New Passive Income Rules Effective Date

The Concept Of Passive Income And List Of 6 Easy Passive Income Ideas Getmoneyrich

Ranking The Best Passive Income Investments Financial Samurai

Best Passive Income Ideas For Beginners In 2020

Https Invested Mdm Ca Md Articles New Passive Income Rules Starting In 2019 What Incorporated Physicians Need To Know

Active Income Vs Passive Income Passive Income Ideas Social Media Passive Income Online Profit

Investing Through A Professional Corporation Physician Finance Canada

But for every dollar of passive income over that amount you lose 5 of the deduction.

New passive income rules effective date. 125 5 1 b which eliminates the business limit of a canadian controlled private corporation if it or associated corporations had significant passive income a k a. Federally the first 500 000 of active business income is taxed at the small business deduction sbd tax rate. As you probably remember the government passed new tax legislation in june 2018 around private corporations and passive income. These changes will apply where a corporation earns passive investment income and also earns income from active business that is taxed at the small business rate or small business income.

Starting january 1 2019 new rules about passive income will take effect and many incorporated physicians could feel the consequences. The purpose of the new passive investment income proposals is to remove some of this tax deferral advantage the size of which depends on the difference between the applicable corporate tax rate and the shareholder s personal tax rate. A previous amendment to income splitting laws which came into effect as of 2018 introduced a tax on split income paid to family members unless those family members were meaningfully contributing to the business and met certain other criteria. There is a new limitation on the 500 000 small business deduction based on a company s previous year s passive income.

You can earn passive income whether you re an entrepreneur with a brilliant business plan a talented artist or just happen to have extra cash to invest. The new passive income rules don t affect income splitting. The recent federal budget proposed changes the proposals that will restrict access to the small business deduction sbd for many corporations. These new cra passive income changes will first apply to fiscal years that start in 2019 and will.

Aggregate investment income in their taxation years ending in the preceding calendar year is stated to apply to taxation years that begin after 2018. The initial downtime you put into passive income can be as involved as starting a blog or as simple as logging into a robo advisor platform and investing 100. The look through rules under section 904 d 3 provide that certain dividends interest rents and royalties i e passive income of the taxpayer received or accrued from a cfc are not treated as passive category income. A corporation can have up to 50 000 of investment income in the prior year with no impact to the small business deduction.

Start building a nest egg.

Factors Affecting The Us Dollar Us Economy In 2020 Investing Stock Market Investing Money

Modicare Passive Income Plan How To Earn 6 14 Lakhs Per Month Youtube How To Plan Passive Income Business Planning

Real Estate Investing For Beginners Realestatetips Do You Want To Invest In Real Estate But Can T Afford In 2020 Real Estate Investing Investing Beginner Real Estate

The Highly Effective Money Management Matrix I Dream Of Fire Money Management Project Management Quotes Management

