Income Approach Ifrs 13

Ifrs 13 Fair Value Measurement Video Lecture Part 4 Acca Online Accounting Teacher Accounting Notes Fair Value

New Ifrs 13 Fair Value Measurment

Pin On Karetan

Pin On Book

Impairment Of Financial Assets Ifrs 9 Ifrscommunity Com

Telecharger International Financial Reporting A Practical Guide Pdf Gratuit De Alan Melville Telecharger Votre Accounting Student Financial Free Textbooks

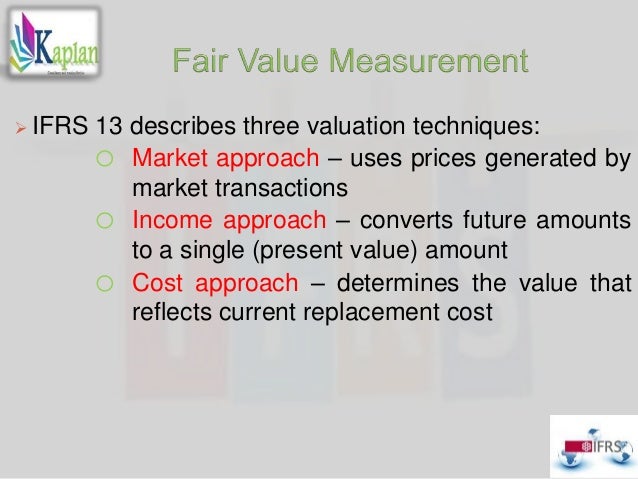

Ifrs 13 introduces a fair value hierarchy that categorizes inputs to valuation.

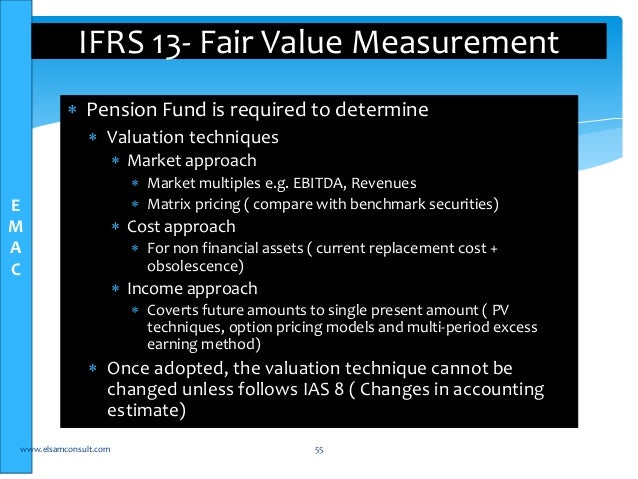

Income approach ifrs 13. Cash flows or income and expenses to a single current i e. Income approach the income approach converts future amounts e g. A defines fair value b sets outin a single ifrs a framework for measuring fair value and. Ifrs 13 fair value measurement 1 introduction fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly.

12 ifrs 13 states that when measuring fair value the objective is to estimate the. When a quoted price for the transfer of an identical or a. This is a complex process and so ifrs 13 sets out a valuation approach which refers to a broad range of techniques which can be used. Considered within the context of materiality as defined in international financial reporting standards ifrss.

Income approach 34 discounted cash flow dcf method 35. The standard defines fair value on the basis of an exit price notion and uses a fair value hierarchy which results in a market based rather than entity specific measurement. Ifrs 13 fair value measurement detailed review wednesday april 2. Income approach or market approach.

There are three approaches based on the market income and cost. As a result the classification as level 1 level 2 or level 3 became required for non financial assets and liabilities measured at fair value and disclosures of fair values in the notes to the financial statements. When the income approach is used the fair value measurement reflects current market expectations about those future amounts. Ifrs 13 applies when another ifrs requires or permits fair value measurements both initial and subsequent or disclosures about fair value measurements except as detailed below.

Ifrs 13 fair value measurement ifrs 13. Ifrs 13 applies to ifrss that require or permit fair value measurements or disclosures and provides a single ifrs framework for measuring fair value and requires disclosures about fair value measurement. The income approach converts future amounts e g. Income approach converts future amounts cash flows or income and expenses to a single current discounted amount reflecting current market expectations about.

77 using another valuation technique i e. The fair value measurement is determined on the basis of the value indicated by current market expectations about those future amounts. Ifrs 13 expanded the guidance on assessing fair value measurements within the three levels of the fair value hierarchy. Converts future amounts e g.

Cash flows or income and expenses to a single current i e. It is technique which is used for valuation under which fair value is based on the estimated future net cash inflows of an asset and those estimated future net cash inflows are determined from the market participant s point of view.

Pin On Solution Manual Download

Https Www Iasplus Com En Publications Global Ifrs In Focus 2013 Ifrs In Focus Ifrs13 At Download File Ifrs 20in 20focus 20 20valuation 20methodologies Pdf

Ifrs For Dummies Ebook Rental

Excel Inventory Template Inventory Spreadsheet Template For Excel Product Tracking Excel Inve Spreadsheet Template Project Management Templates Excel Templates

Ifrs For Pensions Schemes Emac

Lovely Sample Nursing Assessment Forms 7 Free Documents In Pdf In 2020 Nursing Assessment Assessment Head To Toe

Understanding Mergers And Acquisitions In The 21st Century Ebook Rental In 2020 Merger 21st Century Understanding

Applying Ifrs In Real Estate

Ppt International Financial Reporting Standards Ifrs Powerpoint Presentation Id 1642929

Ifrs 17 First Approach

Pin On Test Bank

Ifrs Training Module

Pin On Test Banks Solution Manuals