Passive Income Loss Carryover

150 000 Income 150 Income Tax Income Tax Student Loan Interest Income

Understanding Passive Activity Limits And Passive Losses 2020 Tax Update Stessa

Pin On Investing

Passive Activity Credit Flowchart

Carryover Of Disallowed Deduction On Passive Activ

Https Encrypted Tbn0 Gstatic Com Images Q Tbn And9gcsctk42 Vco4owgvayigukc0isuagjcz9 Y5q Usqp Cau

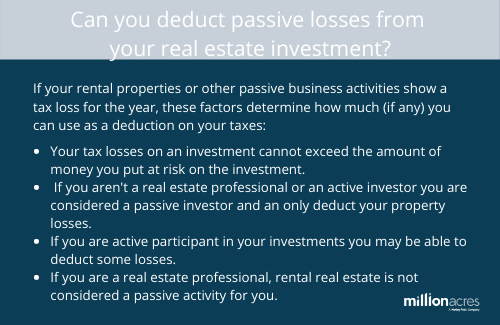

Passive loss carryover occurs when you do not have enough passive income by which to offset these losses for a given tax year.

Passive income loss carryover. A taxpayer can apply suspended losses against passive activity income from any source not just from the activity that created the loss. Under the passive activity rules you can deduct up to 25 000 in passive losses against your ordinary income w 2 wages if your modified adjusted gross income magi is 100 000 or less. The loss continues to be carried over until you use up the entire amount. A passive loss is a financial loss within an investment in any trade or business enterprise in which the investor is not a material participant.

This deduction phases out 1 for every 2 of magi above 100 000 until 150 000 when it is completely phased out. You can carry over these losses until you sell the asset or realize. A passive loss carryover is created when you have more expenses than income a loss from passive activities in a prior year that could not be used that year.

Where Do I Enter Prior Year Passive Losses On Rental Property

36 Passive Income Ideas To Help You Make Extra Money Emoneyindeed

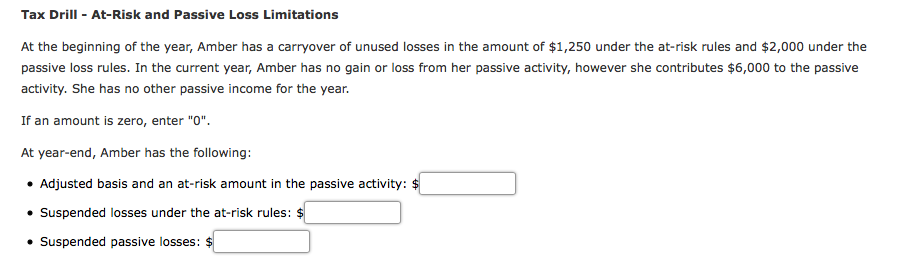

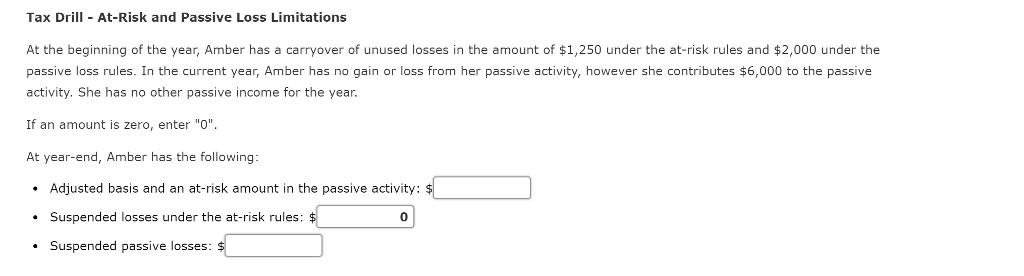

Solved Tax Drill At Risk And Passive Loss Limitations A Chegg Com

Passive Activity Credits And Recharacterized Income

Foreign Tax Credit Form 1116 And How To File It Example For Us Expats

At Risk Limits And Passive Activity Loss Income Tax Course Cpa Exam Regulation Tcja 2017 Youtube

Real Estate

7 Smart Ways To Make Passive Income Off Rental Property Rental Property Investment Firms Passive

How Interior Designers Can Create Passive Income And Why They Should Nest Prosper Interior Design Business Design Clients Creating Passive Income

Passive Activity Loss Limitations

Tax Drill At Risk And Passive Loss Limitations At Chegg Com

Video Mortgage Interest Deductions For Rental Property

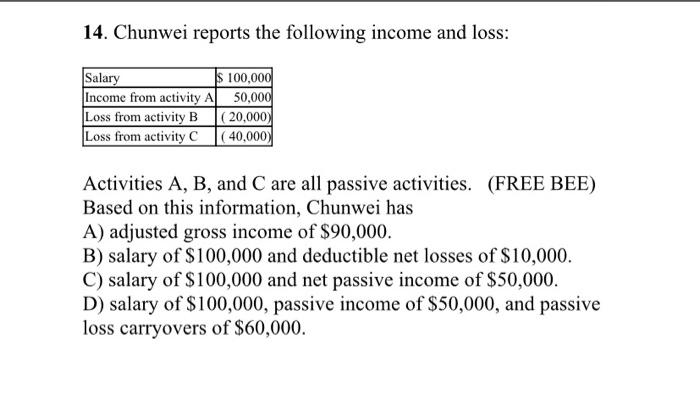

14 Chunwei Reports The Following Income And Loss Chegg Com