Income From Discontinued Operations Ifrs

Ifrs 5 Discontinued Operations Acca Financial Reporting Fr Youtube

Acca P2 Ifrs 5 Discontinued Operations Youtube

Ppt Ifrs 5 Discontinued Operations Powerpoint Presentation Free Download Id 5351309

Non Current Assets Held For Sale And Discontinued Operation Ifrs 5 Hkfrs Ppt Download

Discontinued Operation

Ifrs 5 Non Current Assets Held For Sale And Discontinued Operations

If the entity presents profit or loss in a separate statement a section identified as relating to discontinued operations is presented in that separate statement.

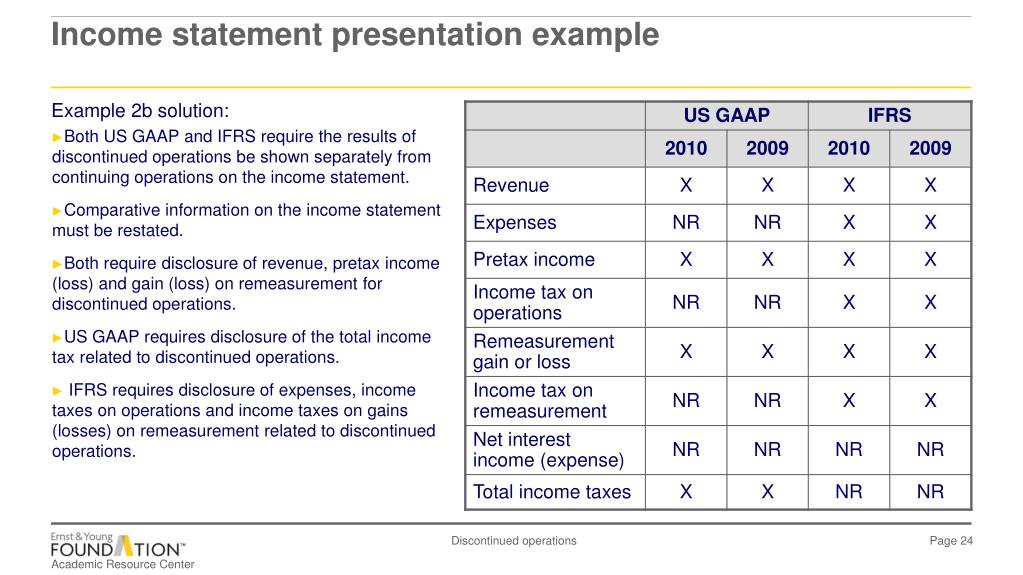

Income from discontinued operations ifrs. Income or loss from discontinued operations is a line item on an income statement of a company below income from continuing operations and before net income. Is this mandatory in case of discontinued operations. The sum of the post tax profit or loss of the discontinued operation and the post tax gain or loss recognised on the measurement to fair value less cost to sell or fair value adjustments on the disposal of the assets or disposal group is presented as a single amount on the face of the statement of comprehensive income. The international accounting standards board iasb ceased recognizing extraordinary items under ifrs rules in 2002.

Only incremental directly attributable costs excluding finance costs and income tax expenses are included in costs to sell. However it specifically scopes out deferred tax assets ias 12 pension assets ias 19 financial assets ifrs 9 investment property ias 40 biological assets ias 41 and insurance assets ifrs 17. If an entity ceases to classify a component of an entity as held for sale the results of operations of the component previously presented in discontinued operations are reclassified and included in income from continuing operations for all periods presented ifrs 5 36. According to your guidance the presentation of result from discontinued operations is not included as such in the income statement but in the comprehensive income staement.

Or ifrs international financial reporting standards. If the asset or disposal group is not a discontinued operation the amount is presented within continuing operations and is disclosed as an impairment loss recognized on classification as held for sale. Oh and one more question. Any income from discontinued operations is also presented separately.

Discontinued operations must be recorded separately in compliance with the accounting regulatory standards such as gaap generally accepted accounting principles gaap gaap generally accepted accounting principles is a recognized set of rules and procedures that govern corporate accounting and financial reporting in the us. Summary of ias 35 objective of ias 35. Ifrs seems to speak about the comprehensive income statement only. 2 the ifrs has a separate disclosure required for income or expenses of.

