Passive Income Business Limit Reduction

Investing Through A Professional Corporation Physician Finance Canada

Understanding Passive Activity Limits And Passive Losses 2020 Tax Update Stessa

Don T Be Passive About Canada S New Passive Income Rules Advisor S Edge

An Active Approach To Passive Income Investment Executive

Company Tax Rates Atotaxrates Info

Https Ca Rbcwealthmanagement Com Documents 634020 634036 The Navigator Taxation Of Business Income In A Corporation Pdf 988001e9 8304 4a3f 8b42 Fd43ef4befd7

There is a new limitation on the 500 000 small business deduction based on a company s previous year s passive income.

Passive income business limit reduction. The 30 000 additional passive income has reduced the small business deduction by 150 000 thereby increasing the tax obligation by 21 000 26 5 150 000 12 5 150 000. Better understand the reduction of the business limit on october 16 2017 department of finance announced to reduce the tax rate for small ccpcs that earned a qualifying active business income from 10 5 per cent to 10 per cent effective january 1 2018 and to 9 per cent effective january 1 2019. Enter the reduction on new line 422 and the resulting reduced business limit on new line 426. A corporation can have up to 50 000 of investment income in the prior year with no impact to the small business deduction.

The reduction in the ccpc s business limit is then the greater of its taxable capital business limit reduction and its passive income business limit reduction for the year. Please see the table below for how passive income reduces the small business deduction and correspondingly increases the tax penalty. Depending on the amount of passive income eg. Under the proposals the small business limit will be reduced by 5 for every 1 of investment income above a 50 000 threshold.

Bl 500 000 x 5 aaii 50 000 where. The passive income reduction reduces a corporation s business limit for a taxation year as otherwise determined by five dollars for every dollar by which the corporation s adjusted aggregate investment income as newly defined in subsection 125 7 and that of its associated corporations for taxation years ending in the preceding. Passive income earned small business limit reduction small business limit available. Investment income such as interest dividends and capital gains a private corporation may be subject to a reduction of their sbd.

5 x 90 000 50 000 200 000. Canadian controlled private corporation s passive investment income. Under this formula the sbd will be eliminated when investment income reaches 150 000 in a given taxation year. Bl is the ccpc s business limit otherwise determined for the particular year i e its business limit as described above.

The passive income reduction reduces a corporation s business limit for a taxation year as otherwise determined by five dollars for every dollar by which the corporation s adjusted aggregate investment income as newly defined in subsection 125 7 and that of its associated corporations for taxation years ending in the preceding. Income in excess of the small business limit would be taxed at the general corporate rate of 26 5.

Instructions For Form 8995 2019 Internal Revenue Service

Cra Changes To Taxation Of Passive Income Manning Elliott Llp Accountants Business Advisors

Https Invested Mdm Ca Md Articles New Passive Income Rules Starting In 2019 What Incorporated Physicians Need To Know

