Tax Rate For Passive Income In Canada

Canadian Tax Return 2020 In 2020 Income Tax Income Tax Return Income

The Guide On Tax Efficient Investing In Canada Genymoney Ca Investing Dividend Income Dividend Investing

If You Have Rental Properties In Canada Check Out This Helpful Infographic F Real Estate Investing Rental Property Rental Property Investment Rental Property

Taxes In Canada Have Been Reported As Increasing Faster Than Other Expenditures But Tax Rates May Actually Be Decreasin Personal Finance Personal Finance Blogs

Income Tax 2020 Changes Every Canadian Needs To Know In 2020 Money Mom Income Tax Budgeting Money

Eq Bank Review High Interest Savings Account In Canada High Interest Savings High Interest Savings Account Savings Account

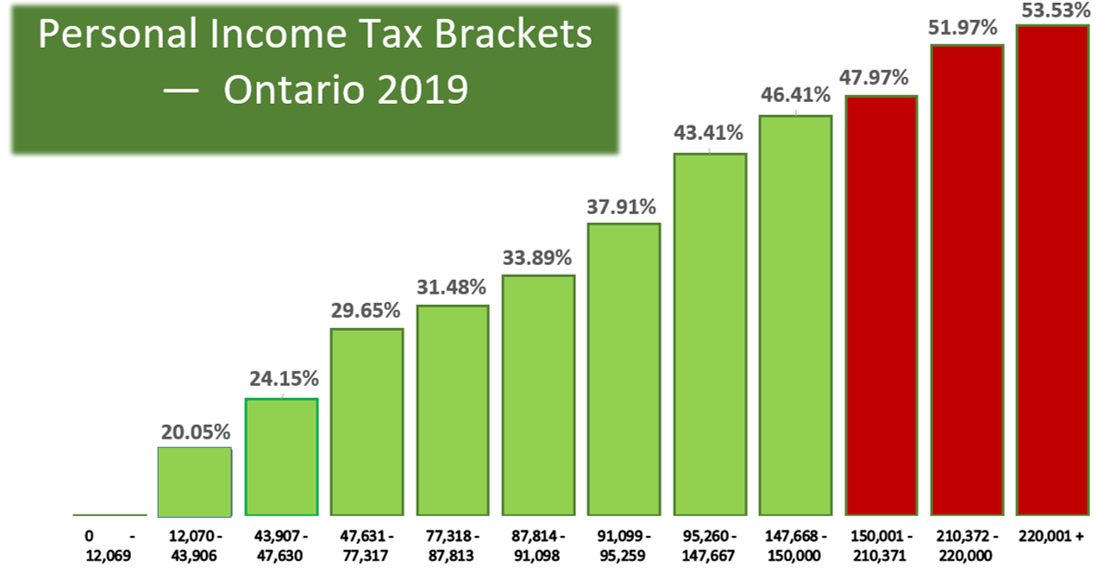

0 15 and 20 based on your income bracket.

Tax rate for passive income in canada. The 2018 federal budget saw the introduction of a set of new passive income rules in canada to restrict the small business deduction for ccpcs that alone or as part of an associated group earn more than 50 000 of passive investment income. At 150 000 of passive income none of the active business income will qualify for the small business tax rate. Passive income tax rate for 2017 for 2017 passive income that is taxed as ordinary income will be taxed in the 2017 tax brackets and so the income tax rates range from 10 to 39 6 percent depending on your annual income. With the exception of inter corporate dividends passive income earned by ccpcs or any corporation in canada is ineligible for deductions and consequently fully taxable at the corporation s combined provincial and federal tax rate.

As outlined the effective tax rate on passive income is 50 7 while dividend income is taxed at 38 3. However a portion of the federal tax on passive and dividend income is refundable when a taxable dividend is paid to a corporation s shareholder. Long term capital gains and qualified dividends are taxed at zero 15 and 20 percent for 2017 but the brackets are different. Long term passive income tax rates long term capital gains assets held for more than one year are taxed at three rates.

This is a federal calculation only as the provinces do not have a refundable component. These types of passive investment income earned inside a ccpc are part i tax and will be taxed at a federal rate of 38 67. This uses a projected top marginal tax rate on eligible dividends received by an individual in 2019 of 31 71 percent and similarly a top marginal tax rate on non eligible dividends of 42 56 percent. Since 2009 a ccpc using the sbd could claim the small business tax rate on the first 500 000 of its active business income carried on in canada representing a fairly substantial reduction in tax.

