Net Income From Continuing Operations Formula

Operating Income Vs Net Income What S The Difference

:max_bytes(150000):strip_icc()/AppleIncomeSattementDec2019-cd967d0a8f5e4748a1060f83a7e7acbc.jpg)

Net Income After Taxes Niat

How Do Net Income And Operating Cash Flow Differ

:max_bytes(150000):strip_icc()/NetProfitMargin2-edf5ae45cbe048208913caa9d3b03110.png)

Net Profit Margin Definition

How To Calculate Pre Tax Profit With Net Income And Tax Rate The Motley Fool

:max_bytes(150000):strip_icc()/dotdash_Final_Gross_Profit_Operating_Profit_and_Net_Income_Oct_2020-01-55044f612e0649c481ff92a5ffff1b1b.jpg)

Gross Profit Operating Profit And Net Income

Since one time events and the results of discontinued operations are excluded this measure is considered to be a prime indicator of the financial health of a firm s core activities.

Net income from continuing operations formula. Interest earned or paid should not be. Net income from continuing operations is a line item on the income statement that notes the after tax earnings that a business has generated from its operational activities. Operating income total revenue direct costs indirect costs. Net income formula is used for the calculation of the net income of the company.

There are three formulas to calculate income from operations. To calculate the income from continuing operations subtract the cost of goods sold and other operating expenses such as cost from labor from the revenue earned from the day to day operations of a business. The example also shows how net income 200 000 is at times greater than operating income 170 000 due to other items in this case income from discontinued operations 20 000 and extraordinary. Formula for operating income.

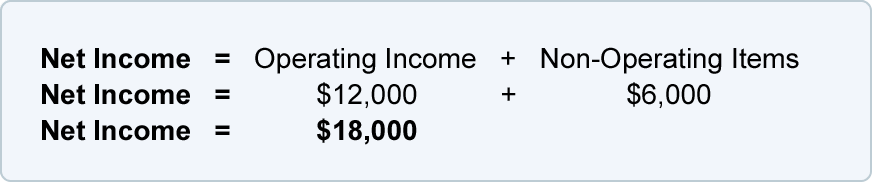

Net income total revenues total expenses. After all of the expenses are deducted the investor is left with a figure called net income from continuing operations. Operating income net earnings interest expense taxes. It is the most important number for the company analysts investors and shareholders of the company as it measures the profit earned by the company over a period of time.

Where funds from operations net income depreciation depletion amortization deferred taxes investment tax redit other funds. To calculate operating income start with revenue from operations subtract the cost of goods sold and other operating expenses such as the cost of labor. Net income from continuing operations. Profit margin is a financial ratio defined as net income divided.

Income earned from the equipment sale is part of the profit margin but selling assets is not a sustainable way to generate profits. Operating income and net income both show income for a company. For example a company reports 180 000 of sales 80 000 cost of goods sold and 15 000 of operating expenses. In the above example operating income is stated in the item called income from continuing operations which equals 170 000.

The Formula For Calculating Ebitda With Examples

Adjusted Ebitda Overview How To Calculate Adjusted Ebitda

Operating Income Vs Gross Profit

Pin On Fitness And Health

Earnings Before Interest And Taxes Ebit Overview Financial Edge Training

Nopat Net Operating Profit After Tax What You Need To Know

Ebit Vs Operating Income What S The Difference

How Are Operating Income And Ebitda Different

Pin On Basics Of Accounting Definition Types

Gross Vs Net Income Definitions And How To Calculate Mbo Partners

Single Step Vs Multi Step Income Statement Key Differences For Small Business Accounting

Income Statement Examples Gaap Ifrs Accounting

Multiple Step Income Statement Accountingcoach

:max_bytes(150000):strip_icc()/dotdash_Final_Income_Statement_Aug_2020-02-23bef448b8aa4c9bac46c8e15b2b9f0a.jpg)