Do Passive Loss Rules Apply To Corporations

Can You Deduct Your S Corporation Losses Passive Activity Loss Rule

Investment Risk In Mutual Fund Investing Infographic Investing Infographic Mutual Funds Investing Investing

Starting Your Own Corporation Can Be More Costly And Time Consuming Than Other Business Types Read Our Five Legal Tips T Business Format Business Legal Advice

Business Feasibility Study Checklist Businessdegree Mbadegree Booksworthreading Marketing Business Management Business Analyst

Fx Childs Play Signals Review Does It Really Work Affiliate Product Review Forex Trading How To Get Rich Trading Quotes

Investment Guides Make Money Today How To Make Money Money Today

Nonpassive income for this purpose includes interest dividends annuities.

Do passive loss rules apply to corporations. Portfolio income interest dividends royalties etc mldr. 5 closely held corporations. Passive losses only deductible against passive income i e. The most important limitations regard basis at risk limitations and active and passive loss rules.

The court acknowledged that the passive loss rules do not refer to s corporations at all. Not deductible against ordinary income or portfolio income 1. You can t deduct the excess expenses losses against earned income or against other nonpassive income. They do apply to individuals partners shareholders of s corporations closely held c corporations and personal service corporations.

Losses must clear all three of these hurdles to be used by owners. Even though the rules don t apply to grantor trusts partnerships and s corporations directly they do apply to the owners of these entities. Casualty losses considered to be business related casualty losses are deductible in full by a corporation and are not subject to a 100 reduction. The losses can generally be used to offset the individual s profits.

Passive activity rules apply to individuals estates trusts other than grantor trusts personal service corporations and closely held corporations. For information about personal service corporations and closely held corporations including definitions and how the passive activity rules apply to these corporations see form 8810 and its instructions. An associated regulation defining certain passive activities including rental activities specifies. For the passive activity rules a corporation is a per sonal service corporation if it meets all of the following requirements.

There are however limitations on the ability of individuals to use or employ these losses. They specifically apply to taxpayers who are individuals estates trusts closely held c corporations and personal service corporations. 1 it is not. Even though the rules do not apply to grantor trusts partnerships and s corpo rations directly they do apply to the owners of these entities.

Passive loss rules may affect. Passive loss limits do not apply to corporations except personal service corps and closely held corporations partnership partners can deduct passive loss only to the extent of passive income limited partners losses are passive by definition s corp passive loss limits may also limit loss deductions depending upon the nature of the corporate business and the shareholders participation in. If the ventures are passive activities the passive activity loss rules prevent you from deducting expenses that are generated by them in excess of their income. The passive loss rules generally do not apply to c corporations 1.

