Passive Loss Rules Real Estate

Understanding Passive Activity Limits And Passive Losses 2020 Tax Update Stessa

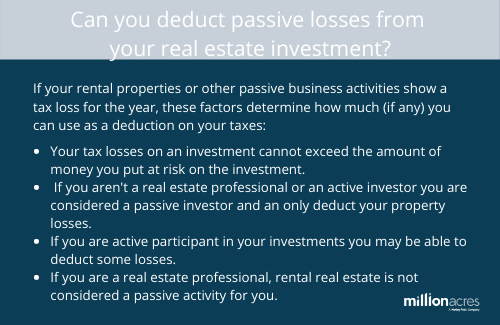

Can I Deduct Passive Losses From Real Estate Investments Millionacres

Passive Activity Credit Flowchart

Passive Activity Rules For Real Estate Activities Income Tax Course Cpa Exam Regulation Youtube

Reporting Information Regarding Llcs Passive Activities

Rental Property Loss Deduction Rules 2020 Youtube

Rental real estate activities generally are considered passive activities regardless of whether the taxpayer materially participates.

Passive loss rules real estate. Any rental real estate loss allowed because you materially participated in the rental activity as a real estate professional as discussed later under activities that aren t passive activities. What is a passive business activity. A pal is the amount by which the taxpayer s aggregate losses from all passive activities for the year exceed the aggregate income from all of those activities. When you own an income property and are earning your income through monthly rent payments this is considered passive income by the irs.

He owns 2 rental properties that generate 28 000 of losses in which he materially participates in the management. This is his main source of income. The other exception to the pal rules is the one for real estate professionals. However the rules for who is a real estate professional for tax purposes are rather specific and the irs enforces these rules rather strictly.

Llc and files a schedule c as a real estate trade or business. Thus at first glance it appears the taxpayers took every necessary step to help ensure they could treat the real estate activities as nonpassive activities. According to the irs a passive activity is one in which the taxpayer doesn t. Unlike the 25 000 exception described above this is a complete exemption from the rules that is landlords who qualify as real estate professionals may deduct any amount of losses from their other non passive income.

This is different than typical active income that would come with a standard. His modified agi is 175 000 before the losses. Passive loss rules were established by the irs back in 1986 and they are something that all rental property owners need to know about. Here s what all real estate investors need to know about the passive loss rules.

In general taxpayers in the real property business or real estate professionals can exclude their rental activity or activities from the passive activity loss rules. Any overall loss from a publicly traded partnership see publicly traded partnerships ptps in the instructions for form 8582. However since rental real estate income is considered to be passive in nature there are special rules called the passive activity loss rules that can limit the amount of rental real estate or. Since he is a real estate professional the.

If one is classified as a real estate professional any losses are treated as ordinary losses and may be deducted against other income sources.

Passive Activity Loss Rules And Limitations

Ep190 What Is Passive Loss And How Can You Use It On Your Taxes Real Estate Investing Wealth Building Real Estate Business

Tax Passive Activity Loss Rules Overview Short Term Rental Passive Activities

Passive Activity Losses Real Estate Professionals Bkd Llp

Real Estate Professionals Avoiding The Passive Activity Loss Rules

Passive Activity Loss Rules And Limitations

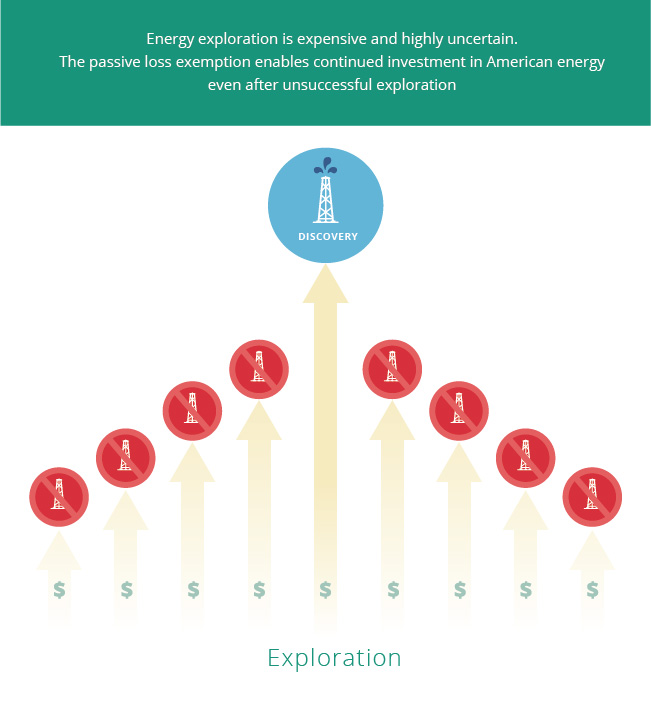

Passive Loss Exception Energy Tax Facts

How To Deduct Rental Losses And Get Around The Passive Loss Rules

Passive Activity Loss Limitations

1031 Exchanges On Property With Passive Activity Losses 1031 Experts

Is Rental Income Passive Or Active Free Investor Guide

Passive Losses And Rental Real Estate Mark J Kohler Tax Legal Tip Youtube

Ep190 What Is Passive Loss And How Can You Use It On Your Taxes Real Estate Advice Real Estate Business Investing