Passive Activity Loss Vs At Risk Rules

Application Of The Tax Basis And At Risk Loss Limitations To Partners

Pin On Forex Trading

Pin On Quotes

Https Www Oataxpro Com Assets Files Presentations Be 19 Basis And At Risk Rules For Partnerships Pdf

Publication 925 Passive Activity And At Risk Rules Comprehensive Example

Publication 527 Discusses Rental Income And Expenses Including Depreciation And Explains How To Report Them On Your Retu Rental Income Rental Property Public

See publication 925 passive activity and at risk rules.

Passive activity loss vs at risk rules. Only the amount that does not exceed basis should be carried to the next step main form form 6198 or form 8582 as the case may be. See passive activity deductions later. If a passive loss exceeds passive income in any tax year the excess loss may be carried over to the following tax year. Publication 925 passive activity and at risk rules passive activity and at risk rules passive activities.

Under the basis excess farm loss or at risk rules. The limits imposed by irs rules dealing with basis at risk activity and passive activity are applied in that specific order. Generally the passive activity loss for the tax year isn t allowed. At risk rules vs passive activity rules.

At risk rules limit the amount of a business loss you may deduct in any given tax year. However there is a special allowance under which some or all of your pas sive activity loss may be allowed. The second part discusses the at risk rules. Under the passive activity rules you can deduct up to 25 000 in passive losses against your ordinary income w 2 wages if your modified adjusted gross income magi is 100 000 or less.

If you merely invest in a business and do not actively participate in the day to day operations losses are classified as passive losses. However when you figure your allowable losses from any activity you must apply the at risk rules before the passive activity rules. This deduction phases out 1 for every 2 of magi above 100 000 until 150 000 when it is completely phased out. Passive losses may only be deducted from passive income.

The first part of the publication discusses the passive activity rules.

Trading Isnt Gamblingif Your Wisdom Says It Is One And The Same Check Out The Difference Here Hit Like If You Agree In 2020 Trading Charts Forex Trading Quotes Trading Quotes

Forex Signals In 2020 Trading Quotes Investment Quotes Forex Signals

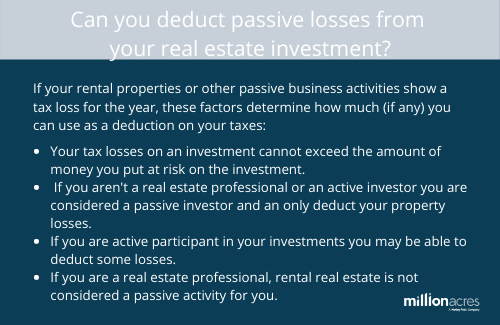

Can I Deduct Passive Losses From Real Estate Investments Millionacres

Forex Trading Tips Easy Ways To Improve Fx Trading Forex Trading Education Forex Trading Tips Forex Trading

Pin On Stock Trading Guide

Rules Of Money Comment Your Favorite One Follow Financialintellect Fo Money Management Advice Investing Money Money Financial

Physical Activity Is Incredibly Important For Your Overall Health But It Doesn T Have To Look Like Exercise What Physical Activities Activities Senior Health

Pin On Complex Trauma

If Poem Rudyard Kipling If Rudyard Kipling Words Trust Yourself

Getjoemoneyright Citation Motivation Rules Regle Business Entrepreneur Mindset Focus Goal Faire De L Argent En Ligne Faire De L Argent Apprentissage

Home Wetalktrade What It Really Takes To Taste Forex Success Trading Stocks Ideas Of Trading In 2020 Forex Trading Quotes Trading Quotes Forex Trading Training

Entrepreneur Entrepreneurs Entrepreneurslife Millionaire Millionairemindset Milli Money Management Advice Personal Finance Articles Money Saving Plan