Passive Loss Rules Apply To All Corporations

Passive Activity Credit Flowchart

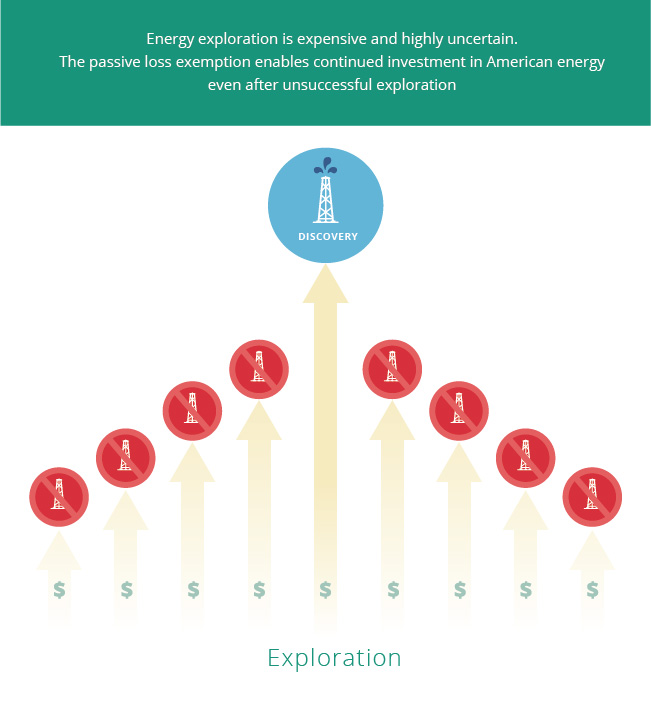

Passive Loss Exception Energy Tax Facts

Increasing Passive Activity Loss Deductions With Self Charged Interest

Passive Activity Credits And Recharacterized Income

Why Passive Activities May Be Clean Energy S Biggest Hurdle Institute For Local Self Reliance

Can You Deduct Your S Corporation Losses Passive Activity Loss Rule

The passive activity loss rules also apply to any items passed through to you by partnerships in which you re a partner or by s corporations in which you re a shareholder.

Passive loss rules apply to all corporations. This means that any losses passed through to you by partnerships or s corporations will be treated as passive as part of the partnership taxation. An associated regulation defining certain passive activities including rental activities specifies. Passive activities are trades businesses or income producing activities in which you don t materially participate the passive activity loss rules also apply to any items passed through to you by partnerships in which you re a partner or by s corporations in which you re a shareholder. The pal rules apply to all business activities but are particularly strict for real estate rentals because they were the primary tax shelter.

Passive income or loss comes from. The court acknowledged that the passive loss rules do not refer to s corporations at all. Passive activity rules apply to individuals estates trusts other than grantor trusts personal service corporations and closely held corporations. You can t deduct the excess expenses losses against earned income or against other nonpassive income.

Passive activity loss rules are generally applied at the individual level but they also extend to virtually all businesses and rental activity in various reporting entities except c corporations. Passive activities are trades businesses or income producing activities in which you don t materially participate the passive activity loss rules also apply to any items passed through to you by partnerships in which you re a partner or by s corporations in which you re a shareholder. Nonpassive income for this purpose includes interest dividends annuities. In addition three other rules discussed below may limit the amount of losses and deductions that may be deducted.

The passive activity loss rules also apply to any items passed through to you by partnerships in which you re a partner or by s corporations in which you re a shareholder. Work you do in your capacity as an investor does not constitute participation in the business unless you are directly involved in the day to day management or operations of the activity. They specifically apply to taxpayers who are individuals estates trusts closely held c corporations and personal service corporations. There are two types of passive income or loss.

If the ventures are passive activities the passive activity loss rules prevent you from deducting expenses that are generated by them in excess of their income. The passive activity loss rules created a special category of income and loss called passive income or loss.

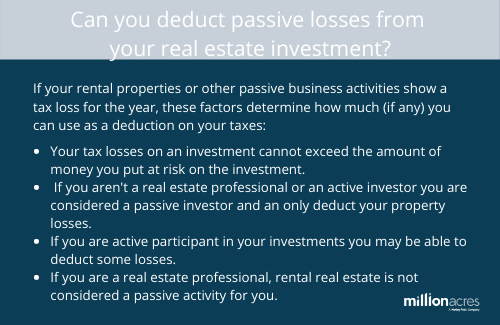

Can I Deduct Passive Losses From Real Estate Investments Millionacres

35 People Share Passive Aggressive Gibberish Phrases That Almost Everyone Uses In Their Workplace In 2020 Passive Aggressive Passive Aggressive Humor Phrase

Investment Risk In Mutual Fund Investing Infographic Investing Infographic Mutual Funds Investing Investing

Pin By Signingagentrenee On Money Making Business Motivation Business Ideas Entrepreneur New Business Ideas

Basic Bookkeeping Small Business Income Sales Expenses Tax Etsy In 2020 Profit And Loss Statement Bookkeeping Bookkeeping Templates

How To Do Credit Spreads In 2020 Options Trading Strategies Option Strategies Trading Strategies

I M Sure You Know There Are No Guarantees When It Comes To Investing Still The Most Successful Investors Do Focus On Some Basic P Investing Finance Investors

Passive Activity Rules For Real Estate Activities Income Tax Course Cpa Exam Regulation Youtube

The Act Allows Flow Through Businesses In New Jersey Such As Sub S Corporations Partnerships Llcs Or Sole Proprietorsh In 2020 Tax Services Tax Rules Tax Deductions

Ep190 What Is Passive Loss And How Can You Use It On Your Taxes Real Estate Investing Wealth Building Real Estate Business

Publication 925 Passive Activity And At Risk Rules Comprehensive Example

Instructions For Form 8995 2019 Internal Revenue Service

Starting Your Own Corporation Can Be More Costly And Time Consuming Than Other Business Types Read Our Five Legal Tips T Business Format Business Legal Advice