Income Equalisation Fund Accounting

Pdf The Income Equalization System Among Municipalities In Norway Strengths And Implications

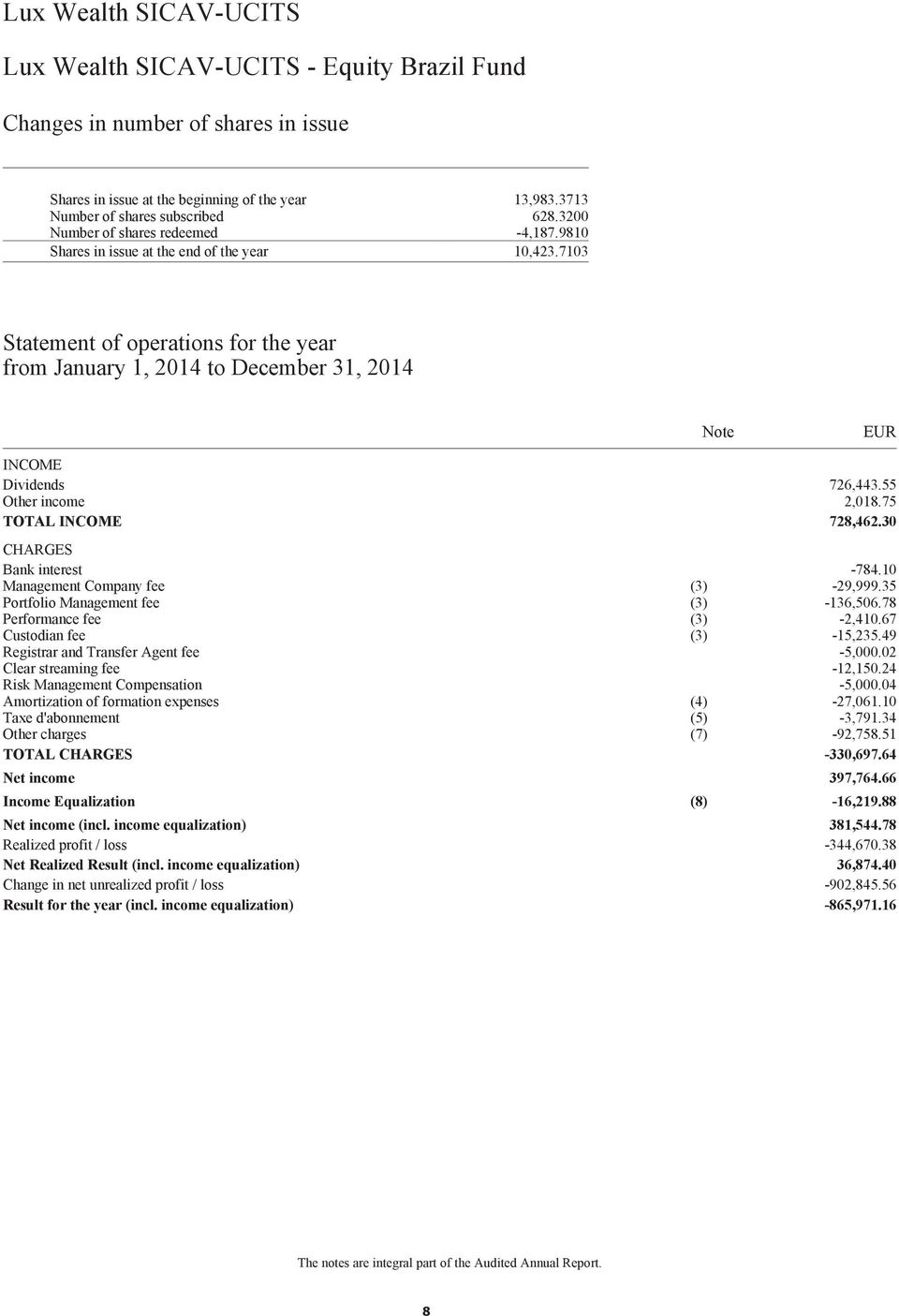

Lux Wealth Sicav Ucits Pdf Kostenfreier Download

Https Www Lombardodier Com Modules Documents Ukrs Ukrs 17984 Ch En Pdf Isin Kyg675281284 Cdcountry Ch Cdlanguage En

