The Taxation Of Foreign Passive Income For Groups Of Companies

Pin On Money Matters

How Is Passive Income Taxed Free Investor Guide

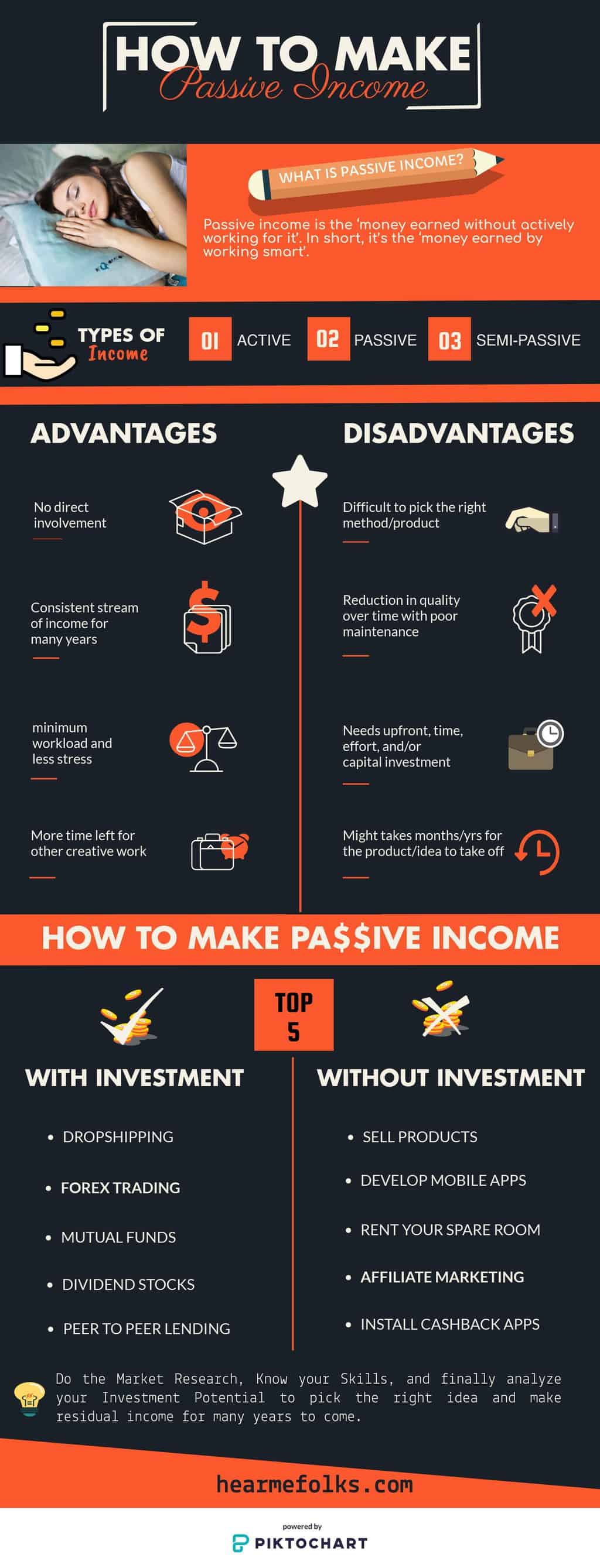

28 Epic Passive Income Ideas Worth 100k A Year Hearmefolks

5 Things You Should Know Before Investing In Real Estate In 2020 Real Estate Investing Investing Real Estate Tips

10 Best Passive Income Investments What Is Passive Income

Ranking The Best Passive Income Investments Passive Income Financial Best Way To Invest

Considered questions specific questions.

The taxation of foreign passive income for groups of companies. 2 the rule in subsection 1 applies to. Taxation of foreign passive income for group companies. The foreign sourced income exemption as it existed until 31 december 2019 has been replaced by a new tax regime that solely includes income from a domestic enterprise. 279f related 51 group company u k.

Taxation of foreign passive income for group of companies the directives. Usp must treat the 200 inclusion 160 fphci plus 40 section 78 dividend and the 40 of foreign tax as passive category income and tax and must comply with the procedures in prop. Income that is considered derived from foreign entrepreneurial activity is excluded from the taxable base for profit tax purposes. Foreign tax credits are available for the foreign taxes as sociated with subpart f inclusions and a novel foreign tax credit approach applies with respect to gilti inclu sions.

If i the country of head office of the foreign affiliate does not have any tax on corporate income or ii the effective tax rate of the foreign affiliate is 20 or less even when the head office country has system of corporate income tax the foreign affiliate is called designated foreign subsidiary. Taxation if the foreign corpora tion was not a cfc for an uninterrupted period of at least 30. Under prior law subpart f income earned by a cfc was not subject to u s. Until cfc rule was adopted foreign passive income obtained in low tax jurisdiction was not subject to.

Directives for the report the subject. Taxation of foreign passive income for group of companies jamal afakir olivier gaston braud pierre régis dukmedjian 21 january 2013. In principle japanese corporations are subject to corporate tax in japan only with respect to its own income. Only the anti abuse provisions 2.

Introduction traditionally danish tax law is considered to be based on a principle of world wide taxation 1 however for companies a limited principle of territoriality was introduced in 2005 2 accordingly income from permanent establishments and landed property located abroad should be excluded from the taxable income 3 companies incorporated in denmark are subject to full danish. 1 for the purposes of this chapter a company b is a related 51 group company of another company a in an accounting period if for any part of the accounting period a a is a 51 subsidiary of b b b is a 51 subsidiary of a or c both a and b are 51 subsidiaries of the same company. Taxation on notional income as a specific anti avoidance measure south african residents have to account for an amount equal to the net income of a controlled foreign company cfc on the basis that the net income is calculated as if the cfc were a south african tax resident in terms of certain sections of the act. Unless the designated foreign.

Financial Samurai Passive Income Portfolio Update 2018 Financial Samurai

Want To Earn Income From Real Estate But Can T Afford The Upfront Cost Of Buying A Property Consider Reit S To Earn So Income Investing Passive Income Income

Pin On Personal Finance The Simple Way

Pin By Mark Eldridge On Network Marketing Network Marketing Quotes Residual Income Financial

Foreign Acquisition Structures Business History Legal Support Investing

Become An Investor And Earn Residual Income 90 Of The People Fall In Employee Self Employed Category Who Are Poor Cashflow Quadrant Residual Income Cash Flow

Pepsi Dividend Stock Analysis Big Dividends Dividends Diversify Dividend Stocks Dividend Stock Analysis

Pfics Rules Initial Impressions And Observations Kpmg United States

How Is Passive Income Taxed Passive Income Tax

21 Passive Income Ideas For A Freedom Lifestyle 2020

Corporation Vs Rrsp Vs Tfsa Simulator Under The Hood Physician Finance Canada

Taxhow Filing Your Federal State Taxes Free Federal E File In 2020 Filing Taxes Online Taxes Income Tax

What Is The Cashflow Quadrant Cashflow Quadrant Residual Income Cash Flow