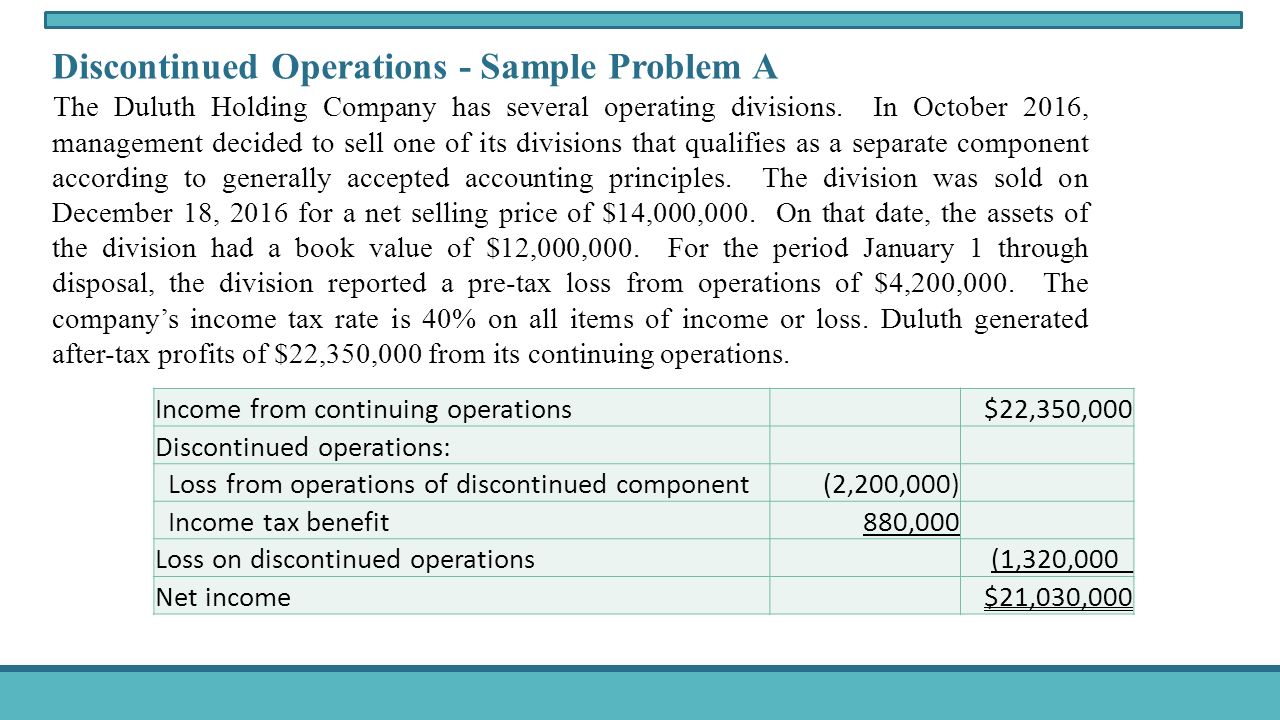

Income From Operations Of Discontinued Component

Income Statement Components Under Ias 1 Income Statement Personal Financial Statement Financial Statement

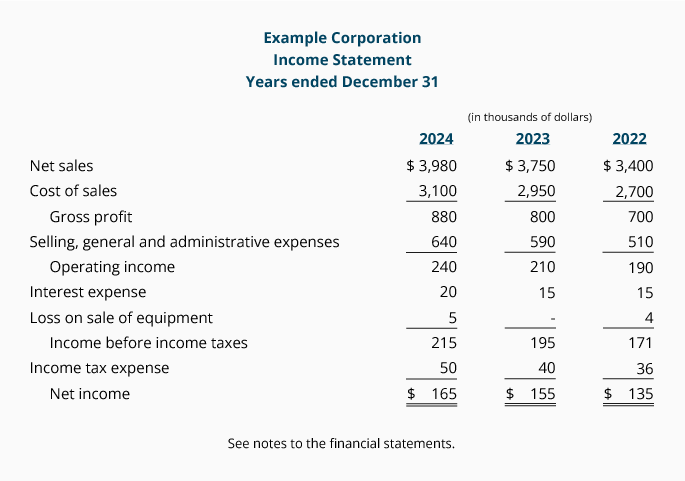

Operating Income Vs Gross Profit

Reporting Unusual Items Income Statement Accountingcoach

Operating Income Vs Net Income What S The Difference

Fresh 9 In E Statement Example Templates In 2020 Income Statement Statement Template Profit And Loss Statement

How Are Operating Income And Ebitda Different

Income from operations of discontinued component 840 income tax expense 210 income from discontinued operations 830 net income 4710 unrealized gain from investment 320 loss from foreign currency translation 240 80 comprehensive income 4790 income from continued operating 3 4 income from discontinued operating 0 525.

