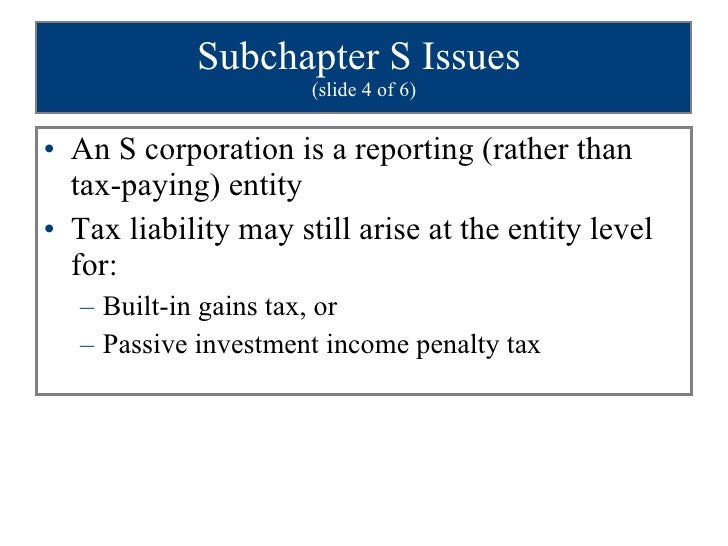

Passive Investment Income Penalty Tax Payable By This Corporation

Https Revenue Alabama Gov Wp Content Uploads 2017 08 810 3 175 01 Pdf

Don T Be Passive About Canada S New Passive Income Rules Advisor S Edge

Investing Through A Professional Corporation Physician Finance Canada

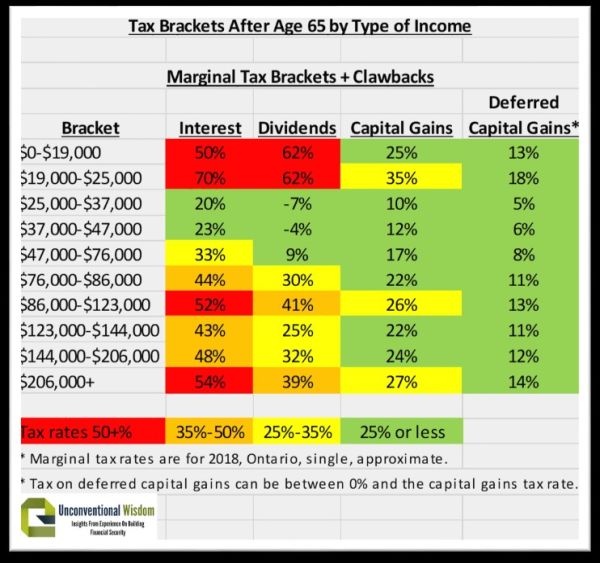

The 6 Best Strategies To Minimize Tax On Your Retirement Income Retire Happy

How Money You Earn Flows Through Your Corporation To Your Pocket Physician Finance Canada

After The Aca Tax Planning For The Current Net Investment Income Tax Cpa Practice Advisor

Brew has accumulated e p of 22 000 and ordinary income of 50 000.

Passive investment income penalty tax payable by this corporation. This rate is to be reduced to 9 percent in 2019. In 2019 the company will earn 500 000 of active business income. Excess net passive income tax. The small business limit the amount of income annually that is eligible for the small business rate is 500 000 federally and in most provinces except for.

As illustrated in the table below the passive income rule change will result in the company paying 40 000 more tax than it would have before the cra passive income tax changes. Taxable income 10 000 5 000 tax payable 47 4 700 2 350 net income 5 300 7 650 rdtoh 26 67 of taxable income 2 667 1 333 cda 50 of capital gain not taxable 5 000 assumes corporate tax rate of 47 per cent. The highest corporate rate is applied to the s corporation s excess net passive income as follows. In 2018 the company earned 100 000 of passive investment income.

It has passive investment income of 100 000 with 40 000 of expenses directly related to the. In 2018 canadian controlled private corporations ccpcs pay corporate income tax on small business income at 10 percent federally. Passive investment income penalty tax brew an s corporation has gross receipts of 190 000 and gross income of 170 000. In february 2018 the government of canada introduced new rules for passive income that could affect how your small business clients are taxed.

It has passive investment income for the tax year that is in excess of 25 of gross receipts. A corporation must pay the enpi tax if all the following apply. Along with relevant topics like passive activity 2020 passive income tax rates and how investors can qualify for the many tax advantages offered in the new tax cuts act of 2018. It has accumulated earnings and profits e p at the close of the tax year.

Passive investment income penalty tax means a tax imposed on the excess passive activity income of an s corporation that has accumulated earnings and profits. The maximum rates applicable to the distributed earnings of c corporations and pass through entities are now fairly comparable 36 8 to 39 8 for c corporations depending on the applicability of the 3 8 tax on net investment income and 37 to 40 8 for pass through entities depending on the applicability of the 3 8 tax on net investment. Taxation of investment income within a canadian corporation corporation s after tax income 5 300 7 650 corporation keeps 44 more. Also learn about the financial impact of short term versus long term investments and how they are taxed differently.

The Jewish Community Foundation Of Montreal Ppt Download

Understanding The Net Investment Income Tax

Infographic What You Need To Know About Real Estate Investing With A Self Directed Ira Real Estate Infographic Real Estate Investing Real Estate Tips

:max_bytes(150000):strip_icc()/dotdash_Final_Investment_Income_Apr_2020-01-fae8874a0f0c4ab38e8e3cc18801e803.jpg)

Investment Income Definition

Chapter 12 Presenatation

2019 Tax Planning Guidelines For Individuals And Businesses The Ledger Mazars Usa The Ledger Mazars Usa

Income And Withholding Taxes Ppt Download

International Tax Jurisdiction Basic Concepts Ppt Download

2019 Year End Tax Planning Individuals Ohio Tax Firm

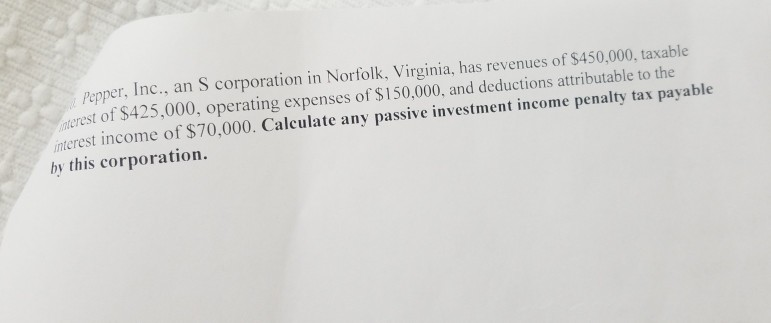

Solved Pepper Inc An S Corporation In Norfolk Virgini Chegg Com

This Chart Tells You How Basic Investment Accounts Are Taxed Investment Accounts Budgeting Money Budgeting Finances

Https Www Iras Gov Sg Irashome Uploadedfiles Irashome Businesses Basic 20format 20of 20tax 20computation 20for 20an 20investment 20holding 20company Pdf

The Pros And Cons Of Credit Cards In India In 2020 Rewards Credit Cards Credit Card Help Credit Card Protection