Passive Activity Loss Limitations Single

Nasm Study Guide Chapter 2 Basic Exercise Science The Healthy Gamer Study Guide Physical Therapy Assistant Nasm Cpt

Understanding Passive Activity Limits And Passive Losses 2020 Tax Update Stessa

Pin On Sports Ortho Pt

Pin By Terri Nicole On Cpt Program Design Training Plan Hypertrophy Training

Clinical Exercise Physiology 3e Exercise Prescription For Obese Patients Exercise Physiology Physiology Workout Plan For Beginners

Pin On Sports Ortho Pt

Limiting passive activity losses began with the tax reform act of 1986 as a means of discouraging economic activity undertaken strictly as a tax shelter.

Passive activity loss limitations single. The excess business loss limitation applies to the total aggregate income and deductions from all of a taxpayer s trades or. 469 defines a passive activity as. The term was defined in 1986 when the passive activity loss rules went into effect to try to close a tax loophole that allowed high income individuals with substantial on paper passive losses to. Under the passive activity rules you can deduct up to 25 000 in passive losses against your ordinary income w 2 wages if your modified adjusted gross income magi is 100 000 or less.

The passive activity loss rules created a special category of income and loss called passive income or loss. Any trade or business of the taxpayer in which the taxpayer does not materially participate and. Form 8582 passive activity loss limitations is used to calculate the amount of any passive activity loss that a taxpayer can take in a given year. This deduction phases out 1 for every 2 of magi above 100 000 until 150 000 when it is completely phased out.

Single taxpayers may deduct no more then 250 000. Information about form 8582 passive activity loss limitations including recent updates related forms and instructions on how to file. Passive activity loss rules are a set of irs rules that prohibits using passive losses to offset earned or ordinary income. Any rental activity of the taxpayer except as provided under sec.

You can carry over passive activity losses to a future tax year to offset passive activity income in the future. There are two types of passive income or loss. Passive activity loss rules and limitations. Passive activity loss limitations pages 1 2.

Use irs form 8582 passive activity loss limitations to handle reporting of a. Passive activity rules of section 469 irc limits the amount of deductions and credits that taxpayers can claim from passive activities a taxpayer can claim passive activity losses or credits only up to the amount of his passive activity income or tax any excess losses or credits can be carried over to the next year and upon the.

Differences Between Chorea Athetosis And Ballismus Neurological Assessment Huntington Disease Icu Rn

Physical Therapy 9781423203155 Physical Therapy Physical Therapy Student Physical Therapy School

Ohiohealth Spine Patient Education Guide Helpful Info For Pre And Post Op As Well As Physical Activity M Education Guide Patient Education Healthcare System

Best And Simplest Way To Make Sure Your In Your Target Heart Rate Zone Health And Physical Education Exercise Physiology Study Info

Nothing Worthwhile Is Easy What Is Knowledge Life Coaching Tools Personal Success

Strength Training With A Disability Strength Training Mobility Exercises Exercise

Everyone Says Why Don T You Break Up Already That S The Easy Way Out We Re In It Until The End And We Love Each Other So Were Here To Positivity

Pin On Work

Gallery Of Uts Blackfriars Children S Centre Djrd Lacoste Stevenson 1 Colour Architecture Architecture Architecture Awards

Pin On I M A Loser 63 Lbs Lost 42 Lbs To Go

Publication 514 2019 Foreign Tax Credit For Individuals Internal Revenue Service

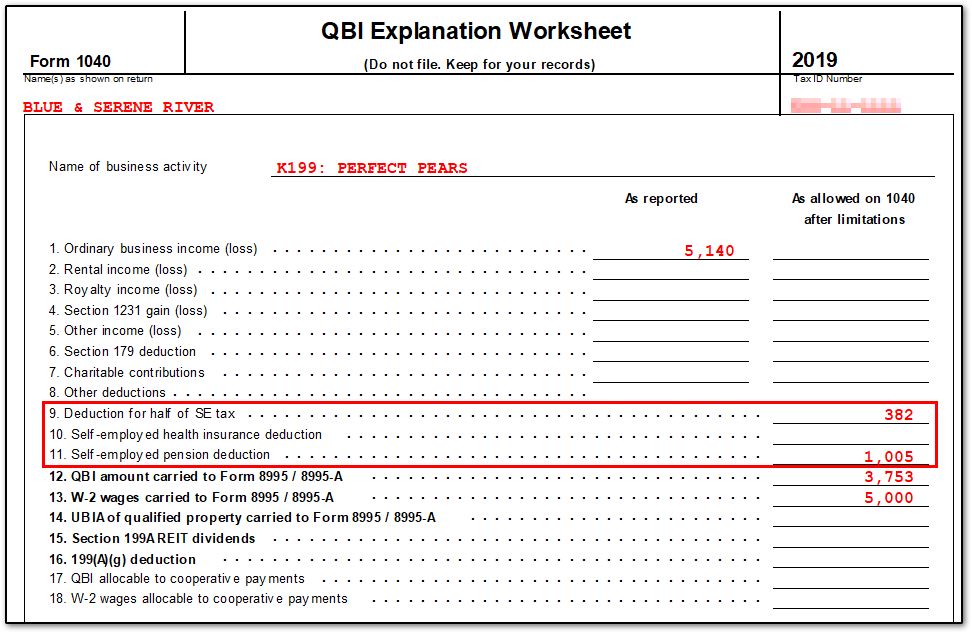

Qbi Deduction Frequently Asked Questions Qbi Schedulec Schedulee Schedulef W2

Deducting Pass Through Business Losses