Passive Income Offset Passive Loss

Pin By Financial Shaper On Monthly Dividend Income Dividend Income Income Passive Income Streams

You Either Need Cash Or Time To Create Passive Income There Are Many Ways To Achieve Financial F Start Online Business Creating Passive Income Online Business

Pin By Financial Shaper On Monthly Dividend Income Dividend Dividend Income Financial

Best Passive Income Investments 2019 Foxy Monkey

Passive Income Ideas Passive Income What Is Passive Income Passive

Understanding Passive Activity Limits And Passive Losses 2020 Tax Update Stessa

Passive activity loss rules are a set of irs rules stating that passive losses can be used only to offset passive income.

Passive income offset passive loss. To qualify your modified adjusted gross income must not exceed 100 000 for the year. The term was defined in 1986 when the passive activity loss rules went into effect to try to close a tax loophole that allowed high income individuals with substantial on paper passive losses to. So if you have a passive loss from a passive activity and nonpassive income from a nonpassive activity such as a sole proprietorship that you own and run you would not be allowed to deduct a loss from the passive activity from a net profit of the sole proprietorship. A limited partner is generally passive due to more restrictive tests for.

This deduction phases out 1 for every 2 of magi above 100 000 until 150 000 when it is completely phased out. If the current year non passive activity triggers deductibility of prior year suspended passive activity losses irc 469 f permits a prior year passive loss to offset current year income from the same activity even though that income might be non passive in the current year. As a result of this combination of income and losses the beechers paid no tax on the rental income paid to them by their corporations this amounted to over 85 000 of tax free income over three years. While net income or gain on sale is non passive it may be used to trigger prior year passive losses or credits from.

A passive activity is one wherein the taxpayer did not materially. There are limited partnerships that might pass passive income through a k 1. If you are the owner or landlord of a rental property a special rental loss offset lets you apply up to 25 000 of passive activity losses against your normal income. In a given year she earns 3 000 as her share of partnership profits.

You may not offset passive losses against nonpassive income. Before the passive activity rules these investors were allowed to offset other income like dividends interest and salaries and wages with these losses. They would use this lease income ordinarily passive income to offset the losses from their rentals. The losses can also be claimed to offset gains at the 4me of sale of the equity interest.

Under the passive activity rules you can deduct up to 25 000 in passive losses against your ordinary income w 2 wages if your modified adjusted gross income magi is 100 000 or less. Rentals and businesses without material participation. At the same 4me tina is a passive investor in an s. According to the irs.

Passive losses are only offset by passive income not income from stocks bonds interest and dividends.

Proven Ways On How To Make Money Online Faq What Are The Ways On How To Make Money Online Beradiva Beradiva Proven Ways On How To Make Money Online Beradiva

How Is Passive Income Taxed Free Investor Guide

Rental Property Tax Deductions Real Estate Rentals Being A Landlord Property Tax

How To Earn Money Without Skills Full Time Income Part Time Income In 2020 Earn Money Income Business Management

Passive Income Definition

Which Geoup Would You Pick Comment Bellow In 2020 Dividend Dividend Stocks Business Money

Increasing Passive Activity Loss Deductions With Self Charged Interest

Claiming A Business Loss On Taxes Can Schedule C Losses Offset W 2 Income Or Do The Hobby Loss Rules Prevent This Personal Finance Bloggers Personal Finance Finance Bloggers

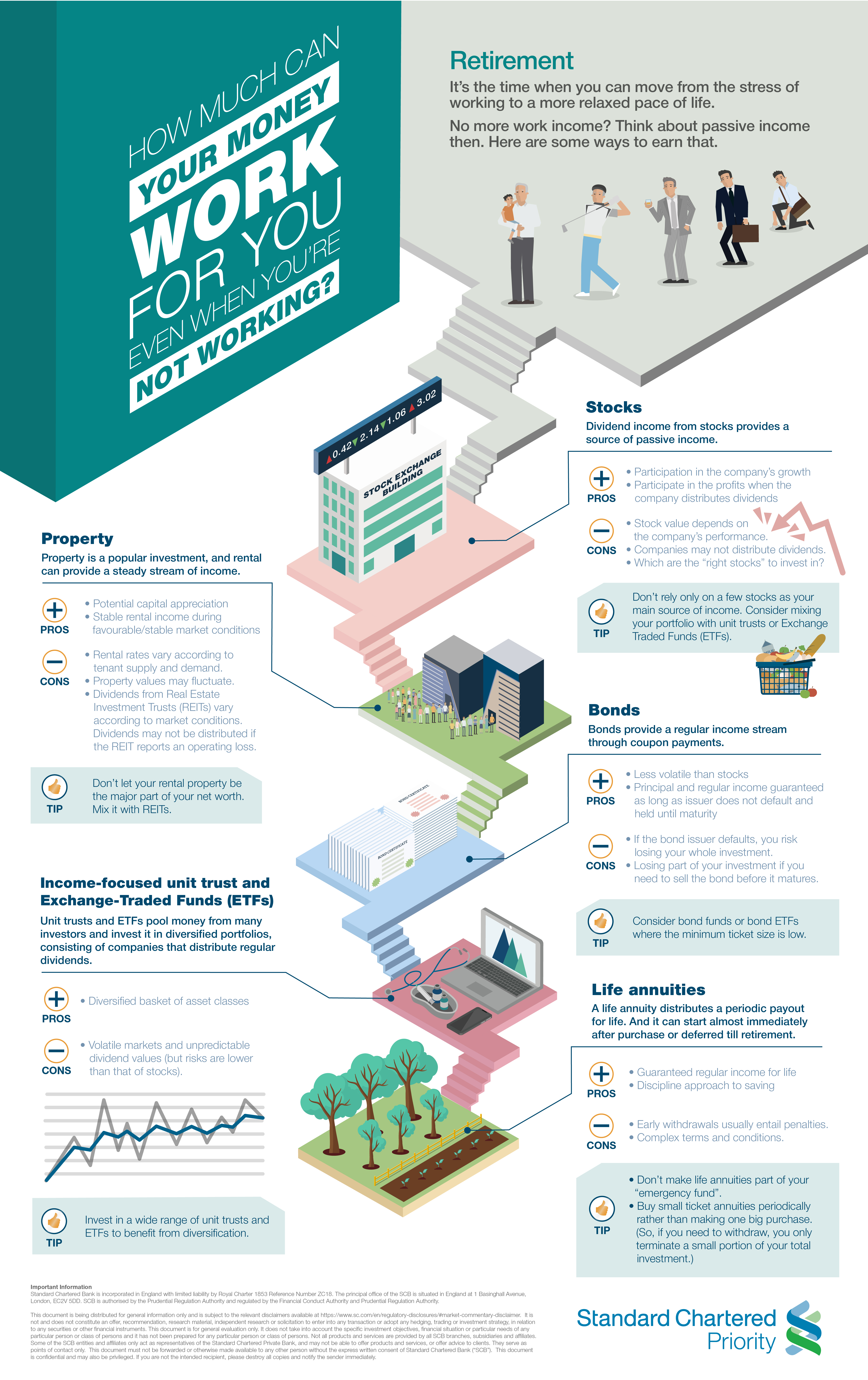

Passive Income For Retirement Standard Chartered Singapore

Passive Income Thin Line Pixel Perfect Stock Vector Royalty Free 1114935044

Passive Activity Credits And Recharacterized Income

Passive Income For Christmas Something 2 Offer Ways To Save Money Money Spending Money

9 Passive Income Ideas That Earn 1000 Per Month Gillian Perkins