Passive Activity Loss Ordering Rules

What Are Current Renters Looking For Passive Real Estate Investing Renter Real Estate Investing Investing

This Worksheet Contains 15 Fill In The Blanks Sentences For Students To Practice The Passive Voice In Spanish It Includes Language Teaching Teaching Sentences

Pin On Restaurants In Usa

Agony Aunt Worksheet Free Esl Printable Worksheets Made By Teachers Agony Aunt Conversation Skills Teaching Jobs

Https Www Cpelite Com Wp Content Uploads 2018 08 Passive Loss And At Risk Rules 2 Hrs Pdf

At Risk Limits And Passive Activity Loss Income Tax Course Cpa Exam Regulation Tcja 2017 Youtube

Under the passive activity rules you can deduct up to 25 000 in passive losses against your ordinary income w 2 wages if your modified adjusted gross income magi is 100 000 or less.

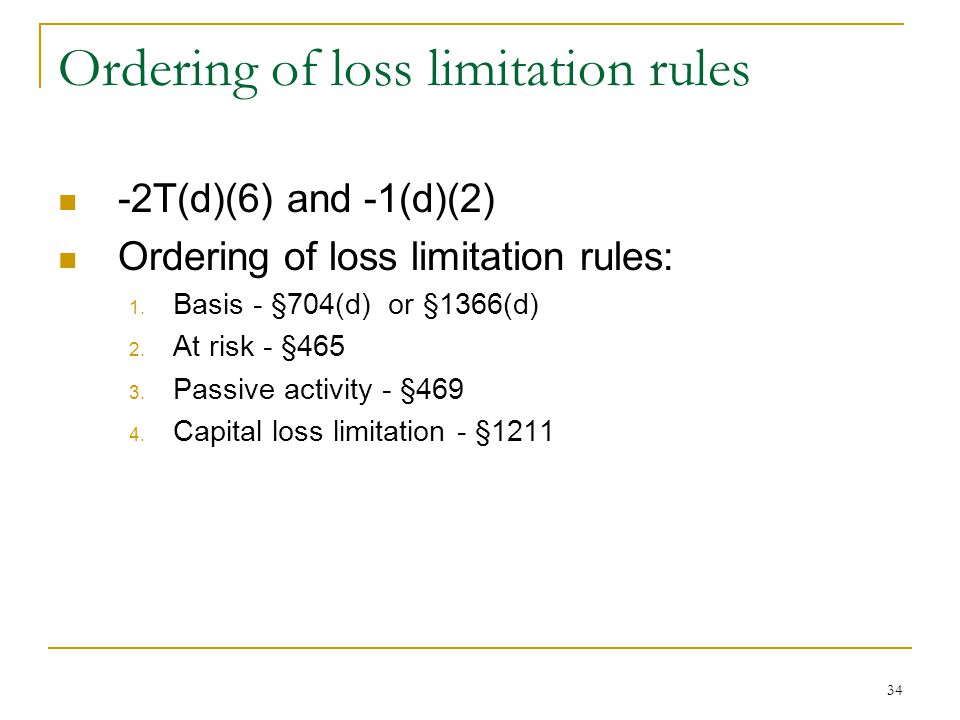

Passive activity loss ordering rules. The passive activity rules apply to individuals estates trusts closely held c corporations and personal service corporations. However the ordering rules require the 25 000 allowance to be first reduced by any passive losses from the rental real estate activities before the credits are applied against it. For shareholders there are ordering rules. First determine if there is sufficient basis then whether the taxpayer is at risk and finally whether the losses are passive.

Passive loss rules ordering rule. Partnership or s corporation basis rules 2. Section 469 a 2 losses and credits attributable to limited partnership interests generally are treated as from passive activities. The portion of passive activity losses attributable to the crd.

Passive activity loss rules are generally applied at the individual level but they also extend to virtually all businesses and rental activity in various reporting entities except c corporations. Special rules apply to rental activities. If you have more than one of the exceptions to the phaseout rules in the same tax year you must apply the 25 000 phaseout against your passive activity losses and credits in the following order. The rules on how to determine a passive activity are pretty straight forward.

Any disallowed loss is carried to the following year return and is treated as incurred in the following tax year. Must contain a declaration that the activities make up an appropriate economic unit for the measurement of gain or loss under the. If there is insufficient basis to absorb losses then the other two limitations need not be considered. That works out to.

If you have more than one of the exceptions to the phaseout rules in the same tax year you must apply the 25 000 phaseout against your passive activity losses and credits in the following order. This deduction phases out 1 for every 2 of magi above 100 000 until 150 000 when it is completely phased out. The rehabilitation credit is also subject to a phaseout range. In order to be considered a non material participant the investor cannot be continuously and substantially active or involved in the business activity.

For partners the allowed loss is allocated pro rata to each category of loss or deduction ordinary 1231 capital gains losses 179 expense etc.

Business Law Study Aid Commonly Used For Bus 241 341 Www Wildcatshop Net Business Law Studying Law Study

1 Irc 469 Passive Activities Part 4 Definition Of Activity Rental Real Estate With Active Participation Real Estate Professionals Interaction With Ppt Download

Pin On Czar S Board

What Are Current Renters Looking For Passive Real Estate Investing Renter Real Estate Investing Investing

Pin On Companies Hiring Work From Home

Passive Activity Loss Rules And Limitations

Real Life Examples Of Integers Integer Activity In 2020 Integers Integers Activities Integers Real Life

Primerica Business Card Design 2 Business Card Design Business Cards Card Design

What Are Current Renters Looking For Passive Real Estate Investing Renter Real Estate Investing Investing

The Benefits Of Tutoring Infographic Tutoring Business Tutor Math Tutor

Instructions For Form 8990 05 2020 Internal Revenue Service

Trashketball Template Any Subject With Auto Timer Trashketball Timer Templates

Usborne Books More See Inside Your Body Ir Flap Book The Body Book Child Life Specialist