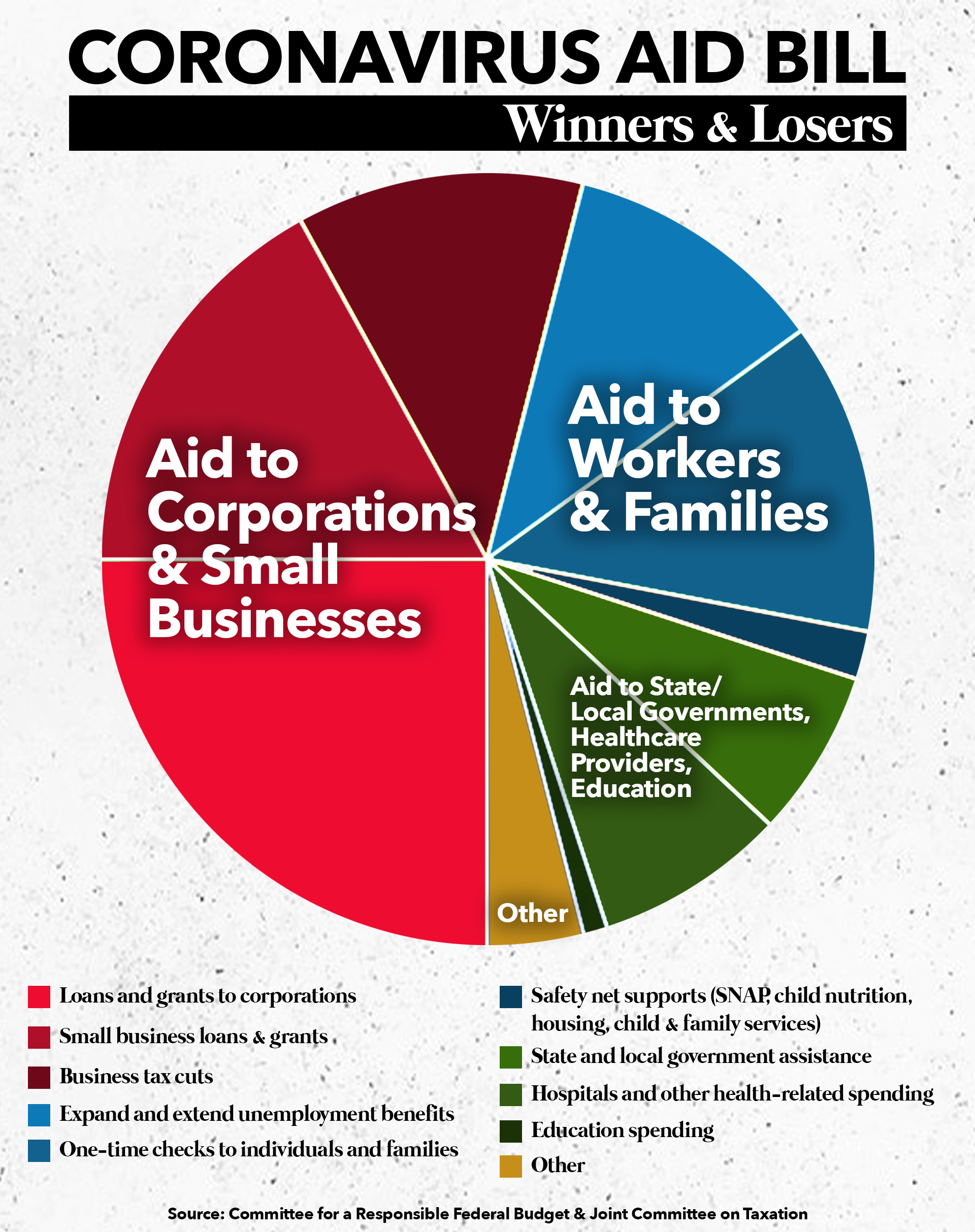

Summary Of Major Tax Provisions In The Senate And House Coronavirus Stimulus Bills Americans For Tax Fairness

Pin On Residual Income Is Important

The Act Allows Flow Through Businesses In New Jersey Such As Sub S Corporations Partnerships Llcs Or Sole Proprietorsh In 2020 Tax Services Tax Rules Tax Deductions

Pin Pa Health Recipes

Infographic What You Need To Know About Real Estate Investing With A Self Directed Ira Real Estate Infographic Real Estate Investing Real Estate Tips

10 Business Tax Write Offs That Will Save You Money Business Tax Tax Write Offs C Corporation

Small Business Accounting Cheat Sheet Important Info Small Business Accounting Small Business Tax Business Account

Which Business Entity Is Right For You Financial Services Business Ownership Business

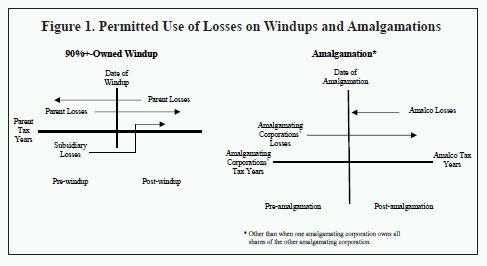

Using Tax Losses Within A Corporate Group Tax Canada

Determining The Taxability Of S Corporation Distributions Part I S Corporation Business Training Corporate

Should You Invest Investing For Beginners In 2020 Investing Marketing Coaching Value Investing

Pfics Rules Initial Impressions And Observations Kpmg United States

Secret Find Out Why I Don T Invest In Individual Stocks Anymore You Ll Learn About My Lazy Investing Approach Best Way To Invest Investing Stock Market