Https Www Datev De Dnlexom V2 Content Files St2112297867 Pdf

Equalisation Explained What Is Equalisation Willis Owen

Https Www Bundesfinanzministerium De Content En Standardartikel Press Room Publications Brochures 2019 03 12 Financial Realations Federation 2018 Pdf Pdf Blob Publicationfile V 4

Consequently the equalisation amount should not be recognised in the financial statements of a fund.

Income equalisation fund accounting. Where an investor buys shares during a distribution or accumulation period the price at which those shares are bought may include an amount of income earned since the last distribution or accumulation by the fund income equalisation. Equalisation does not give rise to assets liabilities income expense or equity. This post considers what happens when there is a subsequent closing and in particular what is meant by equalisation the true up. For the fourth post subsequent closings equalisation click here.

Income equalisation schemes including the environmental restoration scheme allow farmers fisher growers and foresters to even out fluctuations in their income by spreading their gross income from year to year. Equalisation is a mechanism used by open ended collective investment vehicles to ensure that income distributions from a fund can be the same for all shareholders regardless of when the shares were purchased. Make all deposits electronically. Provide a bank account for any refunds.

My previous post outlined private equity accounting when there is a subsequent closing and in particular what is meant by equalisation the true up. This can be done a number of ways 1. This is the fourth in a series of posts on private equity fund accounting. In the case of the lf woodford equity income fund income is distributed quarterly.

1 an authorised fund must have an annual income allocation date which must be within four months of the end of the relevant annual accounting period 3. On the occasion of the first distribution or accumulation of income following that purchase that income equalisation will normally be regarded as a non taxable capital return for uk tax purposes. How income equalisation schemes work. We no longer accept cheques for income equalisation schemes unless you have an exemption.

Private equity fund accounting equalisation interest. When you buy a fund between ex dividend dates any income which has been generated but not yet paid out is included in the price you pay for each unit. For the third post drawdowns click here. When a fund pays out income it does so by going.

Taxpayers can now use. By way of background funds that distribute income do so regularly sometimes yearly sometimes half yearly quarterly or monthly. 3 2 an authorised fund may have interim income allocation dates and one or more interim accounting periods for each of those dates2 and if it does the interim income allocation date must be within four months of the end of the relevant. Equalisation is the method used by funds in order to ensure that every shareholder pays the same percentage of performance incentive fee no matter when they subscribe to the fund.

Because of this the. Adverse event income equalisation scheme. Private equity fund accounting subsequent closings equalisation. This is the fifth in a series of posts on private equity fund accounting.

Https Www Universal Investment Com Media Document Jahresbericht 20chartered 20investments 20fund 20ui

Https Www Metzler Com Mwebrel Ajax Fonds Dokumente Content Fondudfo 34u Docid 5

Https Ec Europa Eu Social Blobservlet Docid 9029 Langid En

Http Fondsdocs Edisoft De Getdoc Php D 25 77667 1

Https Www Bafin De Shareddocs Downloads En Merkblatt Wa Dl 190321 Merkbl 320kagb Wa En Pdf Blob Publicationfile V 1

Https Www Pwc Com Jg En Publications Changes To Offshore Funds Reporting Regulations June 11 Pdf

Pin On Income Tax Diary

Https Www Lazardassetmanagement Com Docs M0 21328 Lgaf Reportableincomereports En Pdf

Https Www Pwc Com En Sg Sg International Comparison Of Insurance Taxation 2009 Assets Icit2009 France Pdf

Http Fondsfinder Universal Investment Com Api V1 Es De000a0myg12 Document Jb En

Http Fondsfinder Universal Investment Com Api V1 De De000a2jqj46 Document Vp En