Pin On Online Jobs

Launch Date Of Onpassive Coming Up In 2020 Dating Product Launch Get Excited

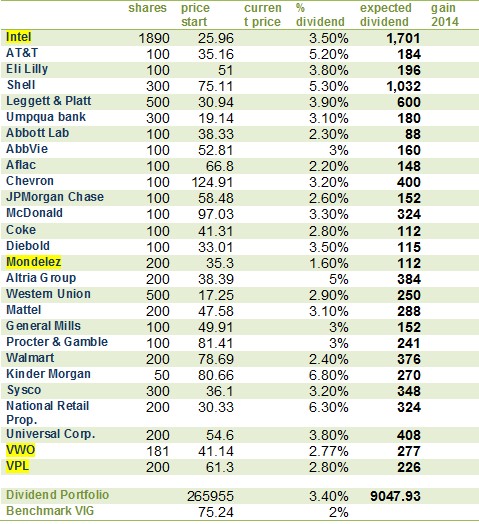

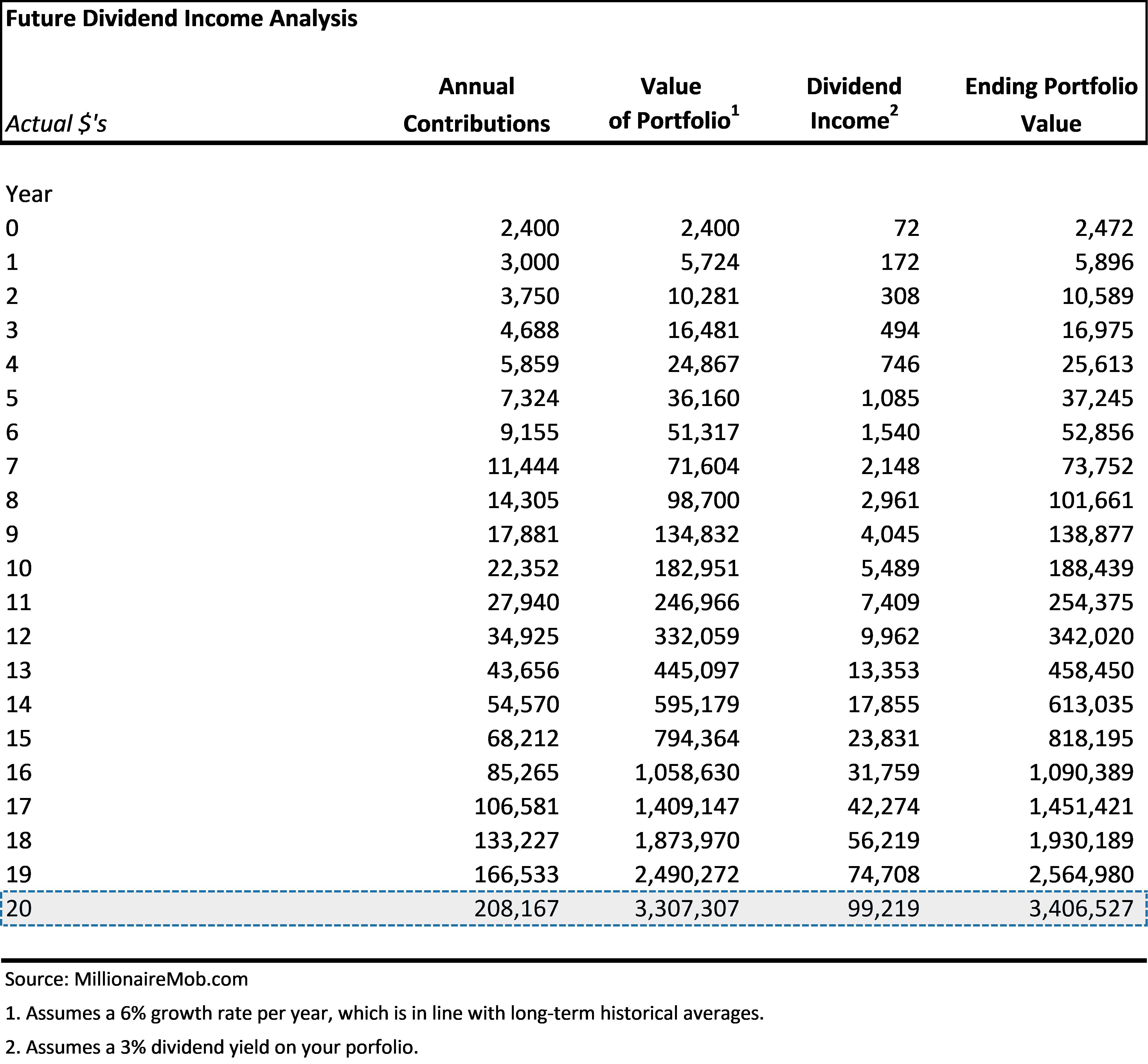

Building A Dividend Growth Portfolio For Passive Income

The Act Allows Flow Through Businesses In New Jersey Such As Sub S Corporations Partnerships Llcs Or Sole Proprietorsh In 2020 Tax Services Tax Rules Tax Deductions

A Simple And Effective Plan For Personal Money Management And Wealth Creation In 2020 Money Management Investing Emergency Fund

How To Start To Create Passive Income Part Ii

Okewon Com Adalah Kasino Online Terbaik Di Indonesia Di Sini Anda Dapat Memainkan Berbagai Permainan Kasino Online Perm Information Center House Rules Casino

Investing For Passive Income 5 Steps For Living Off Dividends Forever

Types Of Income Saving Money Budget Smart Money Financial Tips