Passive Income Definition Oecd

Http Www Taxand Com Wp Content Uploads 2019 07 5 Passive Income 2019 Pdf

The Latest Trend In Macro Variables Economics Macro Variables Economics Https Macro Economic Com The Latest Trend In Macro Variab In 2020 Macro Economics Variables

Robottradingsystem Com System By Justmyname Myfxbook Investment Advice Trading Signals Financial Advisors

The Latest Trend In Macro Variables Economics Macro Variables Economics Https Macro Economic Com The Latest Trend In Macro Variab In 2020 Macro Economics Variables

Fxdreema Ea Builder

Https Www Oecd Ilibrary Org Income Inequality And Poverty In Colombia Part 1 The Role Of The Labour Market 5k487n74s1f1 Pdf

Further information analytical publications oecd 2012 oecd economic.

Passive income definition oecd. It is for that reason that gdp per capita is the most widely used indicator of income or welfare even though gni is theoretically superior. Active vs passive income 2. You collect passive income from certain businesses in which you aren t an active participant. Passive income when used as a technical term is defined as either net rental income or income from a business in which the taxpayer does not materially participate and in some cases.

Concept of beneficial ownership 6. Oecd mc article 11 includes a comprehensive definition of interest for treaty purposes. Of course in a number of situations the recipient may induce or coerce the briber and in that sense is the active party. Definitions of the standardised categories and sub categories of labour market programmes oecd 2001.

Disposable income in the system of national accounts is equivalent to the economic theoretic concept. It means income from debt claims of every kind including bonds and debentures. Dividends interest rental income royalties etc. Active by reason of income and assets.

Pass through entity a nontaxable entity such as a partnership. Income as it is generally understood in economics is theoretically defined as the maximum amount that a household or other unit can consume without reducing its real net worth. Salaries and property income and of depreciation. Passive or income maintenance programmes in the context of labour market programmes consist of unemployment compensation programmes and programmes for early retirement for labour market reasons.

Oecd model oecd model prefers tax incidence wholly in the. Passive bribery is the offence committed by the official receiving the bribe. Less than 50 of the entity s gross income for the preceding calendar year or other appropriate reporting. Sources oecd 2012 national accounts of oecd countries oecd publishing.

The technical fees fits the definition of a royalty and. Attribution of taxing rights a. Generally the income or expense is passed to the underlying owner.

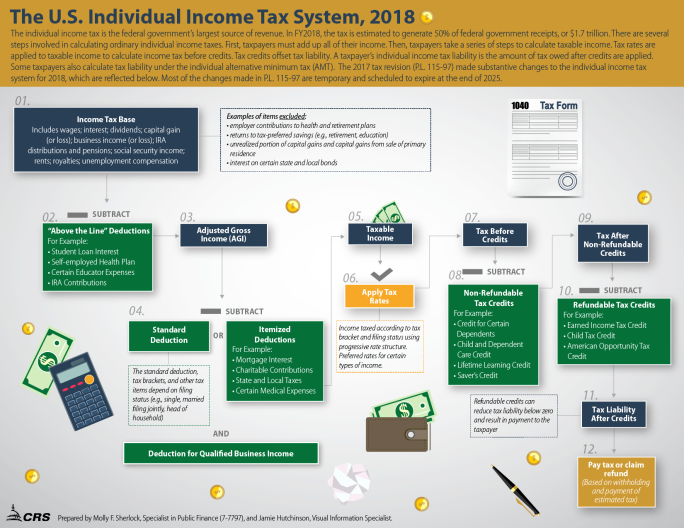

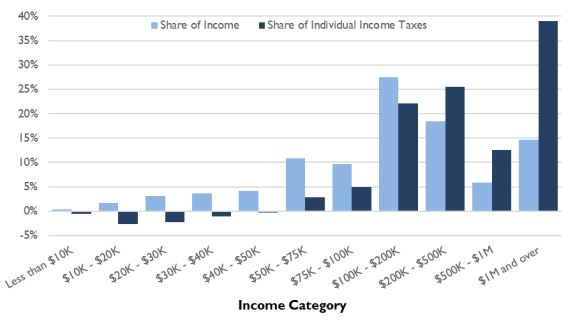

Overview Of The Federal Tax System In 2018

Fxdreema Ea Builder

Titan Educacao Seja Um Consultor Titan Educacao E Ofereca Conhecimento A Distancia Cursos Online Titan Educacao Em Educacao Cursos Online Ensino A Distancia

Titan Educacao Seja Um Consultor Titan Educacao E Ofereca Conhecimento A Distancia Cursos Online Titan Educacao Em Educacao Cursos Online Ensino A Distancia

Https Www Oecd Org Finance Esg Investing Practices Progress Challenges Pdf

Https Www Oecd Ilibrary Org Economics Income Wealth And Equal Opportunities In Sweden E900be20 En Crawler True Mimetype Application Pdf

Https Taxpolicy Crawford Anu Edu Au Sites Default Files Publication Taxstudies Crawford Anu Edu Au 2020 03 Complete Sainsbury Breunig Wp1 Mar 2020 Pdf

Overview Of The Federal Tax System In 2019 Everycrsreport Com

Https Www Bnz Co Nz Assets Business Banking Help Support Frequently Asked Questions V4 Pdf 8434e7684583139e7b9fd60d624d23fe8dbcb18a

Https Www Productivity Govt Nz Draft Report 2 Employment Labour Markets And Income