What Is Passive Income Excess Limit

45 Mel Robbins Quotes 190802 Poster In 2020 Investing Money Investing Finance Investing

Business Productivity Tips Singapore Motivation Entrepreneur Motivation Self Care Activities

Pin On Dividend Income Spreadsheet

Pin By Gerald Unkovich On Be Successful New Things To Learn Business Motivation Self Improvement Tips

Pin By Aaron On Daily Planner In 2020 Business Motivation Successful People Self Improvement Tips

Improve Yourself In 2020 Business Motivation Motivation Self Improvement Tips

Passive income when used as a technical term is defined as either net rental income or income from a business in which the taxpayer does not materially participate and in some cases.

What is passive income excess limit. In particular passive losses are typically deductible only against passive income and you re not able to claim excess passive losses immediately instead having to carry them forward. If the business does generate more than 25 percent of its receipts from passive income the excess is taxed at the highest corporate income rate. However net rental income can be essentially reduced to zero through cca capital cost allowance property depreciation but is recaptured when you sell the property. These new cra passive income changes will first apply to fiscal years that start in 2019 and will reduce the maximum small business deduction available to a ccpc or associated group of ccpcs by 5 for every 1 of passive investment income earned in the previous fiscal year in excess of 50 000.

You can carry back the foreign tax credit to the immediately preceding tax year or carry forward the credit for the next 10 tax years. For example if an s corporation earns 100 000 in a year 35 000 of which is from passive income the total passive income percentage for the year would be 35 percent. Excess net passive income is a corporate level tax on the passive income earned by an s corporation. Passive activity loss rules are a set of irs rules stating that passive losses can be used only to offset passive income.

Passive income includes income from interest dividends annuities rents and royalties. This deduction phases out 1 for every 2 of magi above 100 000 until 150 000 when it is completely phased out. Excess net passive income tax. The following table illustrates how the sbd is affected depending on the level of passive.

A passive activity is one wherein the taxpayer did not materially. Under the passive activity rules you can deduct up to 25 000 in passive losses against your ordinary income w 2 wages if your modified adjusted gross income magi is 100 000 or less. Once passive investment income earned by the group exceeds 150 000 the ability to claim the sbd is eliminated. For every 1 of passive income earned over the new 50 000 threshold by an associated group of companies the sbd limit will be reduced by 5.

How To Get Started In Stocks With Robinhood Investing Apps Finance Investing Investing Money

Here S A Simple Explanation As To Why Ripple Xrp Has So Much Potential Cryptocurrency Trading Bitcoin Cryptocurrency Bitcoin

Http Www Medicaresupplementplans2016 Com Medicare Supplement How To Plan Aarp

Passive Income Is My Game Money Life Goals Quotes Black Ipad Case Skin By Wintre2 Life Goals Quotes Goal Quotes

Pin On Blog

The Step By Step Guide To Get Out Of A Timeshare Timeshare Getting Out Travel Strategy

Don T Be Passive About Canada S New Passive Income Rules Advisor S Edge

Investing Through A Professional Corporation Physician Finance Canada

Interest Paid By Muthoot Finance In Excess Of Statutory Limit Held As An Exp Prohibited By Law Not Allowable 2013 Finance Vodafone Logo Tech Company Logos

How To Research 50a2cf7bde690 Research Methods Educational Technology Online Infographic

Pin By The Next Trip Travel And Fa On Travel Tips The Next Trip Blog In 2020 With Images Traveling By Yourself

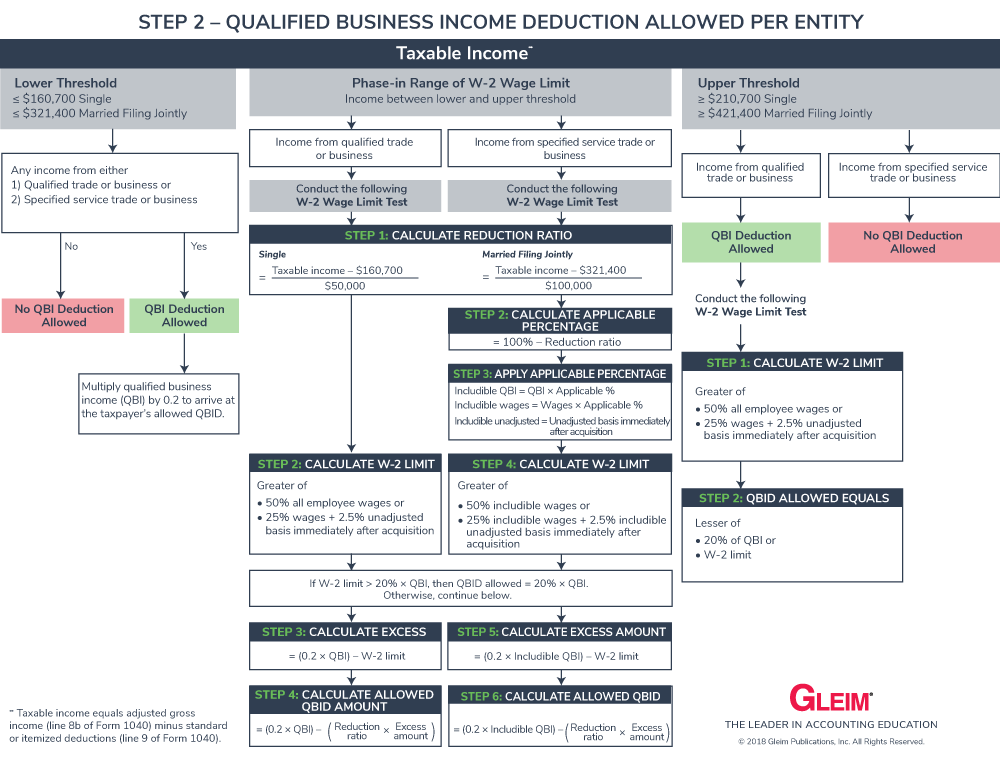

Section 199a Qualified Business Income Deduction Qbid Gleim Exam Prep

Publication 514 2019 Foreign Tax Credit For Individuals Internal Revenue Service