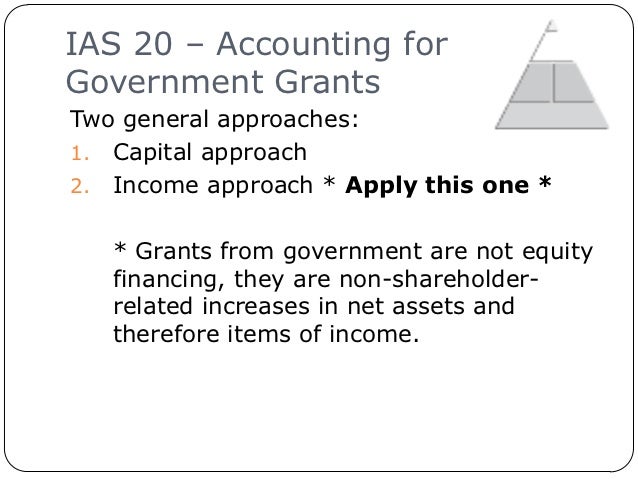

Income Approach Government Grants

As 12 Accounting For Government Grants

Ias 20

How To Account For Government Grants Under Ind As 20

How To Launch Your First Passive Income Funnel In 5 Days Essential Hustle Blogging Essentials Marketing Approach Email Marketing Services

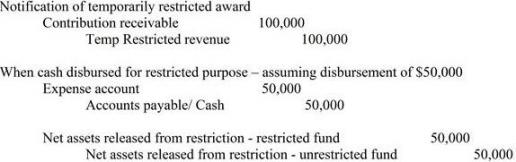

Accounting For Government Grants Sample Journal Entries Nonprofit Accounting Basics

Ifrs Government Grants Grant Thornton Insights

According to para 12 ias 20 requires entities to use income approach which is as follows.

Income approach government grants. Government grants are recognised in profit or loss on a systematic basis over the periods in which the entity recognises expenses for the related costs for which the grants are intended to compensate which in the case of grants related to assets requires setting up the grant as deferred income or deducting it from the. Capital approach versus income approach. Income approach the key assumption is that grants from government are not equity financing they are non shareholder related increases in net assets and therefore items of income. It must be noted that the accounting treatment of a government grants must be based upon the nature of grant itself.

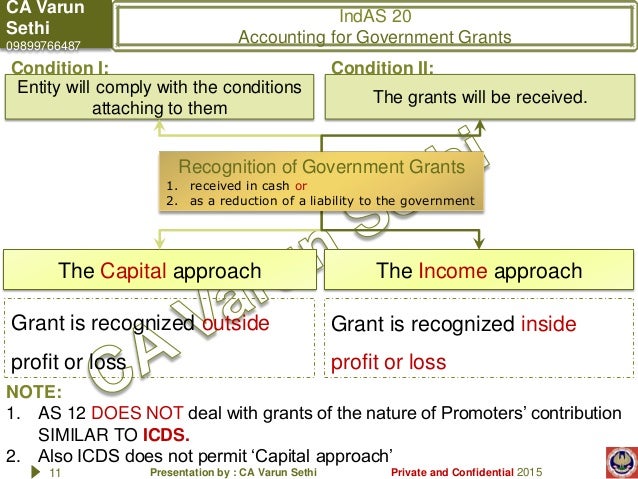

Government grants shall be recognised in profit or loss on a systematic basis over the periods in which the entity recognises as expenses the related costs for which the grants are intended to compensate. Thus grants that have attributes similar to those of promoters contribution must be treated as a part of the shareholders fund. Ias 20 outlines how to account for government grants and other assistance. Two broad approaches may be followed for the accounting treatment of government grants.

As per income approach grants should be recognized.

Dental Financial Assistance Programs Grants Free Care Financial Assistance Dental Bill Dental

5 Things Not To Say In Grant Applications Grant Application Grant Writing Business Grants

Quick Guide Ias 20 Accounting For Government Grants Paul Wan Co

Pin By Theresa Harley On Grant Proposal Writing In 2020 With Images Grant Writing

Pin On Financial

Government Grants Under Ias 20 Chartered Education

Government Grants Government Assistance Ias 20 Ifrscommunity Com

Ca Varun Sethi Ind As 20 Accounting For Government Grants

Accounting For Government Grants Pdf Free Download

Financial Aid Programs Government Assistance More Financial Aid Benefit Program Federal Loans

Just Started A Business Understand Your Tax Obligations The U S Small Busine Small Business Resources Small Business Start Up Small Business Administration

Ias 20 Accounting For Government Grants Part 1 2 Youtube

Pros And Cons Of Government Intervention Economics Help