Passive Loss Limitation Rules 2018

Small Business Accounting Cheat Sheet Important Info Small Business Accounting Small Business Tax Business Account

Health Insurance Tax Benefits Under Section 80d For Fy 2018 19 Ay 2019 20 Health Insurance Tax Deductions Best Health Insurance

The Complete Guide To Bookkeeping For Small Business Owners Blogging Tips For Sma Small Business Organization Bookkeeping Business Small Business Bookkeeping

Tax Deduction Guide For Retirees And Elderly People Tax Deductions Money Stories Deduction Guide

Pdf Download Every Landlord S Tax Deduction Guide Free Epub Mobi Ebooks Being A Landlord Tax Deductions Deduction Guide

How The New Tax Law Affects Rental Real Estate Owners Mitchell Wiggins

Although the basic ordering of the various loss limitation rules is clear the exact manner in which these rules should be coordinated is uncertain.

Passive loss limitation rules 2018. They remain in place. To the passive loss limitations. He has no other business or rental activities. Information about form 8582 passive activity loss limitations including recent updates related forms and instructions on how to file.

Once a loss becomes allowable under these other limitations you must determine whether the loss is limited under the passive loss rules. Dave is an unmarried individual who owns two strip malls. A passive activity is one wherein the taxpayer did not materially. Passive activity rules restrict the deduction of passive activity losses.

Losses and deductions passed through and allowed as a deduction under the basis rules and at risk rules. Further assume that the loss. The cares act temporarily modifies the loss limitation for noncorporate taxpayers so they can deduct excess business losses arising in 2018 2019 and 2020. See form 6198 at risk limitations for details on the at risk rules.

The tax cuts and jobs act tcja the massive tax law enacted by congress that took effect in 2018 did not alter the passive loss rules. For instance assume a taxpayer operates two businesses business a and business b both of which operate at a loss. Also capital losses that are allowable under the passive loss rules may be limited under the capital loss. Passive activity loss rules are a set of irs rules stating that passive losses can be used only to offset passive income.

Form 8582 is used by individuals estates and trusts with losses from passive activities to figure the amount of any passive activity loss pal allowed for the current tax year. Passive activity loss limitation. In 2018 he has 500 000 of allowable deductions and losses from the rental properties after considering the pal rules and only 200 000 of gross income. You may only deduct passive losses from passive income.

The passive loss rules also apply to any activity in which a taxpayer does not materially participate as well as to most rental activities. 461 l 1 as amended by act. Losses and credits that a taxpayer cannot use because of the passive loss limitation rules are suspended and carry over indefinitely to be offset against future passive activity income from any. Loss limitation rules in the real world.

If a loss exceeds your at risk investment the excess is a suspended loss and may be carried to future years indefinitely and deducted when there is sufficient at risk basis to absorb the loss.

Pin On Income Tax India

Cbse Sample Paper For Class 11 Accountancy With Solutions Sample Question Paper Past Exam Papers Sample Paper

Form Nol For 2018 Is Now Available Montana Department Of Revenue

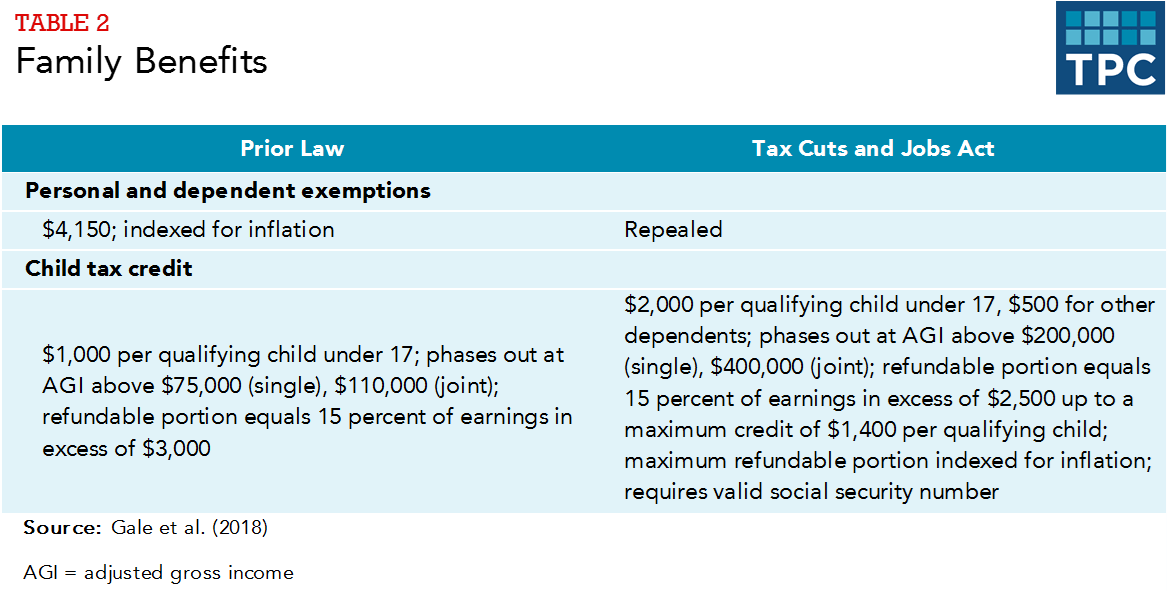

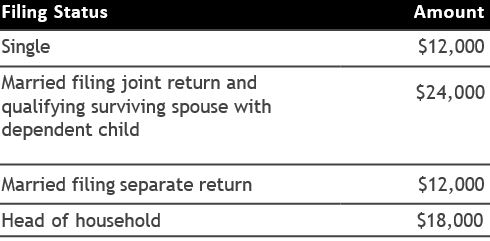

How Did The Tax Cuts And Jobs Act Change Personal Taxes Tax Policy Center

9 Rules Of Successful Dividend Investing Dividend Investing Investing For Retirement Dividend

Https Www Irs Gov Pub Irs Prior I1045 2018 Pdf

Publication 514 2019 Foreign Tax Credit For Individuals Internal Revenue Service

How The New Tax Law Affects Rental Real Estate Owners

Call Your Local Representatives Tell Them To Vote No On The Proposed New Tax Bill Tax Services Income Tax Return Tax Rules

2018 Year End Tax Planning For Individuals Smith Howard

Https Www Irs Gov Pub Irs Prior I6251 2018 Pdf

Days Working Capital Formula Calculate Example Investor S Analysis Financial Analysis Business Tax Deductions Business Management Degree

Binance Research Ethereum Actively Powering The Defi Ecosystem Btcmanager In 2020 Financial Instrument Derivatives Trading Bitcoin