Income Tax Rate Japan Foreigners

The Reason For The Globalisation Of Tech R D The Continental Telegraph Global Economics Tech

Home Away From Home Foreign Home And Away Britain

Pin On Economics

Valuing Patents Creativity And Innovation Internet Trends Innovation

Stock Broker Panosundaki Pin

French Banks Play Russian Roulette April 30th 2014 Russia Exposure Russian Roulette

Foreigner taxpayers fall into one of three possible categories.

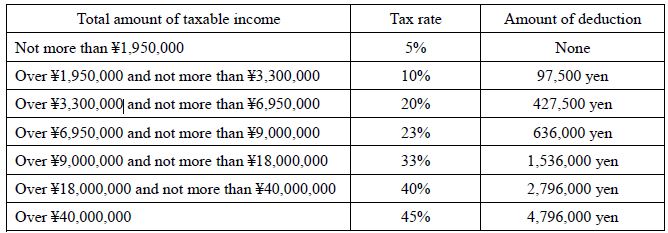

Income tax rate japan foreigners. Foreigners departing japan before the tax deadline must file their returns before they leave or designate a proxy to file a return for them. Those who have lived. Example if taxable income is jpy7 000 000 after deduction of income income tax would be jpy974 000 jpy7 000 000 x 23 636 000. Japanese income tax rates.

Japan s tax year runs from 1 january to 31 december and income tax is payable at a national prefectural and municipal level. Local management is not required. Capital gains tax rate 23 2 30 34 including local taxes residence a company that has its principal or main office in japan is considered to be resident. Taxable income tax rate less than 1 95 million yen 5 of taxable income 1 95 to 3 3 million yen 10 of taxable income minus 97 500 yen 3 3 to 6 95 million yen 20 of taxable income minus 427 500 yen 6 95 to 9 million yen 23 of taxable income minus 636 000 yen 9 to 18 million yen.

National income tax rates. For taxpayers who face difficulty paying their national tax due to the influence of the novel coronavirus disease covid 19 announcement of the event learn and taste local sake in chugoku region tottori shimane okayama hiroshima and yamaguchi on 28 march 2020 pdf 2 013kb. Short term gains are taxed at a flat rate of 30 63 percent including surtax of national income tax plus 9 percent of local inhabitant tax. The list focuses on the main indicative types of taxes.

A foreign corporation generally is taxed only on certain japanese source income. For example the tax rate for withholding tax on interest paid to a foreign corporation is 20 to which the restoration income surtax 20 x 2 1 will be added resulting in a total 20 42 tax withheld at source. Japanese national individual income tax rate for 2015 and after is as below. Returns must be filed between february 16 and march 15.

Income tax is only required on income over 380 000 yen. This applies where the taxpayer is a resident of japan as of january 1 of the current year. The japanese tax year runs from january 1 to december 31. Basis a resident corporation is taxed on worldwide income.

Japanese local governments prefectural and municipal governments levy local inhabitant s tax on a taxpayer s prior year income. Generally in japan the local inhabitant s tax is imposed at a flat rate of 10. Corporate tax individual income tax and sales tax including vat and gst but does not list capital gains tax. Some other taxes for instance property tax substantial in many countries such as the united states and payroll tax are not shown here.

The Meditteranean Of Japan Part 3 Shiraishi Island An Article On Japan Today Travel Writing Japan Today Island

Gross Domestic Product For Japan C Gross Domestic Product Japan Graphing

Real Estate Related Taxes And Fees In Japan

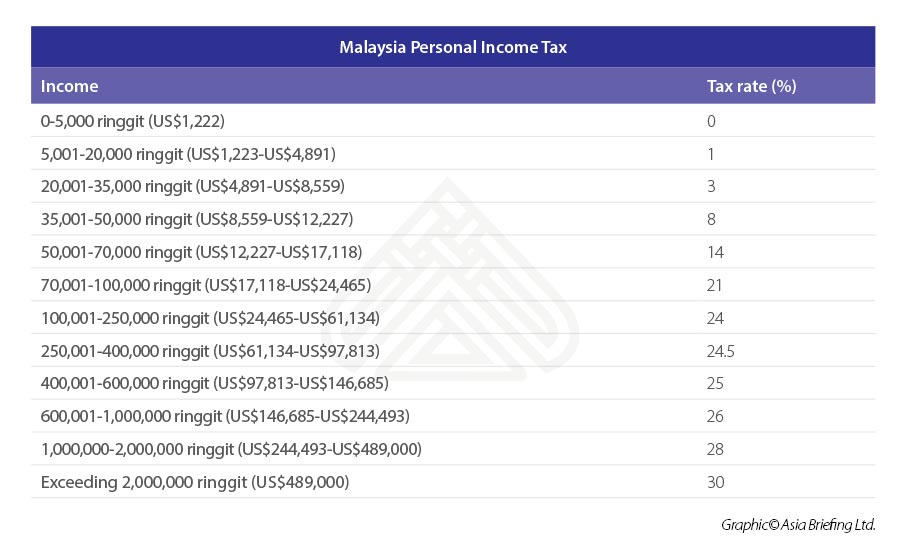

Individual Income Tax In Malaysia For Expatriates

International Liberty Restraining Government In America And Around The World Finland Norway Liberty

Note We Use New York Close Charts Get Our Preferred Charts Trading Platform Here Eurusd Euro Dollar Pulls Back To Near Term Support Uptrend Intact In Goruntuler Ile

Gross Domestic Product For Japan C Gross Domestic Product Japan Graphing

Irs Truck Tax 2290 Filing 2014 2015 Filing Taxes Irs Forms Tax

Pin On World Economy

What Every Foreigner Working In Japan Should Know About Resident Tax Tsunagu Local

Pin On Accounting

Conrad Daren And Jaymieon Jagessar 2018 Real Exchange Rate Misalignment And Economic Growth The Case Of Trinid Exchange Rate Trinidad And Tobago Trinidad

How To Set Canadian Taxes For Your Online Store Canadian Facts Canada Economy Canadian Things