Passive Loss Aggregation Rules

Differential Features And Significance Of Necrosis And Apoptosis Health Insurance Quotes

Understanding Passive Activity Limits And Passive Losses 2020 Tax Update Stessa

Https Assets Kpmg Content Dam Kpmg Us Pdf 2020 02 Reviewing Your K 1 Draft Package Pdf

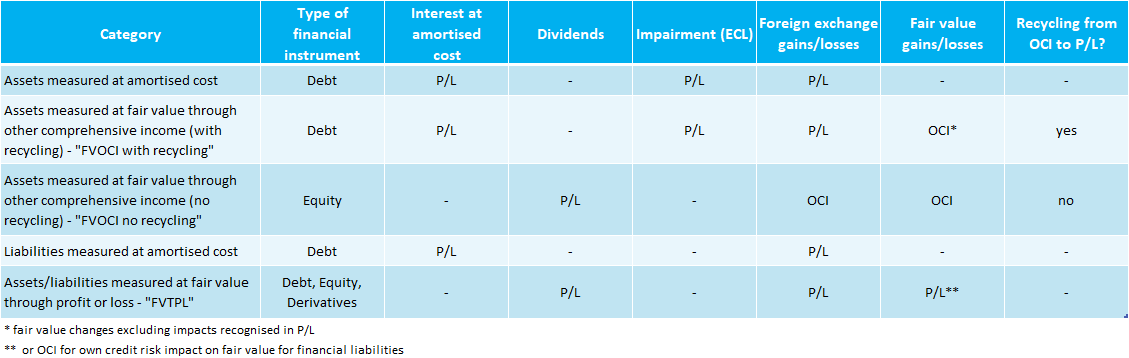

Classification Of Financial Assets Liabilities Ifrs 9 Ifrscommunity Com

Https Www 3iscorp Com School Wp Content Uploads Pdf Courses Self Study California Module 4 Study Text Pdf

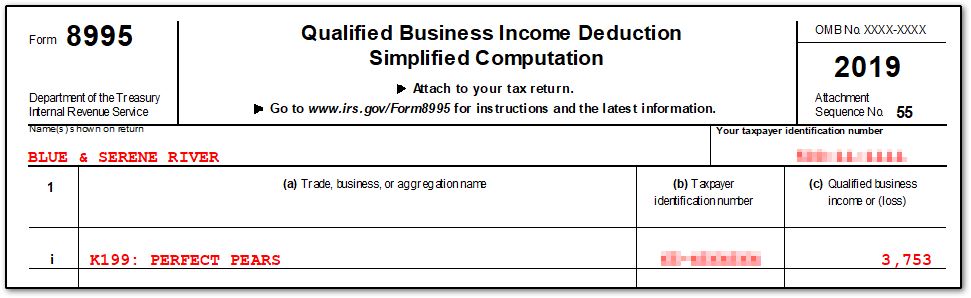

Instructions For Form 8995 2019 Internal Revenue Service

If your real estate rental income generates a net loss.

Passive loss aggregation rules. However your deduction of suspended losses may be limited by the passive loss rules. Introduction for persons dealing with real estate property the use of the aggregation election to meet the material participation test may have a significant impact on their tax liability. In its decision in hardy t c. Under the rule any rental losses are still considered passive but the rental income is deemed nonpassive.

Aggregation can be a liability if a formerly passive rental property carries large previously disallowed losses that are not likely to be absorbed by income from other properties or if the qualifying real estate professional wants to sell the loss property. For taxation purposes the irs looks at your annual income in terms of net gain or loss. Activities described in 6 under activities covered by the at risk rules earlier that constitute a trade or business are treated as one activity if. In general if a taxpayer s aggregate losses from passive activities exceed the taxpayer s aggregate income from passive activities for the taxable year the excess losses may not be deducted against other income for that taxable year.

The self rental rule in irc section 469 applies when you rent property to a business in which you or your spouse materially participates. Passive activity loss rules. An passive activity loss rules. The passive loss rules.

The passive activity loss rules created a special category of income and loss called passive income or loss. Passive income is generated from property rentals and investments in which you do not participate in the ongoing activities of the business. There are two types of passive income or loss. Passive income or loss comes from.

Active income loss is more attractive than passive income loss to. Passive activity loss rules. Using suspended passive losses. The election applies for all pal purposes including the disposition rules.