Income from operations of discontinued component. A discontinued operation is a separate major business division or geographical operation that the company has disposed of or is holding for sale. Loss on discontinued operations 3 900 000 net income. The two components of this disclosure are the profit or loss from the discontinued operations and the gain or loss from disposal. Loss from operations of discontinued business component 6 000 000 income tax benefit.

This shows financial statement users that this income will no longer be a part of the company s continuing operations. Analyze international paper net loss income from discontinued operations. International paper reported last year net loss income from discontinued operations of 310 5 million. Unrealized gains from investments 192 loss from foreign currency translation 144 48 comprehensive income 3843 p4 12.

Disclose the results from discontinued operations on the income statement or in accompanying notes. Income on discontinued operations 504 net income 3795 other comprehensive income net of tax. International paper net loss income from discontinued operations is very stable at the moment as compared to the past year. Inventory turnover ratio inventory turnover ratio cost of goods sold average inventory average inventory beginning inventory ending inventory 2 average inventory 600 800 1 400 2.

When a company sells or decides to sell a business component or unit it reports the income or loss from the operations of the unit separate from its other operations on its income statement. If an entity ceases to classify a component of an entity as held for sale the results of operations of the component previously presented in discontinued operations are reclassified and included in income from continuing operations for all periods presented ifrs 5 36. The unit the company is selling is called discontinued operations and must be a unit that is clearly distinguishable from its other business operations such as a food.

