Passive Income Tax Rate In Canada

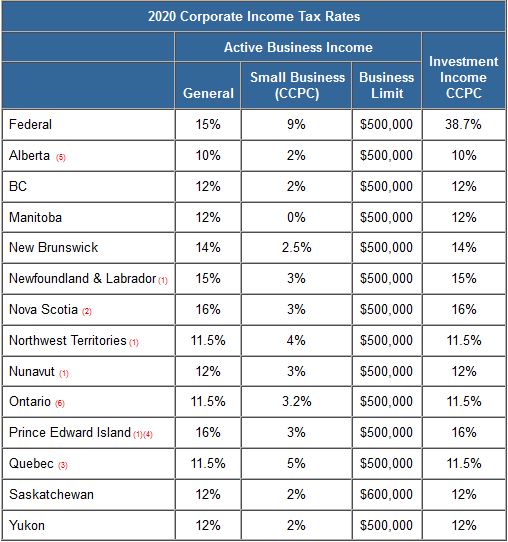

2020 Corporate Income Tax Rates Bdo Canada

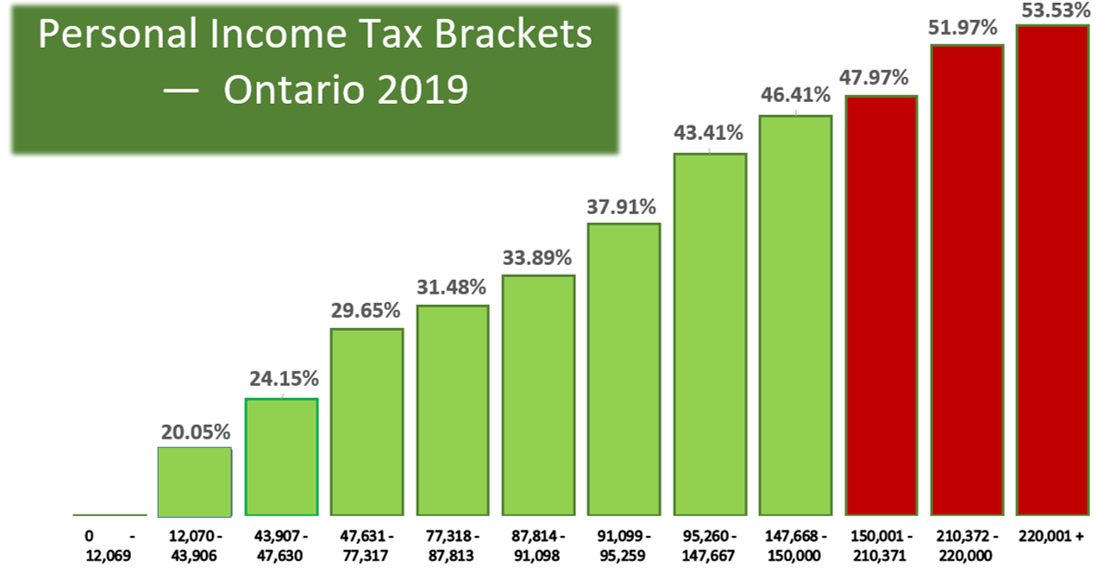

Taxtips Ca Personal Income Tax Rates For Canada Provinces Territories

Taxtips Ca Business 2020 Corporate Income Tax Rates

Canadian Tax Return 2020 In 2020 Income Tax Income Tax Return Income

We Ve Had Some Fun With Facts And Put Together Our Canadian Tax Landscape Infographic Reflecting On Canada S Genes Investing Dividend Investing Investing Money

Blog Md Tax Physician Services Tax Consulting

The small business clawback in 2018 canadian controlled private corporations ccpcs pay corporate income tax on small business income at 10 percent federally.

