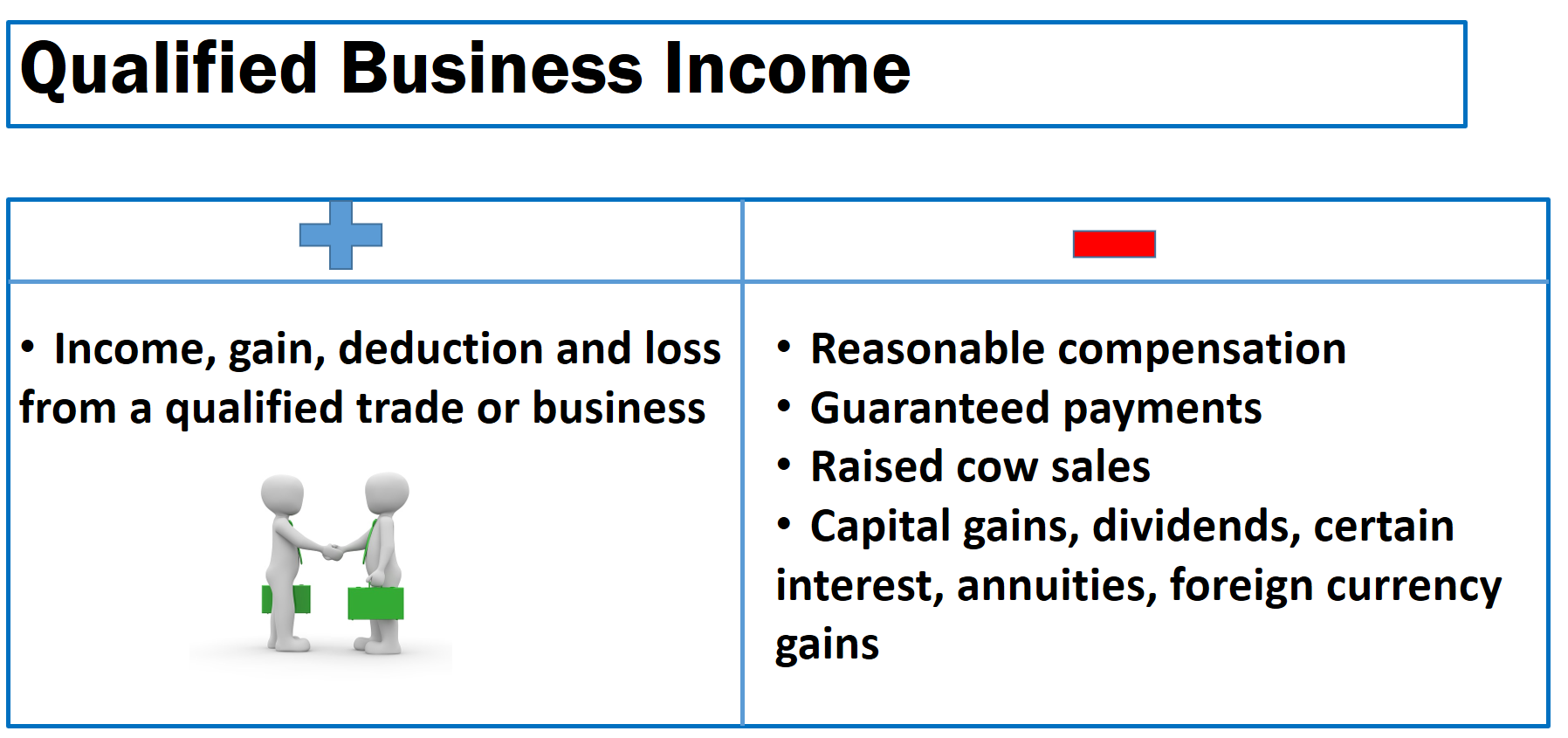

Passive rental income and qbi. 2019 38 can be treated as a trade or business for qbid purposes. The irs has expanded qualified business income qbi frequently asked questions to provide additional information on the relationship between rental real estate and the qbi deduction qbid. For example owning only commercial rental real estate is typically considered a trade or business because of the level of. With the qbi deduction most self employed taxpayers and small business owners can exclude up to 20 of their qualified business income from federal income tax.

The 2017 pal is the older previously disallowed pal and is otherwise allowed against passive income in the current tax year. The net rental income from partnership a is deemed qbi. How qualified business income qbi affects rental income tax reform will change the way rental income is taxed to landlords beginning in 2018. It provides proposed safe harbor requirements for a rental.

Although real estate has some favorable provisions compared to w2 income. Typically rental real estate activity is classified as passive with income and expenses reported on schedule e form 1040 instead of schedule c form 1040. A rental real estate enterprise that meets the safe harbor requirements discussed in notice 2019 07 and rev. However because it is carried over from a pre 2018 tax year it is disregarded for purposes of determining qbi.

Rental real estate as passive income. There are some aspects that bother me. Passive rental activities that are not considered a trade or business for example a single family dwelling rented out for a year or more in which there is little or no interaction between the landlord and the tenants other than periodically collecting rent and the occasional repair. Some rental activity may qualify as a trade or business.

However the rental income is specified service income because partnership b is an sstb and the two partnerships are commonly owned.

My Last Stab At Farm Rents As Qbi Cla Cliftonlarsonallen

Https Www Irs Gov Pub Irs Utl 2019ntf 01 Pdf

Irs Clarifies Whether Rental Real Estate Qualifies For Qbi Taxing Subjects

Rental Activities The Qualified Business Income Deduction Dermody Burke Brown

Instructions For Form 8995 2019 Internal Revenue Service

The 20 Qualified Business Income Qbi Deduction And Self Rentals And You Bartleyfinancial

How To Enter And Calculate The Qualified Business Intuit Accountants Community

Irs Publishes Final Guidance On The 20 Pass Through Deduction Putting It All Together Deduction Irs Guidance

Irs Draft Form 8995 Instructions Include Helpful Qbi Flowchart Center For Agricultural Law And Taxation

More Rental Real Estate Businesses Can Qualify For Qbi Deduction Frazier Deeter Llc Frazier Deeter Llc

Does Rental Real Estate Qualify For Section 199a Qbi Deduction Acap Advisors Accountants

Agricultural And Natural Resource Issues Chapter 9 Pp Ppt Download

Rental Property Krs Cpas