Of the 38 67 the ccpc will receive a refundable dividend tax on hand credit rdtoh of 30 67 when a taxable non eligible dividend is paid out to the shareholders. When you are caught up in the hustle and bustle of your 9 5 job i e. This is frequently higher than the marginal tax rate payable by the individual which reduces the desirability. This assumes that 500 000 of income is taxed at corporate tax rates and then paid out to the shareholders as a taxable dividend.

I must confess but often when i lay awake at night it s because my mind is continually racing to figure out how to earn enough passive income so i can free up my time to do other things. This has a dramatic effect on the amount of tax on that 500 000. For this ccpc 150 000 of passive investment income results in 135 500 of tax on active business income at the combined corporate tax rate of 27.

We Ve Had Some Fun With Facts And Put Together Our Canadian Tax Landscape Infographic Reflecting On Canada S Genes Investing Dividend Investing Investing Money

How To Build A Supplementary Income Flow Passive Income Ideas Infographic Build Flow Ideas Income Infograp Smart Passive Income Passive Income Income

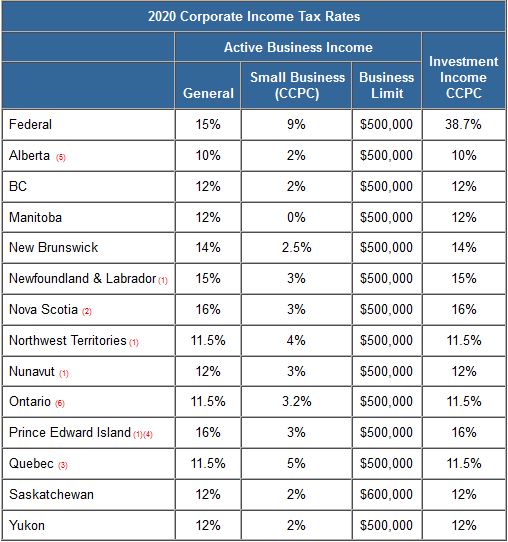

Taxtips Ca Business 2020 Corporate Income Tax Rates

Schreder Brothers Real Estate Group Crea Recommendations For The Home Buyers Plan Infographic N 004 Real Estate Infographics Investment Property Real E

Pin By Brayden On I W A N T T H I S In 2020 Canadian Money Money Logo Money Gift

2 121 Likes 28 Comments Investing Entrepreneurship Entrepreneurmotivations On Instagram Str Money Management Advice Business Tax Deductions Investing

Pin On Homes For Sale In Edmonton Alberta

How I Am Investing In Lending Loop Canada S First Peer To Peer Lending Marketplace Peer To Peer Lending Investing Being A Landlord

Follow Us On Instagram Where We Post Daily Inspirations For Obtaining Financial Freedom Positive Mind Financial Education Financial Literacy Financial Freedom

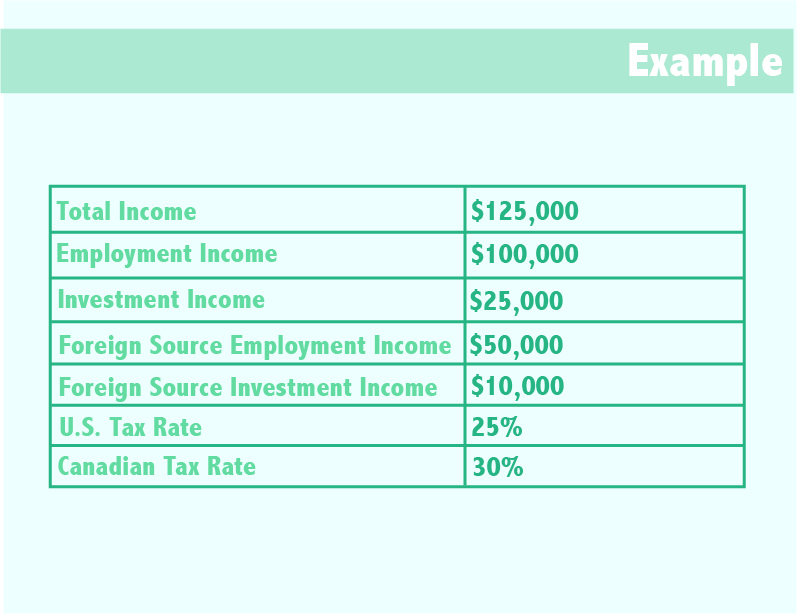

Foreign Tax Credits For Canadians Madan Ca

Pin On Make Money

Residents Fellows Archives Md Tax Physician Services Tax Consulting

Top 11 Best Stock Research Websites Moneybyramey Com In 2020 Stock Research Finance Investing Research Websites