Passive income tax rate in canada. Businesses with less than 50 000 in annual passive income can claim the full 500 000 at the 9 small business rate. Since 2009 a ccpc using the sbd could claim the small business tax rate on the first 500 000 of its active business income carried on in canada representing a fairly substantial reduction in tax. At 150 000 of passive income none of the active business income will qualify for the small business tax rate. This has a dramatic effect on the amount of tax on that 500 000.

So if you have a portfolio within your corporation that generates more than 50k year in passive income more of your corporate active income will face the higher general tax rate. This results in a net corporate tax of 8. These types of passive investment income earned inside a ccpc are part i tax and will be taxed at a federal rate of 38 67. How do the new passive income rules affect small businesses.

The small business deduction limit will get reduced by 5 for every 1 in excess passive income. In 2019 the company will earn 500 000 of active business income. After 500k active earnings are taxed at the general tax rate of 15. Of the 38 67 the ccpc will receive a refundable dividend tax on hand credit rdtoh of 30 67 when a taxable non eligible dividend is paid out to the shareholders.

The amount eligible for the small business rate shrinks by 5 for every 1 over 50 000 that a business makes in passive income until it eventually reaches zero. With the exception of inter corporate dividends passive income earned by ccpcs or any corporation in canada is ineligible for deductions and consequently fully taxable at the corporation s combined provincial and federal tax rate. This rate is to be reduced to 9 percent in 2019. As illustrated in the table below the passive income rule change will result in the company paying 40 000 more tax than it would have before the cra passive income tax changes.

In 2018 the company earned 100 000 of passive investment income.

Tax Tips 2016 Investment Income Capital Gains And Losses Tax Canada

Pin On Canadian Personal Finance

If You Have Rental Properties In Canada Check Out This Helpful Infographic F Real Estate Investing Rental Property Rental Property Investment Rental Property

Corporate Taxation Tax Integration Of Canadian Interest Income Canadian Portfolio Manager Blog

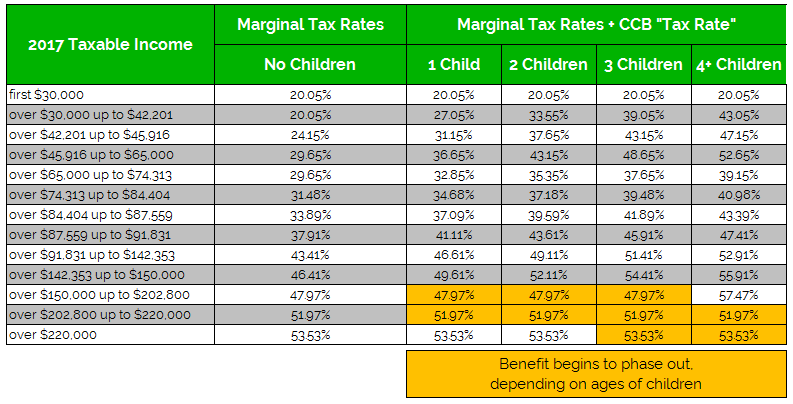

Canada Child Benefit The Hidden Tax Rate Planeasy

The Guide On Tax Efficient Investing In Canada Genymoney Ca Investing Dividend Income Dividend Investing

How To Build A Supplementary Income Flow Passive Income Ideas Infographic Build Flow Ideas Income Infograp Smart Passive Income Passive Income Income

Taxes In Canada Have Been Reported As Increasing Faster Than Other Expenditures But Tax Rates May Actually Be Decreasin Personal Finance Personal Finance Blogs

How I Am Investing In Lending Loop Canada S First Peer To Peer Lending Marketplace Peer To Peer Lending Investing Being A Landlord

How Money You Earn Flows Through Your Corporation To Your Pocket Physician Finance Canada

Canada Tax Deductions Tax Credits To Take Advantage Of In 2020 Tax Deductions Business Tax Tax Credits

Determine Your Passive Investment Income Limit Free Tools

2 121 Likes 28 Comments Investing Entrepreneurship Entrepreneurmotivations On Instagram Str Money Management Advice Business Tax Deductions Investing