Passive Investment Income Tax Canada

Don T Be Passive About Canada S New Passive Income Rules Advisor S Edge

Determine Your Passive Investment Income Limit Free Tools

Can You Benefit From The Loosened Grip On Ccpc Passive Income Tax Physician Finance Canada

Corporate Taxation Tax Integration Of Canadian Interest Income Canadian Portfolio Manager Blog

Explaining The Refundable Dividend Tax On Hand Rdtoh The New Passive Income Rules A Lesson In Klingon Physician Finance Canada

Deloitte Tax Hand

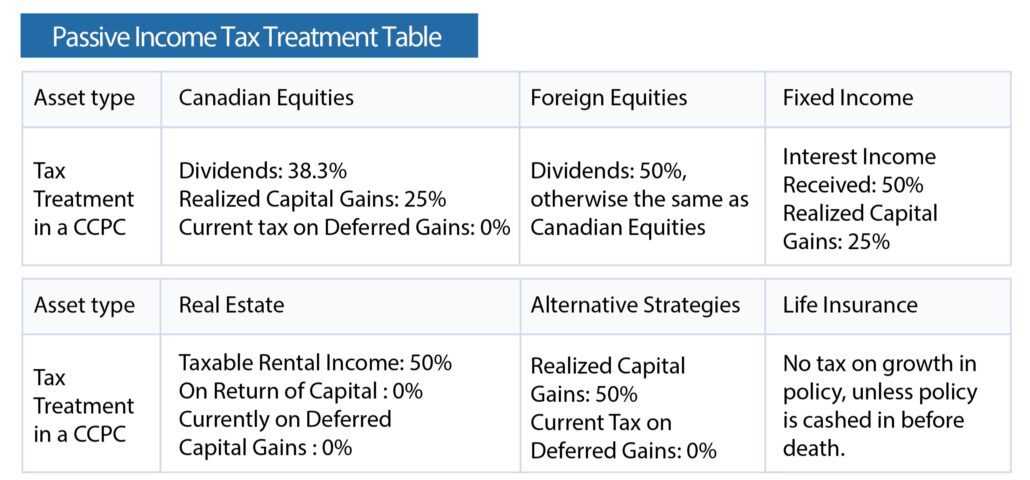

Effective tax rate on income eligible for the small.

Passive investment income tax canada. For many small business owners their private company is a key component in saving for their family and their future retirement. Passive investment income on july 18 2017 the government released a consultation paper with proposals to address tax planning strategies using private corporations including an outline of possible approaches to limit the tax deferral opportunities that are associated with holding passive investments inside a private corporation. The shareholder will pay tax when the income is distributed as a dividend. That means that an increase in passive investment income of 100 000 from 50 000 to 150 000 would result in an additional 80 000 of tax on active business income.

The paper discussed the government s two key objectives which are to i preserve the intent of the lower tax on business income to encourage growth and job creation and. The recent federal budget proposed changes the proposals that will restrict access to the small business deduction sbd for many corporations. 38 federal starting rate less the 10 provincial abatement. Additional refundable tax levied on canadian controlled private corporations.

For this ccpc 150 000 of passive investment income results in 135 500 of tax on active business income at the combined corporate tax rate of 27. Passive investment income 26 october 2017. The new rule changes mean that a ccpc s passive investment income now exposes a business owner to more tax on active business income. Assumed average provincial tax rate on this type of income 4.

The new cra passive income changes took effect at the beginning of 2019 upsetting corporate passive investment income and exposing businesses to more corporate tax. Passive investment income in your private corporation. The corporate tax rate on investment income is usually higher than the highest personal marginal tax rate and exceeds 50 per cent in many provinces. All passive income earned through investments that are part of a non registered investment plan or portfolio are considered to be taxable income in canada.

Remember for canadian controlled private corporations ccpc that income below 500 000 will be taxed at the federal small business tax rate of 9 and above 500 000 will be taxed at the federal active. Net tax rate for aggregate investment income. These changes will apply where a corporation earns passive investment income and also earns income from active business that is taxed at the small business rate or small business income. Since 2009 a ccpc using the sbd could claim the small business tax rate on the first 500 000 of its active business income carried on in canada representing a fairly substantial reduction in tax.

Input the adjusted aggregate investment income passive investment income and it will calculate your access to the small business tax rate. A portion of the tax is refundable and added to the refundable dividend.

How Money You Earn Flows Through Your Corporation To Your Pocket Physician Finance Canada

Tax Tips 2016 Investment Income Capital Gains And Losses Tax Canada

Canadian Outbound Taxation International Tax Blog

Https Ca Rbcwealthmanagement Com Documents 634020 634036 The Navigator Passive Investment Income In A Private Corporation Pdf C0b3cc74 795d 4745 Af86 Bbcc8833c3cb

Corporation Grip As A Tax Slashing Weapon Physician Finance Canada

Https Advisors Td Com Saverio Veltri Mediahandler Media 313770 410 18 Passive Investment Income En1 Pdf

Is It Time To Reexamine Your Corporate Structure Tax Canada

Corporate Taxation Interesting Angles On Canadian Interest Income Canadian Portfolio Manager Blog

What Is Considered Passive Income In Canada

Canada S New Passive Income Rules Take An Ax To The Tax Compass Wealth Partners

Cra Changes To Taxation Of Passive Income Manning Elliott Llp Accountants Business Advisors

Corporate Taxation Of Investment Income Capital Gains Tax 2019 Canada