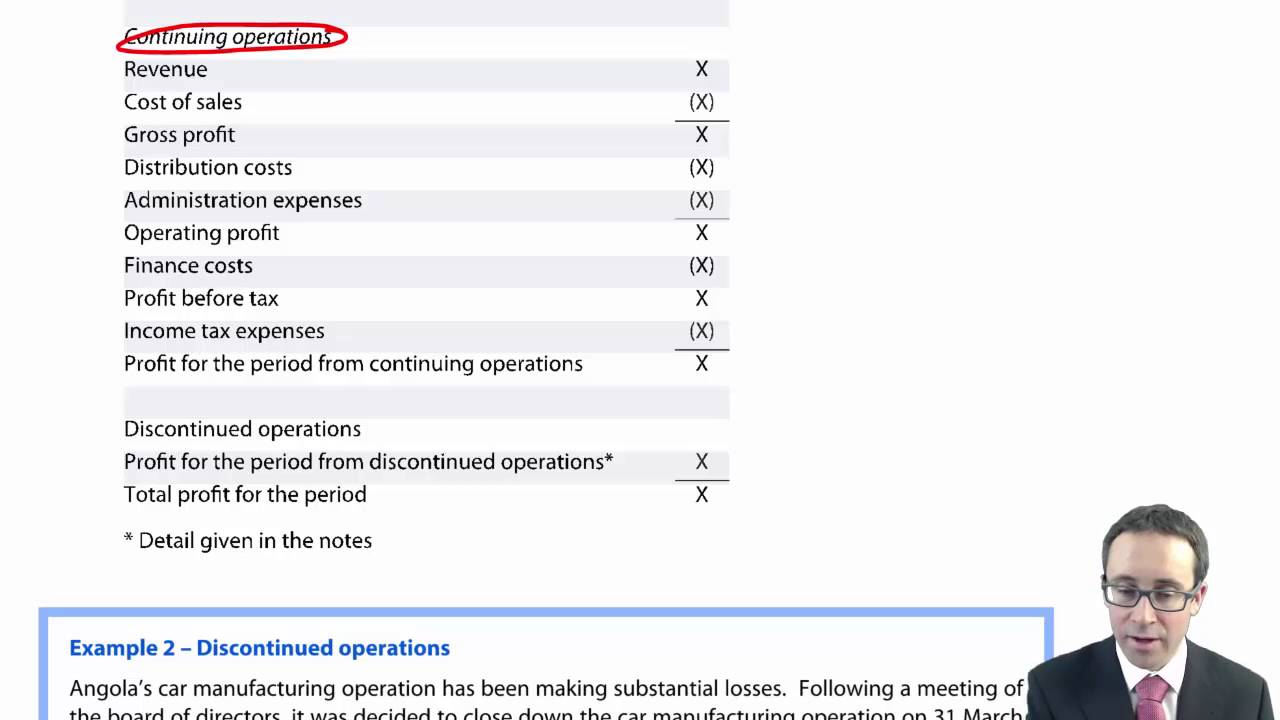

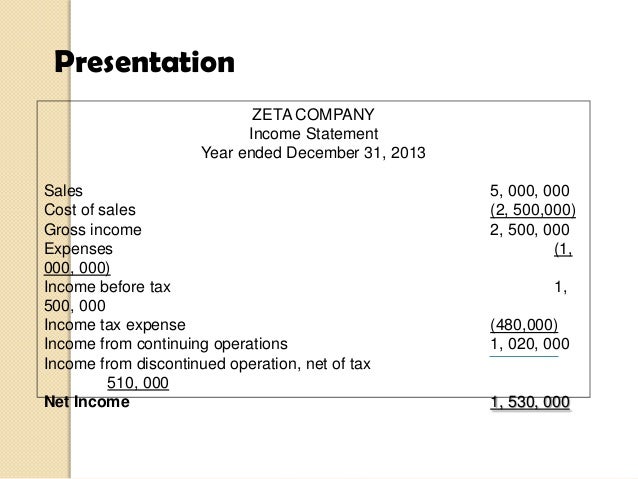

The total gain or loss from the discontinued operations is thus reported followed by the relevant income taxes. When i lookup guidance from a big4 firm they note that the income statement should reflect the result form discontinued operations as well. The objective of ias 35 is to establish principles for reporting information about discontinuing activities as defined thereby enhancing the ability of users of financial statements to make projections of. It represents the after tax gain or loss on sale of a segment of business and the after tax effect of the operations of the discontinued segment for the period.

Ch 4 The Income Statement Comprehensive Income Chegg Com

Ifric 17 Para 15 Ifrs 5 Gain On Distribution Of Non Cash Assets Disclosed On Face Of Income Statement Discontinued Disclosures Accounts Examples

Topic 1 Tangible Non Current Assets Ppt Download

Discontinued Operations Ifrs 5 Ifrscommunity Com

Https Www Mnp Ca Siteassets Media Pdfs Miscellaneous 2017 03 Ifrs 5 Snapshot Final Pdf

Ifrs5 Q1 Ifrs 5 Introduction To Financial Accounting 2 Studocu

Chapter9 Noncurrentassetsheldforsale2008

Solved Discuss Why Adoption Of Ifrs 1 Was Met With Contr Chegg Com

Ifrs 5 Non Current Assets Held For Sales And Discontinued Operations Summary International Financial Reporting Standards Income Statement

Ppt Agenda Powerpoint Presentation Free Download Id 230922

Ias And Ifrs

Https Cdn Ifrs Org Media Feature Supporting Implementation Agenda Decisions Ifrs 5 January 2016 Pdf

Https Www Iasplus Com En Publications Global Comment Letters 2015 Sep Ifric Upd Ifrs 5 1 At Download File Dttl 20tentative 20agenda 20decision 20 Ifrs 205 20intragroup 20transactions Pdf