Passive Income Small Business Grind

5 Passive Income Business Models In 2020 Passive Income Business Business Business Ideas Entrepreneur

6 Ways To Make Passive Income Double Tap Tag A Friend Follow Awokenmindset Entrepr Online Business Marketing Online Business Business Ideas Entrepreneur

Passive Investment Income And The Small Business Deduction Grind Adrian Joseph Cpa

Don T Be Passive About Canada S New Passive Income Rules Advisor S Edge

Passive Income Investing Money Money Financial Investing

Https Advisors Td Com Saverio Veltri Mediahandler Media 313770 410 18 Passive Investment Income En1 Pdf

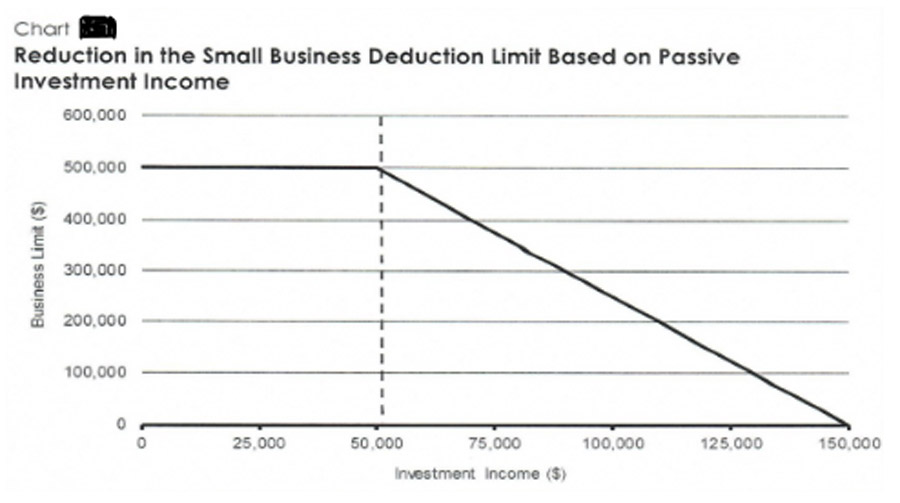

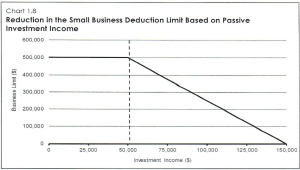

Until 2018 the first 500 000 of active business income earned by canadian controlled private corporations ccpcs was eligible for the small business deduction sbd and a lower federal tax.

Passive income small business grind. A ccpc s passive income business limit reduction for a particular taxation year will be the amount determined by the formula. In addition a small canadian controlled private corporation ccpc. Bl 500 000 x 5 aaii 50 000 where. Under this formula the sbd will be eliminated when investment income reaches 150 000 in a given taxation year.

Merrick also suggests using passive income to invest in growth assets such as real estate that realize less taxable annual income. It is the prior year s passive income level which impacts the current year business limit grind. These new cra passive income changes will first apply to fiscal years that start in 2019 and will reduce the maximum small business deduction available to a ccpc or associated group of ccpcs by 5 for every 1 of passive investment income earned in the previous fiscal year in excess of 50 000. Passive income includes interest dividends mutual fund income capital gains and most rental real estate income.

Under the proposals the small business limit will be reduced by 5 for every 1 of investment income above a 50 000 threshold. Most significantly a corporation that earns more than 50 000 of investment income will suffer a reduction in its small business deduction limit the grind for taxation years beginning after 2018. Beginning in 2019 as your passive income increases there is a corresponding decrease in the amount of your active business income that can be taxed at the small business tax rate. Passive investment income budget 2018 active business income earned by private corporations is taxed at corporate income tax rates that are generally lower than personal income tax rates giving these corporations more money to invest in order to grow their business.

The chart below shows the reduction of the small business limit at selected passive income levels. The result in most cases in ontario is corporate tax applied at a rate of 26 5 versus 12 5 to the first 500 000 of active business income which can make a huge impact on many small businesses. Passive investment income and the small business deduction grind. As mentioned we take each dollar above the limit.

Let s say a corporation has earned 80 000 in passive income. That is 30 000 over the 50 000 limit. Let s look at another example where the amount of passive income is greater thus reducing the amount of the small business deduction. Bl is the ccpc s business limit otherwise determined for the particular year i e its business limit as described above.

How To Generate A Passive Income Hustle Business Motivation Inspiration Inspirational Tip Money Management Advice Investing Money Business Motivation

Active Vs Passive Income Start Online Business Facebook Ads Cost Investing

Entrepreneurship Mindset On Instagram Active Vs Passive Income Waking Up In The Morning Seeing In 2020 Money Management Advice Financial Motivation Business Money

Passive Income Ideas Follow Me On Instagram Tipsfreetips Official For A New Business Idea Business Ideas Entrepreneur Business Money Business Motivation

Passive Income Ideas For 2020 In 2020 Passive Income Quotes Passive Income Cashflow Quadrant

Passive Investment Rules And Small Business Deduction Life Care Insurance

Passive Income Ideas To Make Money Smartly Business Ideas Entrepreneur Business Money Money Management Advice

The Best Business Books For Entrepreneurs Follow Me On Instagram Tipsfreetips Official For A New Busines Business Books Entrepreneur Books Start Up Business

The Small Business Clawback Wiim

Pin On Success

Pin On Passive Income For Beginners Side Hustle Tips

The Average Millionaire Has 7 Sources Of Income Here S Some Ideas For You If Any Of You A Business Ideas Entrepreneur Business Money Small Business Success

4 More Creative Ways To Earn A Passive Income In 2020 Business Motivational Quotes Success Quotes Business Quotes Inspirational Deep