Instructions For Form 8990 05 2020 Internal Revenue Service

S Corps Should Beware How Elections Are Made Shindelrock

Tax Guide Cpa For Real Estate Investors Real Estate Tax Accountant

Pin On Passive Income For Beginners Side Hustle Tips

Https Www Alberta Ca Assets Documents Tra Form Corporate Tax Return At2 Pdf

Publication 514 2019 Foreign Tax Credit For Individuals Internal Revenue Service

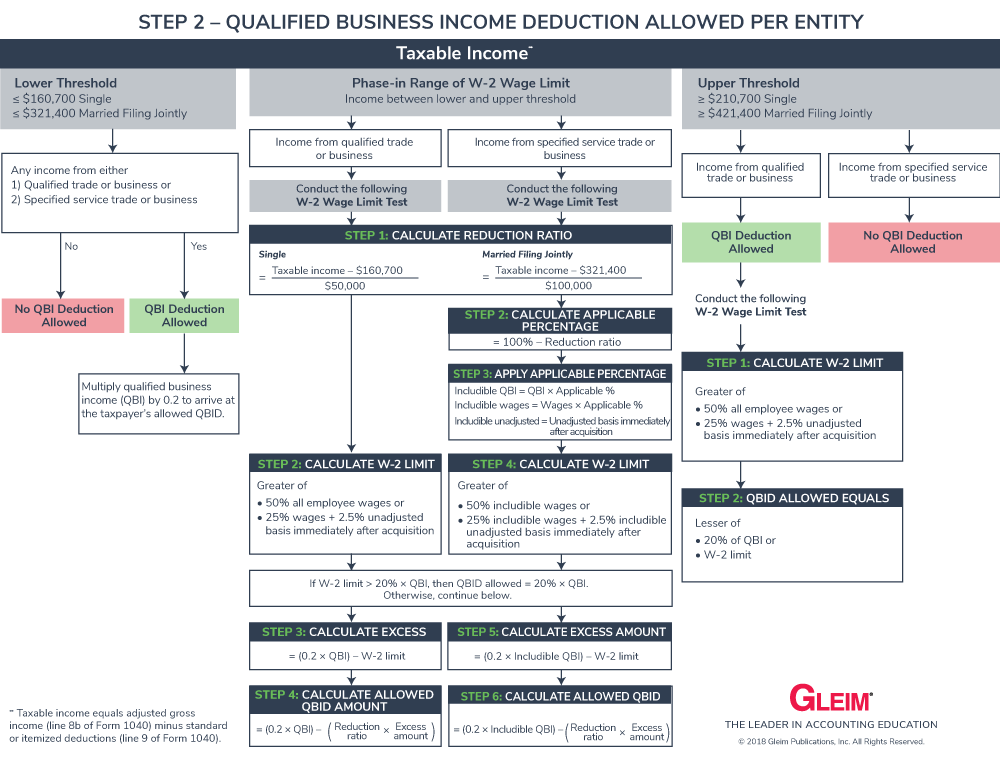

Section 199a Qualified Business Income Deduction Qbid Gleim Exam Prep

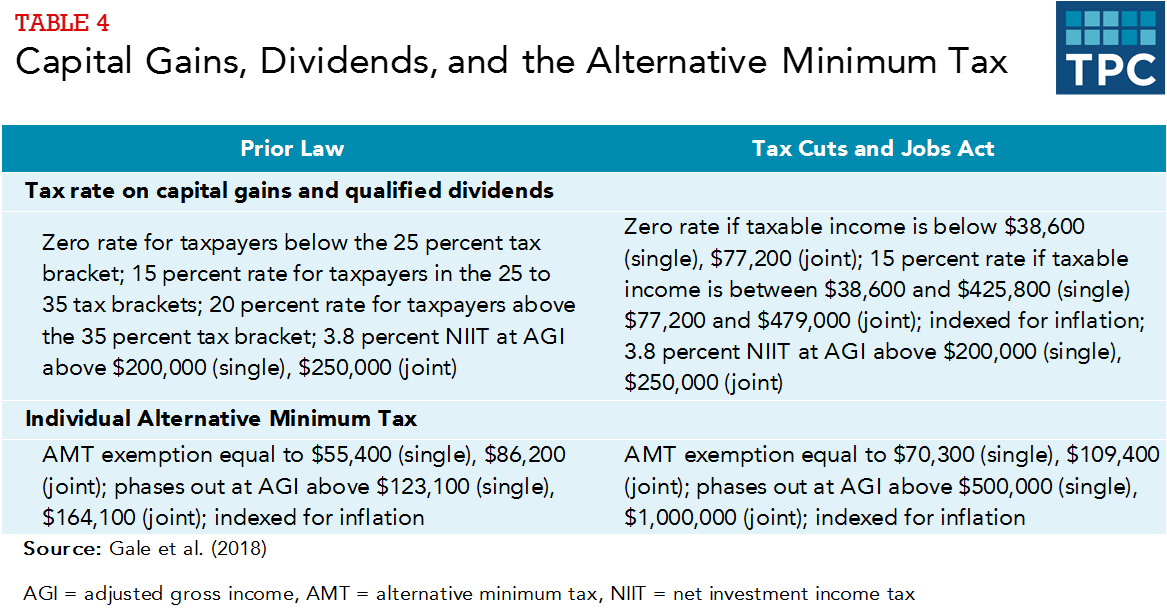

How Did The Tax Cuts And Jobs Act Change Personal Taxes Tax Policy Center

Help Your Customers Keep A Safe Distance With Peel And Stick Floor Decals Each Decal Is A 12 X 12 Inch Cir In 2020 Business Pins Standing In Line Peel And Stick Floor

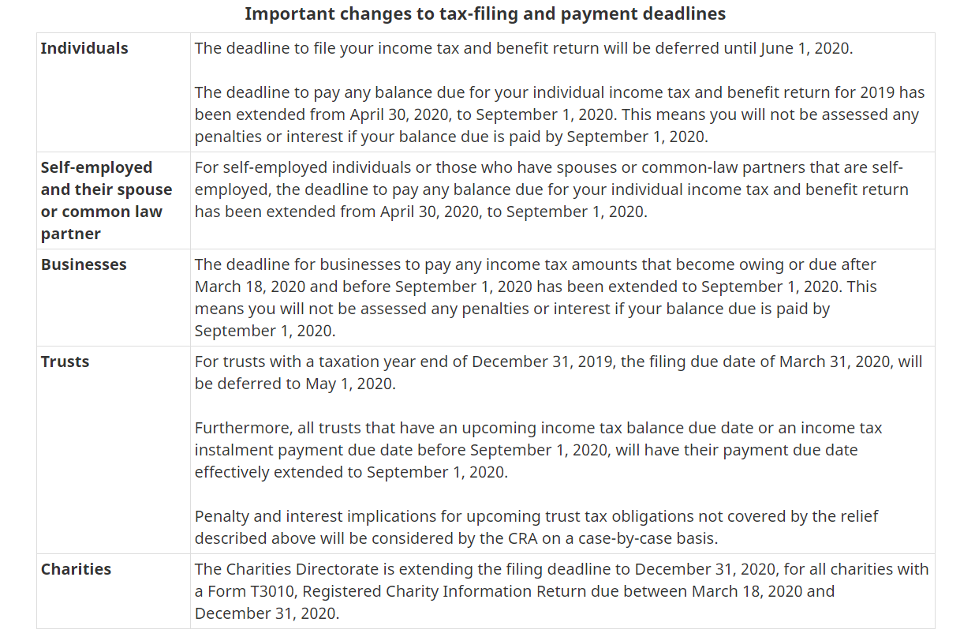

Canada Passes Covid 19 Economic Response Plan Into Law Our Tax Take Moodys Tax