2017 16 the tax court held that a taxpayer had not elected to group two activities together under the passive activity loss rules simply by treating both activities as nonpassive notably as the tax court pointed out the irs and the taxpayer each took tax positions more commonly argued by the opposing side as the taxpayer a surgeon sought to be treated. All rental properties you own. That means your self rental profits can t be offset by passive losses and the self rental losses. Such excess losses are suspended and are carried forward to be treated as.

2395 words 10 pages.

At Risk Limits And Passive Activity Loss Income Tax Course Cpa Exam Regulation Tcja 2017 Youtube

Https Www Irs Gov Pub Irs Utl 2019ntf 01 Pdf

Qbi Deduction Frequently Asked Questions Qbi Schedulec Schedulee Schedulef W2

Https Www2 Deloitte Com Content Dam Deloitte Jp Documents Tax It Jp Bt Japan Tax Newsletter 12december2016 International En Pdf

Irs Releases Final Gilti Regulations Grant Thornton

Instructions For Form 8990 05 2020 Internal Revenue Service

Instructions For Form 5471 02 2020 Internal Revenue Service

Https Www Irs Gov Pub Irs Prior I8582 2018 Pdf

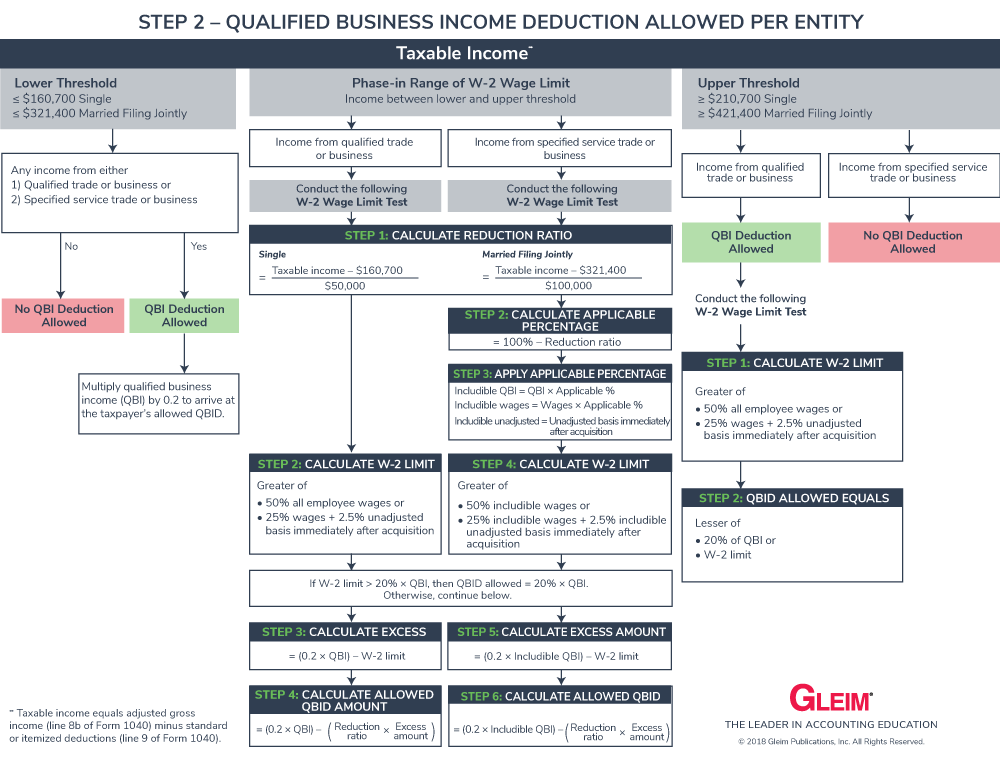

Section 199a Qualified Business Income Deduction Qbid Gleim Exam Prep

Pfics Rules Initial Impressions And Observations Kpmg United States

Https Sales Johnhancockinsurance Com Content Dam Jhins Documents Life Advanced Markets1 Because You Asked Life 7154 Taxation Of Life Insurance Pdf

Http Media Straffordpub Com Products Real Estate 199a Aggregation And 469 Grouping Rules Real Estate Professionals And Safe Harbor Election 2019 07 02 Reference Materials Pdf