Ebit Vs Operating Income What S The Difference

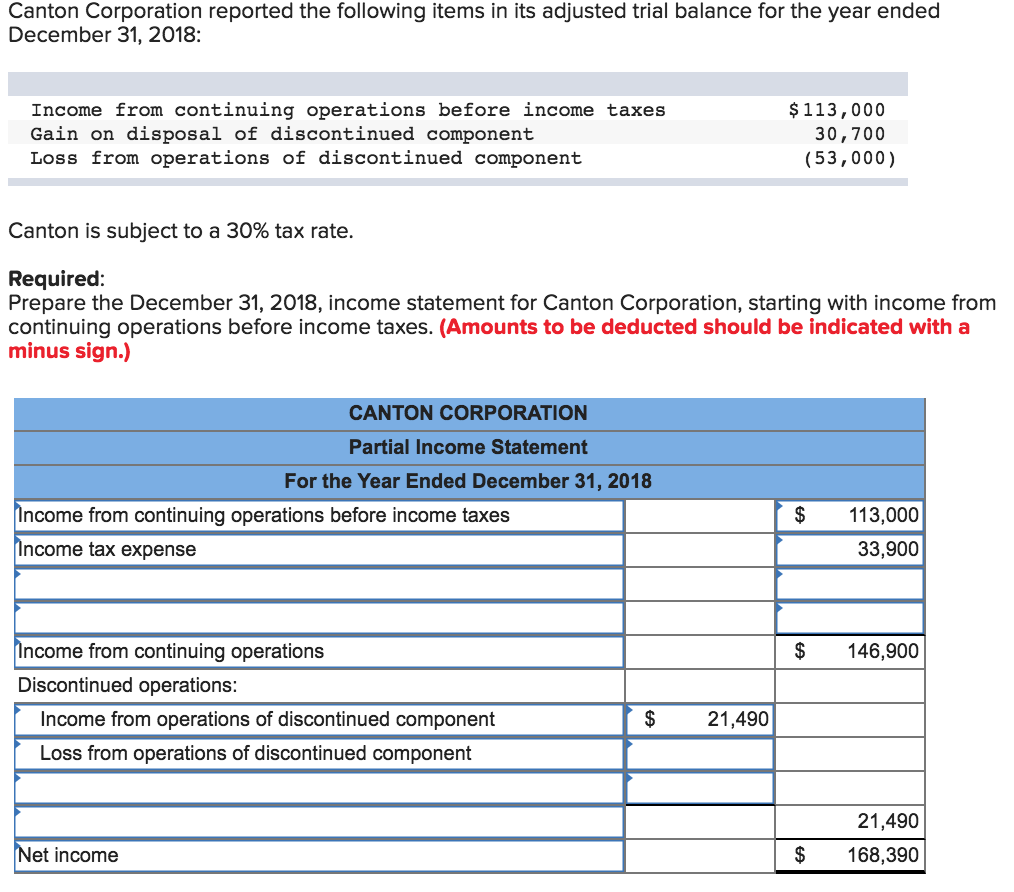

Solved Prepare The December 31 2018 Income Statement Fo Chegg Com

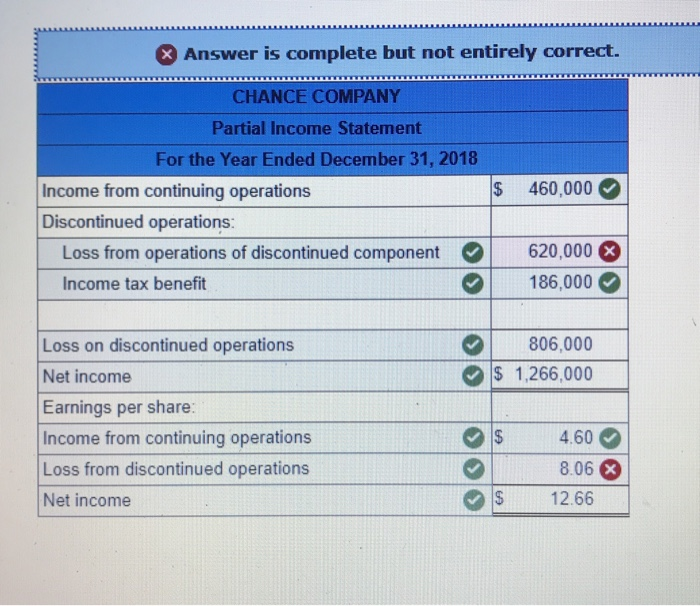

Solved B Determine The Total Gain Loss From Discontinued Chegg Com

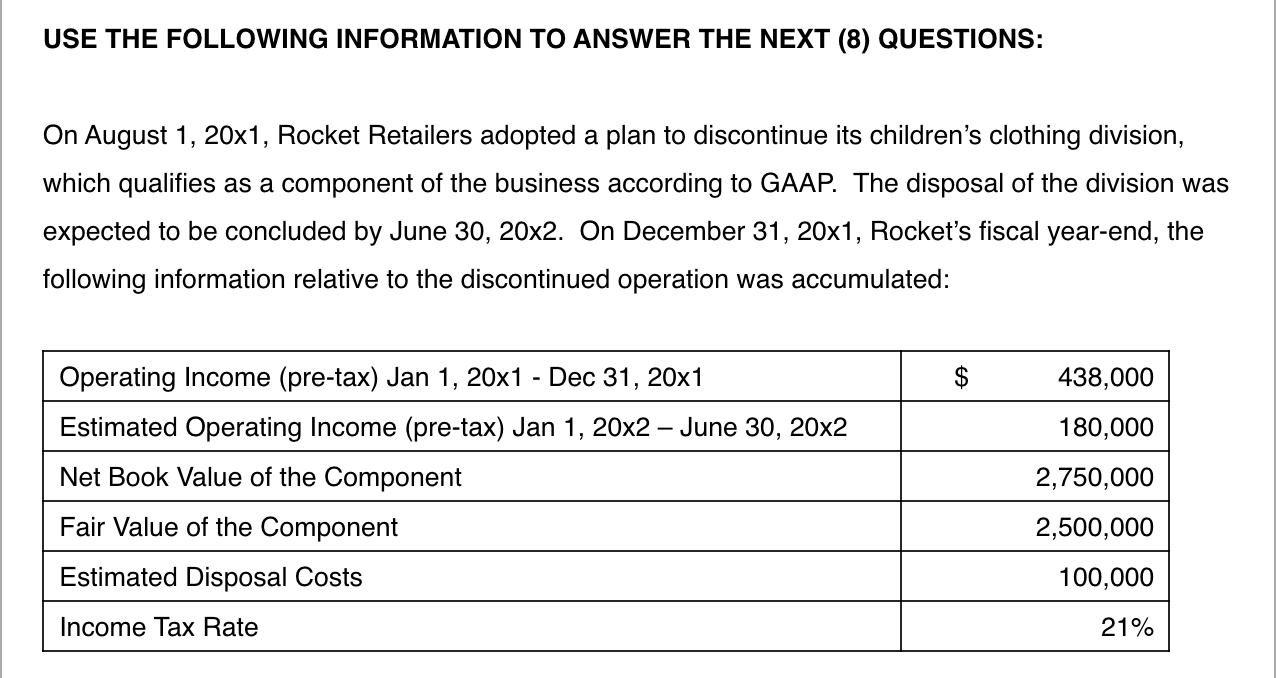

Solved Exercise 4 6 Discontinued Operations Lo4 4 4 5 Chegg Com

Income Statement Template 40 Templates To Track Your Company Revenues And Expenses Statement Template Income Statement Profit And Loss Statement

Income Statement Template Income Statement Statement Template Personal Financial Statement

Ebit Vs Operating Income What S The Difference

Profit And Loss Statement Form Printable On The Download Button To Get This Profit And Loss Profit And Loss Statement Statement Template Income Statement

Pin On Fitness And Health

Quickbooks Part 2 Of 3 Http Www Youtube Com Watch V 6ccvz3cm0dy Quickbooks Quickbooks Tutorial Bookkeeping Business

Balance Sheet Everything About Investment Accounting Classes Bookkeeping Business Balance Sheet

The Income Statement And Comprehensive Income Intermediate Accounting I Chapter 4 This Presentation Is Under Development Ppt Download

Income Statement Template 47 Income Statement Statement Template Financial Statement