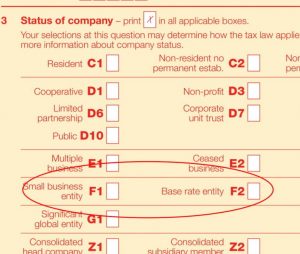

Base Rate Entity Passive Income Meaning

Franking Considerations For Base Rate Entities Taxbanter

Certainty At Last For Base Rate Entities Or Not Taxbanter Blog

Base Rate Entity Rules Avoiding The Royalty Mistake

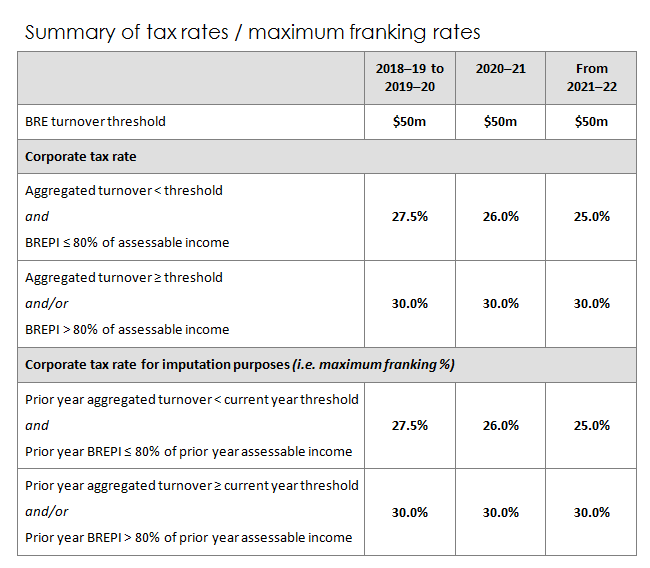

Company Tax Rates Atotaxrates Info

Base Rate Entity Corporate Tax Rates Cordner Advisory

Coffee and cake pty ltd is the owner of a small cafe.

Base rate entity passive income meaning. Similarly if the only income of a discretionary trust was from the carrying on of a trading business an amount distributed to a company would not be base rate entity passive income. Capital gains and franked dividends are the only base rate entity passive income that a trust can stream provided the trust deed allows it. The legislation also makes changes to how a corporate. Example 2 base rate entity.

Because this income is only 3 8 of its assessable income happy feet pty ltd is a base rate entity for the 2019 20 income year and the 27 5 company tax rate applies. Passive income for base rate entity. What amounts of assessable income are base rate entity passive income brepi the meaning of rent interest and when a share of net income of a trust or partnership is referable to an amount of brepi and how to calculate a corporate tax entity s corporate tax rate for imputation purposes and work out the maximum amount of the franking. Starting any type of brand new business particularly an on the internet business can be actually difficult.

Income tax rates act 1986 sect 23ab meaning of base rate entity passive income 1 base rate entity passive income is assessable income that is any of the following. 23aa of the itr act if it satisfies two requirements. The interest income is base rate entity passive income. Instead the carrying on a business test has now been replaced with a passive income test.

From the 2017 18 income year a corporate tax entity must be a base rate entity to be taxed at the lower rate. The ruling considers the meaning of certain types of base. Law companion ruling lcr 2019 5 deals with the passive income threshold and other issues within the treasury laws amendment enterprise tax plan base rate entities act 2018 that limits access to the lower corporate tax rate. Law companion ruling 2019 5 base rate entities and base rate entity passive income the ato released a law companion ruling lcr on 13 december 2019 describing how the commissioner would apply the law to base rate entities from the 2017 18 income year onward.

Requirements Traceability Matrix Excel Template Free Download Project Management Templates Gantt Chart Templates Excel Templates

Syndicated Loan Meaning Parties Involved Process Benefits Etc Syndicated Loan Money Management Advice Finance Investing

Final Account Trading Account Pl Acc Balance Sheet Balance Sheet Accounting Cycle Accounting

Https Www Sage Com En Au Media Files Sagedotcom Australia Documents Pdf 2018 Tax Productivity Manual Pdf La En Au

Https Www2 Deloitte Com Content Dam Deloitte Au Documents Tax Deloitte Au Tax Essentials Understanding Which Corporate Tax Rate Use 040220 Pdf

New Instant Asset Write Off Taxbanter

Tax Knowledge Q A Passive Income From Trust Distributions

12 Best Apps That All Entrepreneurs And Bloggers Need In 2020 In 2020 Business Gadgets Entrepreneur Digital Tools

Https Assets Kpmg Content Dam Kpmg Xx Pdf 2019 06 Australia 2018 New Pdf

Federal Budget 2020 What Is In It For Businesses

Federal Register Medicare Program Fy 2020 Inpatient Psychiatric Facilities Prospective Payment System And Quality Reporting Updates For Fiscal Year Beginning October 1 2019 Fy 2020

20 2 Financial Reporting Considerations Related To Covid 19 And An Economic Downturn March 25 2020 Last Updated September 18 2020 Dart Deloitte Accounting Research Tool

The Small Business Tax Concessions Taxbanter