Passive Income Vs Unearned Income

Pin On Financial Planning

:max_bytes(150000):strip_icc()/dotdash_Final_Investment_Income_Apr_2020-01-fae8874a0f0c4ab38e8e3cc18801e803.jpg)

Investment Income Definition

Bing Ads Coupon Code Worth 100 Unlimited Method 2020 Coding Ads Online Work From Home

Profit Vs Income 5 Most Valuable Differences To Learn

What Are The 3 Types Of Income How To Fire

Beginning Accounting Can You Take A Look At This Accounting Accounting Jobs Accounting Notes

Another disadvantage in regards to taxes when it comes to earned income is the limited amount of deductions available.

Passive income vs unearned income. Earned income to understand the difference between unearned income and earned income you need to understand the meaning of income on its own. It comes in without any required physical activity on your part. We re talking about income that follows its own course this is the main distinction between passive vs. Passive income includes regular earnings from a source other than an employer or contractor such as being paid book royalties or stock dividends.

Earned income is sometimes referred to as active income. In regard to the tax specifications it is more advantageous to focus on ways of producing passive income as opposed to concentrating on generating non passive income. The principals and methods governing the three are substantially different and most importantly the rules relative to taxation are different as well. In some cases this income is taxed differently.

Unearned income is income that is not earned meaning it is derived from another source such as an inheritance or passive investments that earn interest or dividends. Unearned income is money that you receive without doing work for it. One of the most common types of unearned income is interest income or dividends from an investment. Other types include real estate rents child support unemployment earnings.

Unearned income is money that you take in passively. Many people equate unearned income with passive income. While passive and portfolio are income is generated via investments earned income is either employment w2 or self employment 1099 income. In some cases this type of income is passive.

That s known as active. Both are forms of unearned income that is funds you didn t personally work for or come directly from your labor or services. Your income affects your tax liability your ability to contribute to retirement accounts and your social security benefits so it s important to understand the different types of income and how the irs treats them. When compared to passive income deductions on earned income are less plentiful.

With passive income you do not work for the money. A closer look at unearned income vs. It takes a lot of work on the front end to reap.

Map Where 100 000 In Retirement Savings Will Last The Longest In 2020 Saving For Retirement Retirement States

What Is Miscellaneous Income Business Overview

Passive Income Definition

Learn The Meaning Of Post Trial Balance At Http Www Svtuition Org 2013 07 Post Closing Trial Balance Html Trial Balance Accounting Education Learn Accounting

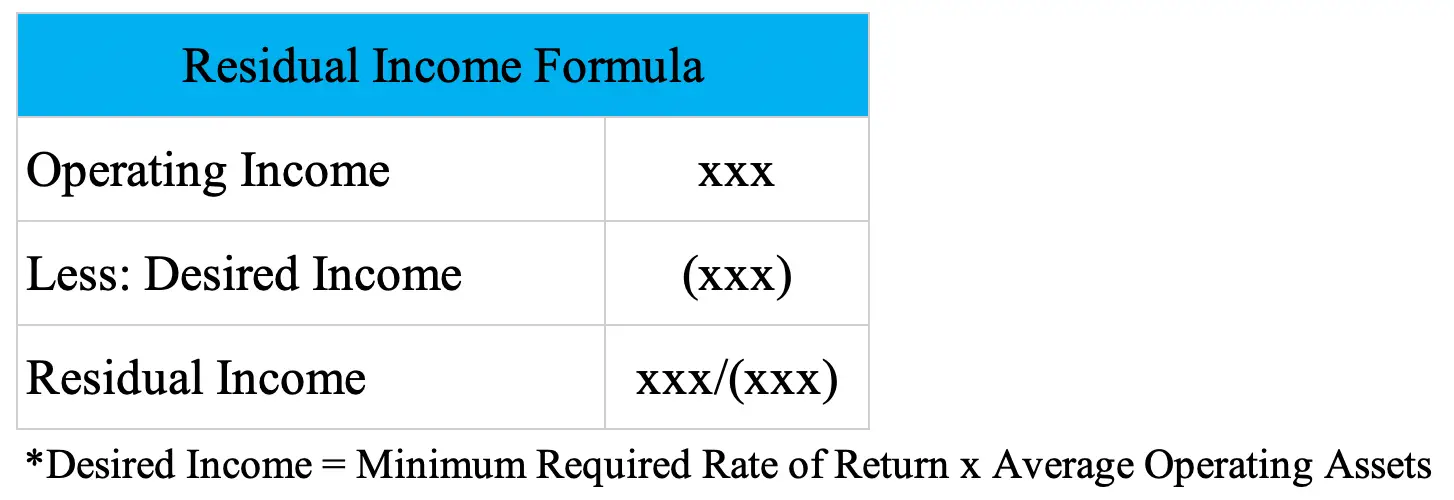

Residual Income Formula Example Accountinguide

Taxes From A To Z 2019 K Is For Kiddie Tax

The Essential Guide To Direct And Indirect Cash Flow Cash Flow Cash Flow Statement Flow

10 Ways The Rich Avoid Taxes Visual Capitalist Economy Blockchain Changing Jobs

Layering Desert Recipes Desert Map Deserts In The Us

Pin On Cake Business Advice

Sample Chart Of Accounts For A Web Based Craft Business Chart Of Accounts Craft Business Accounting

Profit Road Sign With Cloudy Sky Ad Road Profit Sign Sky Cloudy Ad With Images Tax Free Weekend Life And Health Insurance

Pin On Roberta Cannon